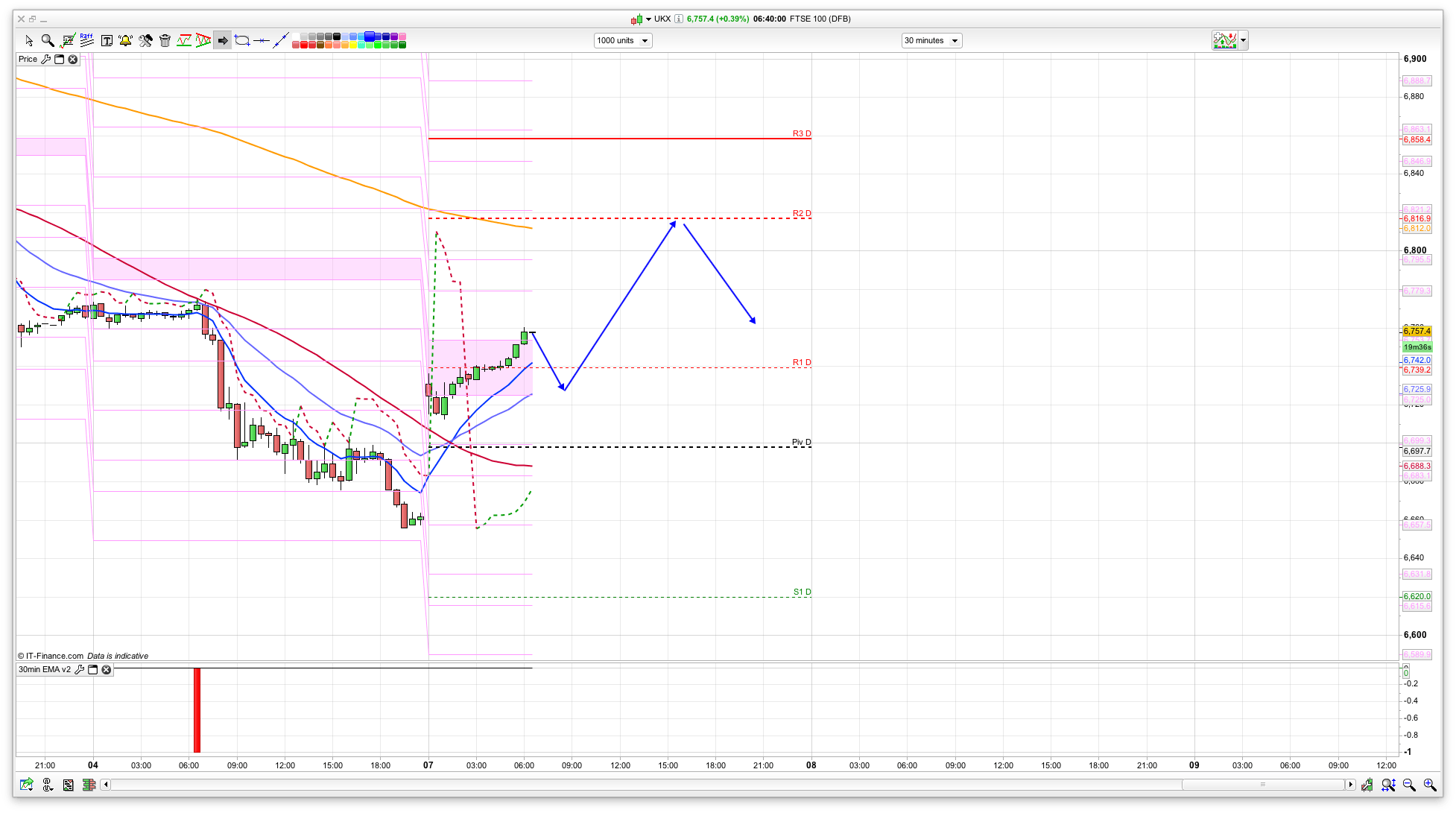

FTSE 100 Support 6725 6697 6670 6665 6598

FTSE 100 Resistance 6803 6812 6858 6860 6904 6959

Good morning. All set for election week? Latest polls have put Clinton further in the lead, and the FBI have not found anything incriminating in the latest batch of her emails, both of which have resulted in a climb in indices since Sunday night. The SP has held that 2085 (we had 2075 to 2085 as support on Friday) and gapped up to 2111 overnight, while the FTSE 100 has added 100 to 6759 currently. Today and tomorrow is obviously going to be mostly sentiment driven, based around polls and results heading into Tuesdays election, so the technicals wont have as much bearing at the moment. It looks like a long really for today off the back of the news.

