FTSE 100 Support 6757 6741 6730 6714 6711 6706 6680 6660 6633

FTSE 100 Resistance 6790 6793 6794 6829 6849

Good morning. Well the first supply cut by OPEC since 2008 caused the FTSE to rise beyond the 6810 resistance level I had yesterday, managing to reach R2 at 6845 before dropping back. Typical that they announce a cut just after I have shorted the FTSE! Despite that rise, the bulls failed to hold above 6800 and it still looks bearish to me at the moment. I am still feeling a dip down towards 6660 before a brief Santa Rally towards the end of the month and then a gloomy 2017. Gold had a shocker yesterday and overnight, hitting 1162, but has started to climb back up.

US & Asia Overnight from Bloomberg

- U.S. oil climbs above $50, building on 9.3% gain on Wednesday

- Private jobs data adds to U.S. rate outlook before payrolls

Asian equities rallied the most in three weeks as a deal to cut global oil output lifted energy shares, while evidence of strength in the U.S. economy sank bonds.

Australia’s Santos Ltd. surged 12 percent, Japan’s Inpex Corp. 11 percent and China’s CNOOC Ltd. 6 percent after the OPEC-led pact to reduce production for the first time in eight years sent U.S. crude above $50 a barrel. Japanese exporter stocks also got a boost after better-than-expected private U.S. jobs data. Yields on government debt in Australia and New Zealand rose after a slump in Treasuries, which had their worst monthsince 2009 in November. The yen gained, recouping some of its 1.9 percent loss against the dollar on Wednesday.The oil deal, which until Wednesday’s meeting seemed in peril, provided further support for so-called reflation trades after Donald Trump’s election as U.S. president added to expectations for fiscal stimulus and Federal Reserve rate increases. Friday’s official U.S. payrolls data is the next focal point, after ADP Research Institute reportedthe biggest increase in private-sector workers since June. China’s official factory gauge came in Thursday at 51.7, above the 51 reading expected by economists, as smokestack industries regained momentum.

“The reflation trade continues to work in earnest, this time Trump has taken a back seat and OPEC and Russia have taken the initiative and lit the fuse under the oil price,” Chris Weston, chief markets strategist in IG Ltd. in Melbourne, said in an e-mail to clients. “We have once again seen that the dollar is the place to be.”

Stocks

The MSCI Asia Pacific Index added 0.8 percent as of 12:18 p.m. Tokyo time, the most since Nov. 10, as a sub-gauge of energy stocks jumped 4.4 percent.

Japan’s Topix index returned to its highest level since January, rallying 0.9 percent, while Hong Kong’s Hang Seng Index was up 0.6 percent and the Jakarta Composite Index was up 0.9 percent.

Australia’s S&P/ASX 200 Index rose 1.1 percent, snapping a three-day drop as New Zealand’s S&P/NZX 50 Index climbed 0.5 percent, while the Kospi in Seoul was 0.2 percent higher.

Futures on the S&P 500 Index were 0.1 percent higher, after the underlying benchmark slipped 0.3 percent Wednesday, trimming its November gain to 3.4 percent, still the best monthly performance since July.

Commodities

West Texas Intermediate crude rose 1 percent to $49.96 a barrel and traded as high as $50.01 after surging 9.3 percent last session, the biggest one-day gain since Feb. 12. It ended November up 5.5 percent.

The OPEC-led deal was broader than many people had expected, given that it extended beyond the bloc with Russia agreeing to unprecedented cuts to its own output.

Gold rebounded 0.2 percent, after sliding 1.3 percent last session to its lowest level since February.

Currencies

The yen gained 0.3 percent to 114.07 per dollar, after touching its weakest point since March 10. The euro strengthened 0.2 percent to $1.0608.

Bloomberg’s Dollar Spot Index, which tracks the greenback against 10 major peers, slid 0.2 percent after advancing 0.5 percent Wednesday, leaving it up 3.9 percent in November, the most since September 2014.

“The failure of U.S. 10-year Treasury yields to get through 2.40 percent will likely cap the dollar ahead of payrolls and the Italian referendum,” said David Forrester, a strategist at Credit Agricole SA’s corporate and investment-banking unit in Hong Kong.

The yuan dropped 0.1 percent onshore, reflecting dollar strength, and gained 0.2 percent offshore amid strengthening factory gauges and a crackdown on capital flows.

Malaysia’s ringgit — which typically moves in line with oil prices given the country is Asia’s only major net crude exporter — was little changed as the dollar’s revival canceled out gains from the OPEC deal. The rupiah lost 0.1 percent.

Bonds

Yields on Australian bonds due in a decade rose a third day, climbing seven basis points to 2.80 percent, while those in New Zealand advanced 11 basis points. Japan’s benchmark yield was 2 basis points and has closed above zero since mid-November.

Ten-year Treasury notes yielded 2.38 percent after surging nine basis points Wednesday to their highest close since July last year. It jumped 56 basis points last month.

Private payrolls in the U.S. climbed by 216,000 this month, after a 119,000 gain in October that was revised lower, ADP data showed Wednesday. Economists are predicting an 180,000-worker increase in nonfarm payrolls in Friday’s data, after they climbed by 161,000 in October.

The Bloomberg Barclays Global Aggregate Total Return Index of bonds fell 4 percent in November, biggest decline since index started in 1990.

