FTSE 100 live outlook prediction analysis for 17th September 2020

- UK inflation slows, but less than feared, as meal discounts cut down consumer costs

- CPIH inflation falls to weakest level since December 2015

- Stocks mixed as investors await Federal Reserve decision

- Second virus wave will slam breaks on recovery, OECD warns

Annual UK consumer price growth slowed to its lowest level since 2016 as Rishi Sunak’s signature Eat Out to Help Out meal discount scheme cut into public spending costs. CPI inflation fell to 0.2pc year-on-year, following a 0.4pc fall in prices between July and August. Although the figure was stronger than expected, inflation remains well below the Bank of England’s 2pc target. Higher costs for video games represented one of the biggest contributors to price growth across the month, with gains also offset by hospitality sector VAT cuts.

Near Zero Target

Federal Reserve officials held interest rates near zero and signaled they would stay there for at least three years, vowing to delay tightening until the U.S. gets back to maximum employment and 2% inflation. The Federal Open Market Committee “expects to maintain an accommodative stance” until those outcomes are achieved, it said in a statement Wednesday. The fresh guidance is the Fed’s first step in an evolving communication strategy after it unveiled a new long-term policy framework to allow inflation to overshoot their 2% target after periods of under-performance. “This very strong, very powerful guidance shows both our confidence and our determination,” Powell told a press conference following the decision. The Treasuries yield curve steepened slightly Wednesday after the decision.

Markets Tepid

Asian stocks headed for a cautious start Thursday after the Fed’s latest comments, and tech shares retreated in the U.S. Futures were flat in Japan while those in Hong Kong and Australia slipped. The S&P 500 Index earlier erased gains to end the session lower after Powell said he’s not sure if the faster-than-expected recovery will continue. A tumble in tech behemoths such as Apple and Facebook also dragged down the gauge. The Treasury yield curve steepened as Powell stopped short of offering new specifics on the Fed’s approach to the monthly bond purchases that have buttressed markets. Some traders may have been expecting signals regarding plans to target longer maturities. The dollar was little changed. Elsewhere, oil surged after government data showed shrinking U.S. crude stockpiles.[Bloomberg]

FTSE 100 Outlook | Trading Signals | Forecast | Prediction | Analysis

The dollar climbed and Asian stocks dropped with U.S. and European futures Thursday after Federal Reserve Chair Jerome Powell highlighted uncertainty about the economic rebound. Treasuries ticked up.

A gauge of Asian shares fell the most in a week, with losses greatest in Hong Kong, South Korea and Australia. S&P 500 futures slipped about 1%. The U.S. benchmark erased gains on Wednesday to end the session lower after Powell said policy will remain accommodative while cautioning that the pace of economic activity will likely slow. A tumble in tech giants such as Apple Inc. and Facebook Inc. weighed on the index. The offshore yuan retreated.