US & Asia Overnight from Bloomberg

Mexico’s peso gained with Asian equities and U.S. stock index futures after the Federal Bureau of Investigation said it maintains the view that Hillary Clinton’s handling of her e-mails wasn’t a crime. The yen and Swiss franc retreated with gold.

Mexico’s currency, which has tended to strengthen on signs Republican presidential candidate Donald Trump’s campaign is faltering, climbed the most in four weeks and the MSCI Asia Pacific Index rebounded from a one-month low ahead of Tuesday’s U.S. presidential election. The yen sank by the most in a month, U.S. Treasuries fell and gold dropped for the first time in eight days as investors shunned haven assets. Hong Kong property shares tumbled by the most since January after the government announced shock measures to cool the world’s least affordable housing market.

The FBI is sticking with its view that Clinton’s handling of e-mails during her tenure as secretary of state wasn’t a crime, after reviewing new communications potentially related to the Democratic candidate, director James Comey said Sunday in a letter to Congress. Comey’s announcement just over a week earlier that the bureau was looking into more e-mails sparked a selloff in risk assets, with U.S. stocks capping their longest run of losses since 1980. The peso’s fortunes have been tied to Trump’s campaign given his pledge to renegotiate trade deals with Mexico and to build a wall along the U.S. border.

“The market is viewing the latest Hillary Clinton news as a positive, at least in the short term,” said Richard Sichel, chief investment officer at Philadelphia Trust Co., which oversees $2 billion. “It may still be a close call in the end, but the market for the time being is acting as if some of the uncertainty is gone.”

Currencies

The peso climbed 1.7 percent versus the dollar as of 12:42 a.m. Tokyo time. The currency fell in each of the last two weeks as Clinton’s lead over Trump narrowed in opinion polls amid the FBI’s renewed probe of her emails, an issue that has dogged her campaign.

The Bloomberg Dollar Spot Index rose for the first time in seven days on optimism the FBI’s latest statement will make a Clinton presidency more likely and pave the way for the Federal Reserve to raise interest rates in December. Trump has advocated winding back free-trade agreements, which may hinder global economic growth and make the central bank less inclined to tighten policy.

“A Clinton win would clear the decks for the Fed to raise rates in December and for markets to price in a more aggressive profile for tightening over 2017,” said Sean Callow, a senior strategist at Westpac Banking Corp. in Sydney. “The surge in U.S. equity futures and slide in the gold price reinforces the evidence that a Trump win is seen as negative for global growth and profits.”

The yen weakened 1 percent to 104.11 per dollar. The haven currency rallied 1.6 percent last week, the most since July. The franc slipped 0.6 percent, after surging 2 percent last week.

China’s yuan fell by 0.3 percent, the biggest loss in a month, after the central bank lowered its daily reference rate ahead of an update on the nation’s foreign-exchange reserves. The holdings are expected to have dropped by $34 billion to $3.13 trillion in October, according to the median forecast in a Bloomberg survey.

Stocks

The MSCI Asia Pacific Index added 0.4 percent, after sliding 1.4 percent last week. Westpac Banking Corp. led gains among Australian banks after reporting earnings and HSBC Holdings Plc added 1 percent in Hong Kong ahead of its results. Japan’s Topix index gained 1.1 percent, recovering from its biggest weekly loss since July, as the yen’s retreat gave a boost to the nation’s exporters. New Zealand’s benchmark stock gauge jumped by the most in five years.

“All that drama and yet the FBI director is sticking to the same conclusion that they had in July with respect to Hillary Clinton’s e-mail,” said Naeem Aslam, chief market analyst at Think Markets U.K. Ltd. in London. “This is good news for investors who have an appetite for risk in this environment.”