“A lot of people are beginning to think that it is the end of the bull rally,” said Roger Bridges, the chief global strategist for interest rates and currencies in Sydney at Nikko Asset Management’s Australia unit

[Bloomberg]

FTSE 100 Outlook and Prediction

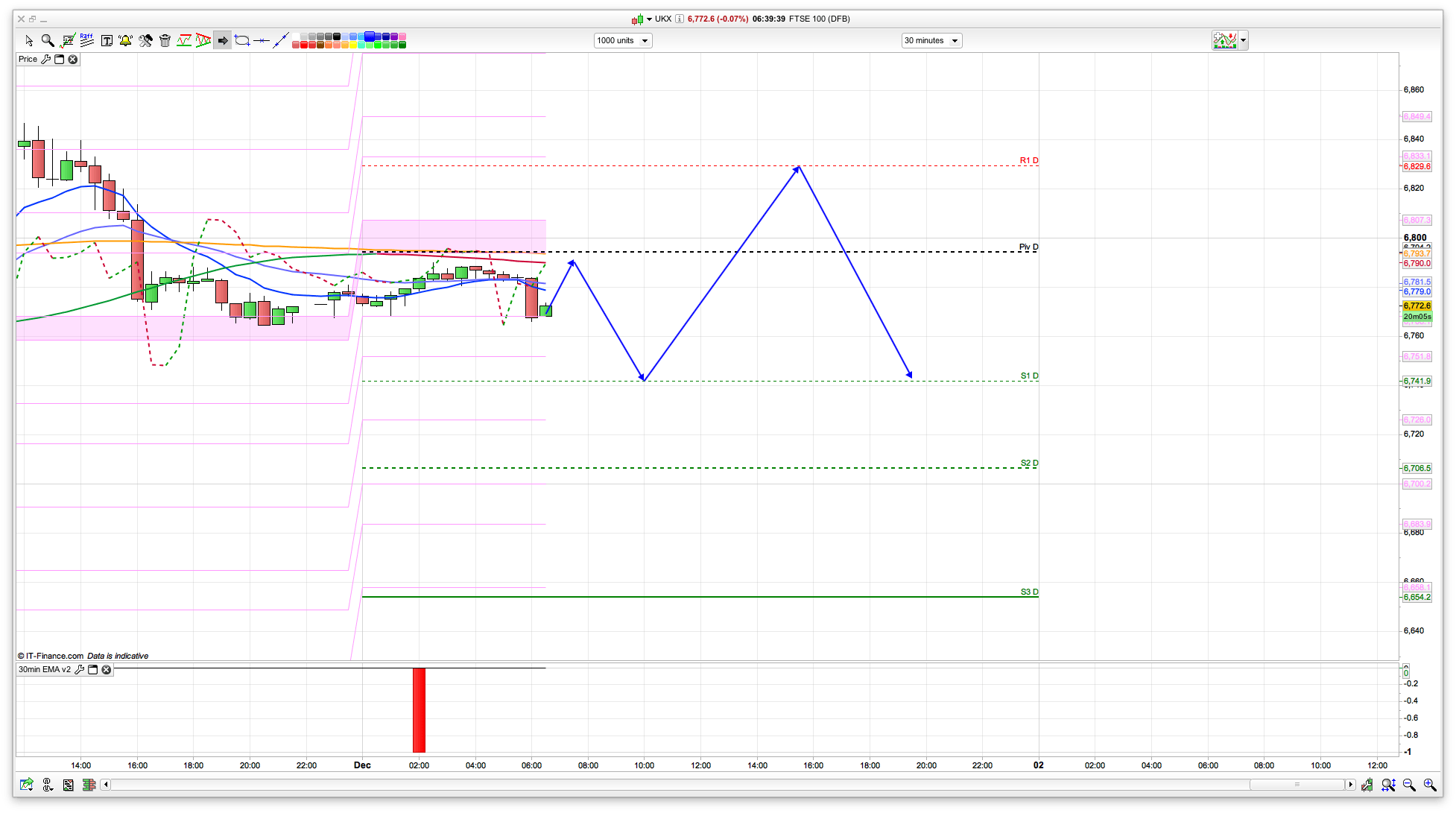

There are a cluster of resistance levels around the 6790 to 6800 area that is probably worth a short from initially, We may well get an initial rise as the market opens as it’s the start of a new month so an influx of new money. If the bulls manage to push above 6800 (and they will be keen to do so) then the top of the 10 day Bianca is slightly lower today at 6849. The OPEC driven move yesterday scuppered a few levels so it might take a few sessions for things to settle down, as currently the 2 hour went bullish on yesterday’s rise, then the drop back to the support at 6785 failed and we dropped slightly below.

I have plotted a drop back from the 6790 area to 6741 before another climb, mainly as the 6730 area held as decent support on the first test earlier this week, so may well again. 6741 is S1 for today so slightly above that level. A break of this 6730 will see a trip to 6660 though I am thinking. The FTSE continues to be slightly choppy, but its certainly looking like the 6880 level is going to be set as the most recent high and we are on a leg down from there. Shorting the rallies still for me feels the best play.

Key area on #FTSE here at 6740. Breaks and we go to 6660

I think first Nick it will bounce back to mid 6750s before falling again tomorrow

Yes, 6711 is the 20 day Bianca channel. So bounce here, then reload shorts for the run to 6660

Thought that 6711 might put up more of a fight, 6660 now then

Didn’t get to 6660, or will it later? Started a bounce.

Probably, SP has dropped nicely off the 2204 level (short from there currently)