FTSE 100 Support 6770 6736 6730 6706 6698 6631

FTSE 100 Resistance 6768 6788 6796 6806 6812 6868 6893

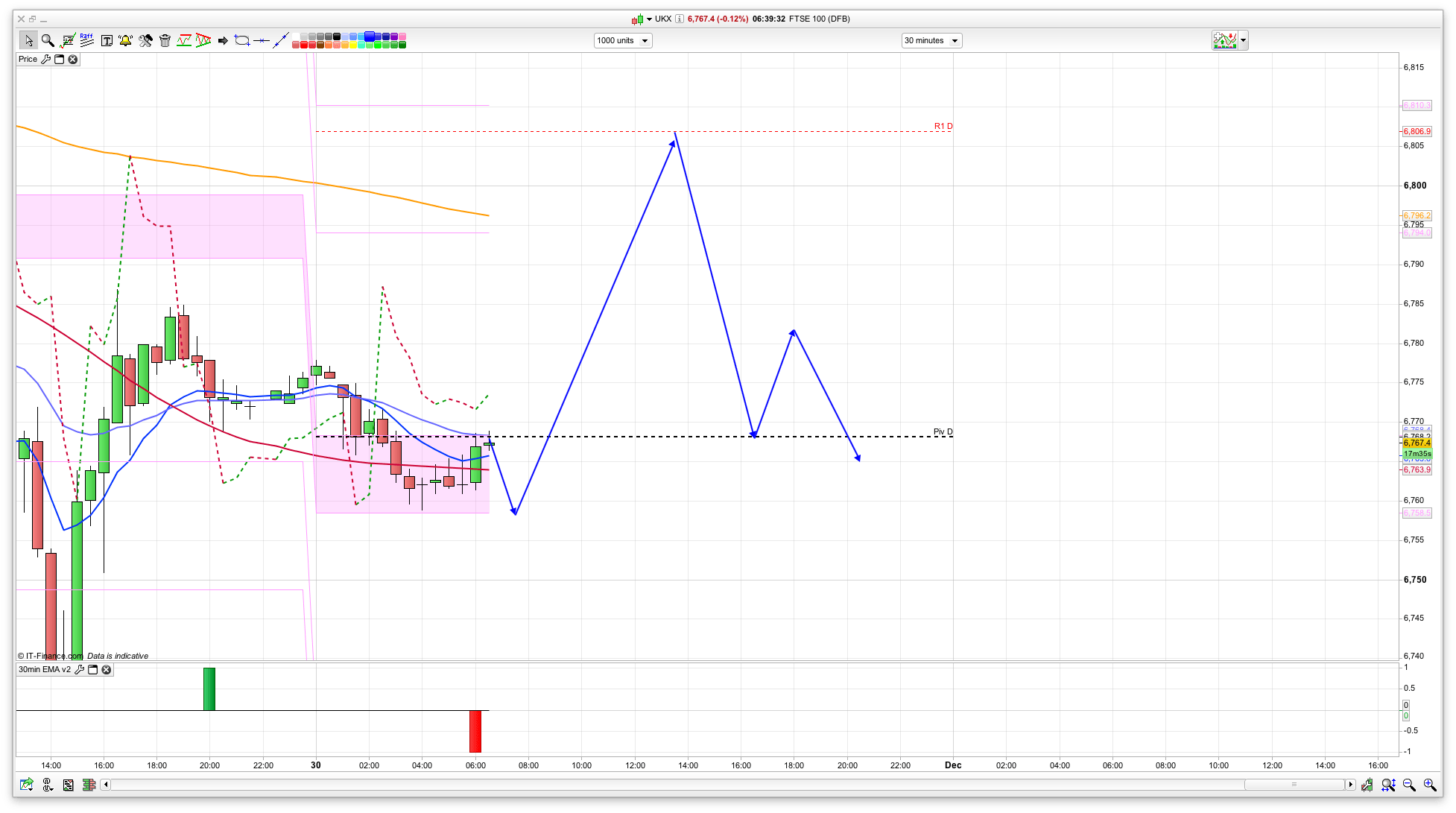

Good morning. Nice to see the lower level support at 6730 hold yesterday for a nice run up to 6780. Shame the S&P order at 2198 just missed as that also had a great bounce to 2210 (target level). The rise however looks like it might not be the start of anything too bullish and in fact we may be on for further declines. We have already dropped back from 6780 overnight, and still have 2 hour resistance at 6788 and 6812. The S&P has been weaker overnight dropping back from 2210 to 2202.

US & Asia Overnight from Bloomberg

- Output pact under threat as day of Vienna meeting dawns

- Greenback climbs with Treasuries premium at nine-year high

Oil held below $46 a barrel ahead of a make-or-break OPEC meeting on stabilizing the crude market, while the dollar headed for its steepest monthly advance since May as U.S. yields rose.