The Hang Seng Property Index of property shares tumbled by the most since January after the government raised stamp duty on home purchases, meaning foreign buyers will now pay an effective 30 percent. Cheung Kong Property Holdings Ltd. and Sun Hung Kai Properties Ltd. tumbled more than 8 percent.

S&P 500 Index futures rallied 1.2 percent following a nine-day slide in the underlying benchmark. The CBOE S&P 500 Volatility Index, a gauge of expected swings in U.S. stocks, soared 39 percent last week as Clinton’s lead was cut. While the race has tightened, the Democratic nominee maintains a 2.2 percentage-point lead over Trump, according to an average of polls by RealClearPolitics.

Commodities

Gold fell as much as 1.3 percent to $1,288.11 an ounce. It surged 2.3 percent last week amid concern Republican Donald Trump may capture the White House, with Citigroup Inc. predicting a rally to $1,400 if he were to win. Adding to the headwinds for bullion, U.S. employment data on Friday bolstered the case for higher borrowing costs and Fed Bank of Atlanta President Dennis Lockhart signaled a December rate hike was likely. Nickel surged 3.7 percent to a three-month high in London after violent protests in Jakarta on Friday spurred concern that Indonesian supplies could be disrupted. Copper advanced to its highest level since April.

Crude oil rose 1.1 percent to $44.54 a barrel in New York after Algeria’s energy minister said he remains confident the Organization of Petroleum Exporting Countries will set output quotas at its next meeting to manage production.

“The market will continue to have a watching brief on OPEC,” said Ric Spooner, a chief market analyst at CMC Markets in Sydney. “There’s going to be plenty of scope for volatility around the election.”

Bonds

The yield on U.S. Treasuries due in a decade increased by four percentage points to 1.82 percent as Clinton’s improved election prospects were seen boosting the likelihood of a Fed rate hike next month.

If Clinton wins, “interest rates are likely to head higher as the market looks towards Fed normalization,” said Eugene Leow, a fixed-income strategist at DBS Group Holdings Ltd. in Singapore. “Conversely, sentiment is likely to deteriorate further if Trump wins. We suspect that the knee-jerk reaction lower in yields would be comparable to what was seen in the immediate aftermath of Brexit.” [Bloomberg]

FTSE 100 Outlook and Prediction

The market has had a good bounce overnight off the back of the poll and FBI news, so I think that the bulls will be in charge for the moment. Buying the dip is probably the best course of action, though obviously its going to be more of a gamble today and tomorrow as we near the result on Wednesday our time. We have the pivot for support at 6697, though the 25ema on the 30min slightly above that at 6725. The daily chart is still bearish with resistance at 6904, so worth a short here though I don’t think we will get that high today. The bulls will need to break the 6803 area today to push higher, though of course the SP, Dax and FTSE have all left rather large gaps on the charts now – 2086, 6662, 10218 respectively – which might well close at some point.

So, today wise, I am looking at resistance at the 6805 area and support as the 6725 area to start with, but stay nimble for the next 2 days!

Caught the sell off well Friday on all indices, rebought last thing Friday and cashed in this morning.

A few small shorts. Long on gold.

FTSE has 18.6 Div I think this week too BTW

Afternoon all. So, could anyone shed some light on what might be the local time/s to be looking at the indices on election day tommorrow, in order to possibly catch some volatile movements etc…thanks all.

Timeline here http://www.telegraph.co.uk/news/0/what-time-are-the-us-election-results-in-the-uk-and-what-is-the/

Ok many thanks nick

So it looks like 4a.m. wed is when we’ll know if clinton is defo in. A woman head of u.k., and a woman head of u.s., up against Putin…asking for it, isnt it? Anyhow, I’m guesing indices should be well choppy tommorrow…

My plan is to sell Dow and Dax rallies today if they happen. Have some shorts in already as I figure there likely to be some profit taking prior to Wednesday 4am

I am long Gold, and looking to close some existing FTSE longs if it rallies up.

That’s my plan

Entered Dow short a little early. Result I am now in horridly heavy!

Buy the rumour sell the news I hope!?!

24pt divi on Dow has compounded my pain!!!

Livid!!!

Ouch