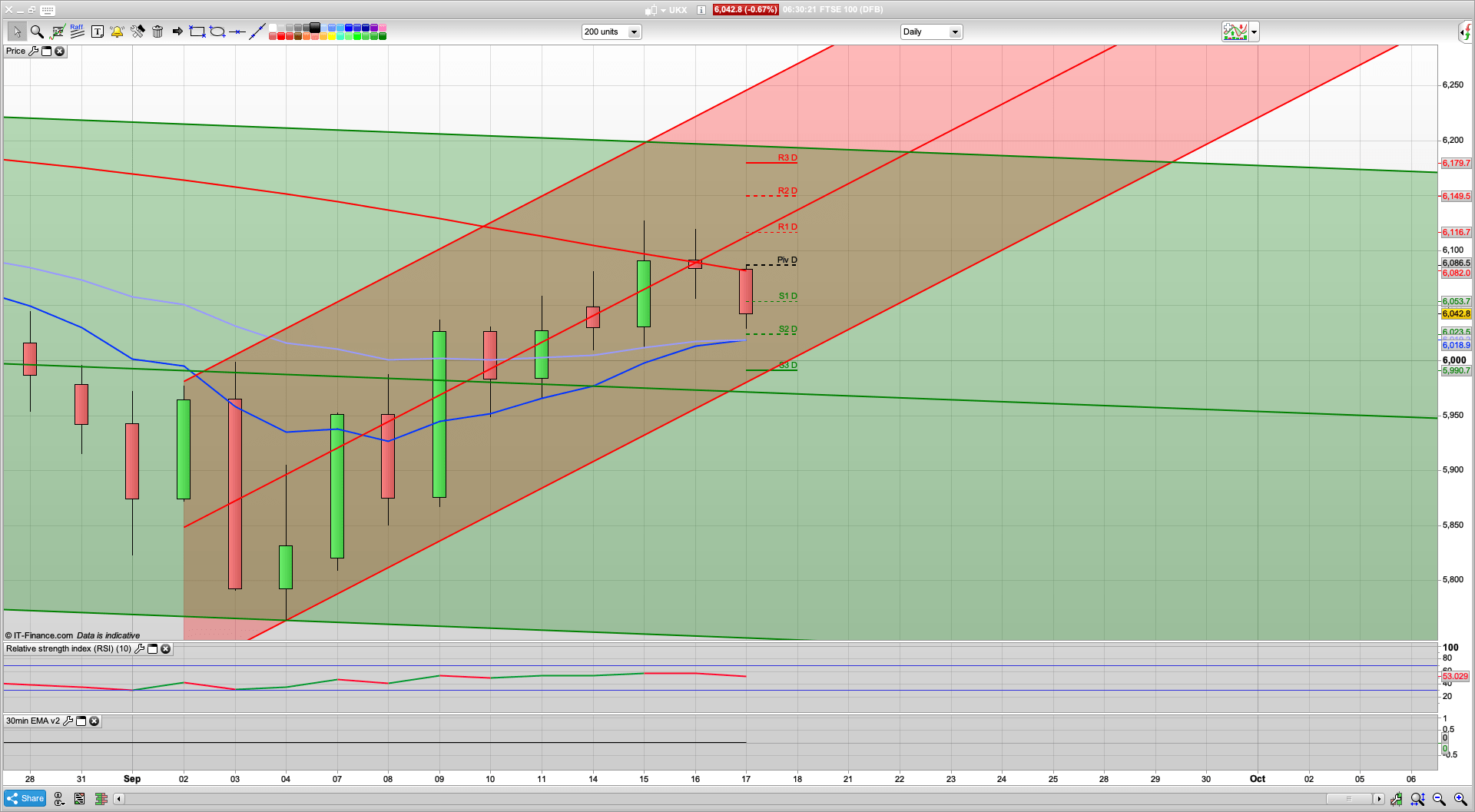

Overnight we have had more weakness creep in as the S&P has dropped off the 3425 level after that cheeky stop hunt to 3430. The big test for today will be S3 at 3330 – the bulls will be keen to defend this and if they manage it it may well help the FTSE stay above the 6000 level. Interestingly the FTSE 100 daily chart is very tentatively going bullish with 6018 support from the moving averages and a rise from here (it also ties in with S2 and a fib level) would make sense, certainly back towards the pivot at 6086.

The 10 day Raff channel remains bullish and 5980 is the bottom of that which if it holds may start to lock in the October rally. 5990 is also S3. For the moment though we look to be in the pullback phase. Daily RSI is at 51 so a dip to bring that down before further upside would fit quite well. The 2 hour chart is bearish to start with today though and 6100 is resistance on that for the moment. As such a rise to this area would probably see the bears reappear. I am not convinced that we rise that far today though and 6085 looks to be decent resistance for any climb.

Initially we have broken below the 200ema as I write this, and that is the closest resistance this morning at 6048. The ASX200 had a bearish session today and we may well do the same, especially if the US continues that slide down towards the 3330 level. Below that then the recent support level of 3000 would be the next level to try longs from. That held last week.

To start with today it would appear that the bears are back in control, and with US retail sales data missing the mark yesterday they may well want their moment in the sun. As such, be cautious with the longs for the moment. We also have quadruple witching tomorrow as the various contracts roll over, so expect more chop tomorrow.

So, 6018, 5990 for support today. 6086, 6100, 6124 for the main resistance levels.

Recommended Broker

IC Markets – offers market leading pricing and trading conditions by providing clients with True ECN Connectivity; this allows you to trade on institutional grade liquidity from the world’s leading investment banks, hedge funds and dark pool liquidity execution venues. Highly recommended!

Membership and Live Trading

If you would like more detailed analysis for FTSE 100, DAX, Gold and S&P, including the trades that I am looking to take myself, then please join my active members community.

What you get

- Daily Analysis pre market open (sent around 7am each day) for FTSE, DAX, Gold and S&P.

- Daily email pre market includes my trading plan for the day including ORDER levels, with stops and targets/limits

- Telegram live trading room and webinar group membership for discussion and realtime trade updates

Keep up to date with new content, free sign up below

[yikes-mailchimp form=”4″]