Crude bounced off a two-week low reached Tuesday, when 10 hours of talks failed to resolve differences between oil-producing nations ahead of Wednesday’s formal meeting in Vienna. Treasuries fell, sending up yields that have already reached the highest relative to global peers since 2007. That spurred gains in the greenback, which is headed for the biggest one-month advance versus the yen since 2009.

Equities also advanced in Singapore — poised for their longest stretch of gains since 2014 — and in South Korea. Industrial metals extended declines, retreating for a second session after the London Metal Exchange Index reached the highest since May 2015 on Monday.

With the market giving just 30 percent odds to an agreement to end the oil supply glut, according to Goldman Sachs Group Inc., pessimism regarding the OPEC talks is helping quell a commodities rally sparked by Donald Trump’s surprise presidential victory. Investors are retreating from some of November’s standout trades as the month comes to a close, with the dollar faltering near a decade high that had been reached as Trump’s win fueled bets on higher interest rates. The monthly U.S. payrolls report is due Friday, after data Tuesday showed growth last quarter beat forecasts.

Australia unexpectedly reported its steepest year-on-year drop in building approvals since 2011, while Japan’s weaker industrial output data was in line with estimates. Thailand issues data on trade and manufacturing output later Wednesday, and Sri Lankan updates on consumer prices. Markets in the Philippines are closed for holidays.

Commodities

WTI crude futures added 0.6 percent to $45.51 a barrel as of 12:48 p.m. in Tokyo, paring back from Tuesday’s 3.9 percent tumble to trim their November decline to 2.8 percent.

Iran has vowed not to cut output, while Saudi Arabia said it is ready to reject an agreement unless all OPEC members — excluding Libya and Nigeria — take part, people familiar with the kingdom’s position said.

Tin, nickel and lead each slumped at least 1 percent. The London Metal Exchange Index tumbled 3.4 percent on Tuesday, its biggest one-day retreat in more than a year.

Gold for immediate delivery gained 0.1 percent to $1,189.98 an ounce; it’s down 6.8 percent since Oct. 31, poised for its worst month since June 2013.

Stocks

The MSCI Asia Pacific Index added 0.1 percent as Singapore’s benchmark gauge climbed for a seventh day, rising 0.7 percent.

Shares in telecommunications service providers were the biggest gainers in the region, rising 0.8 percent as a group, followed by technology equities, while materials companies slid 1.2 percent.

Australia’s S&P/ASX 200 Index fell 0.5 percent, with sub-gauges of raw materials producers and energy stocks down at least 1.9 percent.

Futures on the S&P 500 Index were down 0.1 percent after the underlying benchmark rose 0.1 percent to 2,204.66 on Tuesday.

Currencies

Bloomberg’s dollar gauge, which tracks the greenback against 10 major peers, climbed 0.1 percent; it has risen 3.5 percent since Nov. 24 and hit a decade high last week.

The kiwi and the renminbi rose by at least 0.2 percent, paring their declines in the month.

One-month forwards on Russia’s ruble retreated 0.3 percent.

The dollar climbed 0.2 percent to 112.54 yen, adding to Tuesday’s 0.4 percent increase.

[Bloomberg]

FTSE 100 Outlook and Prediction

For today I am expecting to test the 2 hour resistance levels at 6788 and 6812 before further downside. The bottom of the 10 day Raff has held a couple of tests though it popped just below yesterday before rallying back. As such, that tells me that the bears are gaining in strength and shorting the rallies is a good plan. We have a small dividend today on the FTSE 100 at 1.2. Not likely to see masses of buying towards the close for that, but bear it in mind.

For support we have the bottom of the 10 day Bianca at 6770 – pretty much where we are as I write this, with a bearish looking 30min chart to start with, though the 10 min chart has some weak bull to start with.

If we break yesterdays low at 6730 then 6680, 6660 and 6631 are the next supports to note. I am watching that 6812 area quite closely today. If the bulls manage to break that then the bearish momentum shifts a bit and we might well start to see a climb towards the 6850 and 6900 areas. As such, if the bulls push past this 6812 then flip to a long trade.

With that bad news about banks failing stress tests they dont want the jitters to spread so we are seeing a pump this morning. I can just imagine the headlines otherwise – banks fail stress test, ftse falls 2% which would spook the masses. And they don’t want that. Need to postpone Credit Crunch 2 for as long as possible

Nick- Think oil price pushing up the FTSE

Oil its up 7.5% FTSE < 1%

Yes, and OPEC. screwed up my 6810 short with that rise to 6840 🙁

6660 coming soon me thinks!

shorted 44!

out @25

Nice one!

Gold is getting spanked.