FTSE 100 Support 6951 6932 6915 6910 6850

FTSE 100 Resistance 6968 6972 7005 7024 7031

Good morning. A fairly slow day on the FTSE for most of yesterday, only really livening up towards the end of the session with the US influence. The bulls didn’t manage to reach the 7000 level, though the support area held for most of the day so at least the long got a few points. Gold was also fairly slow, eventually closed the long at 1274, though overnight has seen a bit more bullishness with a rise to 1280. Maybe just needed a lot more patience on that trade! Overnight, the bulls have brought FTSE 100 futures up from the 6930 area to 6960, mainly off the back of a rise in Chinese manufacturing. Unsurprisingly and as we spoke about in the live trading room yesterday Mark Carney has decided to stay till June 2019, all that bluster was just to raise his profile.

US & Asia Overnight from Bloomberg

Asian stocks reversed losses and industrial metals rallied after an unexpected pickup in manufacturing in China, the biggest driver of global economic growth. Australia’s dollar surged and the yen held steady following central bank meetings.

The MSCI Asia Pacific Index swung to a gain as China purchasing managers’ indexes rose to two-year highs and topped the most optimistic estimates in Bloomberg surveys. The Aussie strengthened versus all of its peers and Australian bonds fell after the monetary authority refrained from cutting interest rates and signaled reductions are unlikely. Copper and nickel gained for a seventh day, while oil rose following its steepest slide in a month.

Signs of improvement in China are welcome after global equities in October had their biggest monthly loss since January, weighed down by an underwhelming batch of corporate earnings and indications that major central banks are starting to turn away from ultra-loose policies. While the Federal Reserve is forecast to leave interest rates unchanged at a review this week, futures traders see a 71 percent chance of a hike before the year is out and the Nov. 8 presidential election in the U.S. is giving further cause for caution.

Stocks

The MSCI Asia Pacific Index was up 0.2 percent as of 2:25 p.m. Tokyo time, after earlier falling as much as 0.3 percent. Hong Kong’s Hang Seng Index and the Shanghai Composite Index both rose for the first time in at least a week after China’s official manufacturing purchasing managers’ index as well as a private measure both climbed to 51.2 for October, above the 50 threshold that marks the dividing line between expansion and contraction.

“The market has turned more positive and confident that China’s economy will stabilize in the fourth quarter,” said Linus Yip, a Hong Kong-based strategist at First Shanghai Securities Ltd. “After a correction in Hong Kong and being at a relatively low level, the market needed some stimulus to gain power and the China figures helped trigger that.”

Macau casino stocks advanced as data showed the city’s gaming revenue climbed for a third month in October, with Sands China Ltd. rallying by the most since September. Sony Corp. dropped as much as 2.4 percent after the company cut its annual operating profit forecast by 10 percent on Monday. Panasonic Corp. slid by the most since June after slashing its projection by 21 percent.

Futures on the S&P 500 Index added 0.4 percent, while contracts on the U.K.’s. FTSE 100 Index were little changed ahead of the release of American and British manufacturing gauges. BP Plc, Royal Dutch Shell Plc and Pfizer Inc. are among companies posting results.

Currencies

The Aussie strengthened as much as 0.7 percent versus the greenback. Twenty-two of 28 economists surveyed by Bloomberg forecast the Reserve Bank of Australia would keep its benchmark interest rate at a record-low 1.5 percent, while the other six forecast a quarter-point reduction. RBA Governor Philip Lowe expressed concern about rising property prices and said the economy is expanding at close to its potential rate with inflation seen picking up gradually over the next two years.

“We think the RBA is likely on hold for the foreseeable future,” said David Forrester, a foreign-exchange strategist at Credit Agricole SA’s corporate and investment-banking unit in Hong Kong. “We don’t think they’ll cut in 2017.”

The yen weakened less than 0.1 percent after the BOJ kept its monetary policy stance unchanged, as forecast by the vast majority of economists in a Bloomberg survey, and pushed back the projected timing for reaching its 2 percent inflation goal to the fiscal year starting April 2018. The central bank re-set its monetary program in September to target yields on Japanese government bonds following a comprehensive policy review.

“It looks as though the least anticipated BOJ meeting of the year will quite rightly produce the least market impact,” said Sean Callow, a senior strategist at Westpac Banking Corp. in Sydney. “Six weeks after taking the big step to target JGB yields is not the time to make yet another change, but extending the likely time to reach 2 percent inflation is at least admitting reality.”

The Bloomberg Dollar Spot Index stayed near its highest level since March after data on Monday showed U.S. consumer purchases rose in September by the most in three months as incomes grew, bolstering the case for the Fed to raise interest rates.

Commodities

The Bloomberg Commodity Index rose 0.4 percent, after ending the last session at its lowest level since Sept. 27.

Copper advanced to a three-month high in London, while aluminum held near its best close since June 2015 following the upbeat manufacturing figures for China, the world’s biggest user of industrial metals. Zinc climbed to a fresh five-year high as steel gained in Shanghai.

Crude oil added 0.2 percent to $46.95 a barrel in New York, after tumbling 3.8 percent on Monday. The Organization of Petroleum Exporting Countries ended two days of talks on Saturday without any commitments being made to limit oil output by its members or major producers from outside of the group. Goldman Sachs Group Inc. said it looks increasingly unlikely that a deal will be agreed at an OPEC meeting this month, adding that failure would warrant crude prices in the low-$40s.

Bonds

The yield on Australia’s 10-year bonds increased four basis points to 2.39 percent. The probability of an interest-rate cut by mid-2017 sank below 30 percent in the swaps market after the RBA meeting, from 42 percent on Monday.

The yield on U.S. Treasuries due in a decade increased by two basis points to 1.85 percent. Similar-maturity Japanese government bonds yielded minus 0.05 percent, unchanged from Monday. [Bloomberg]

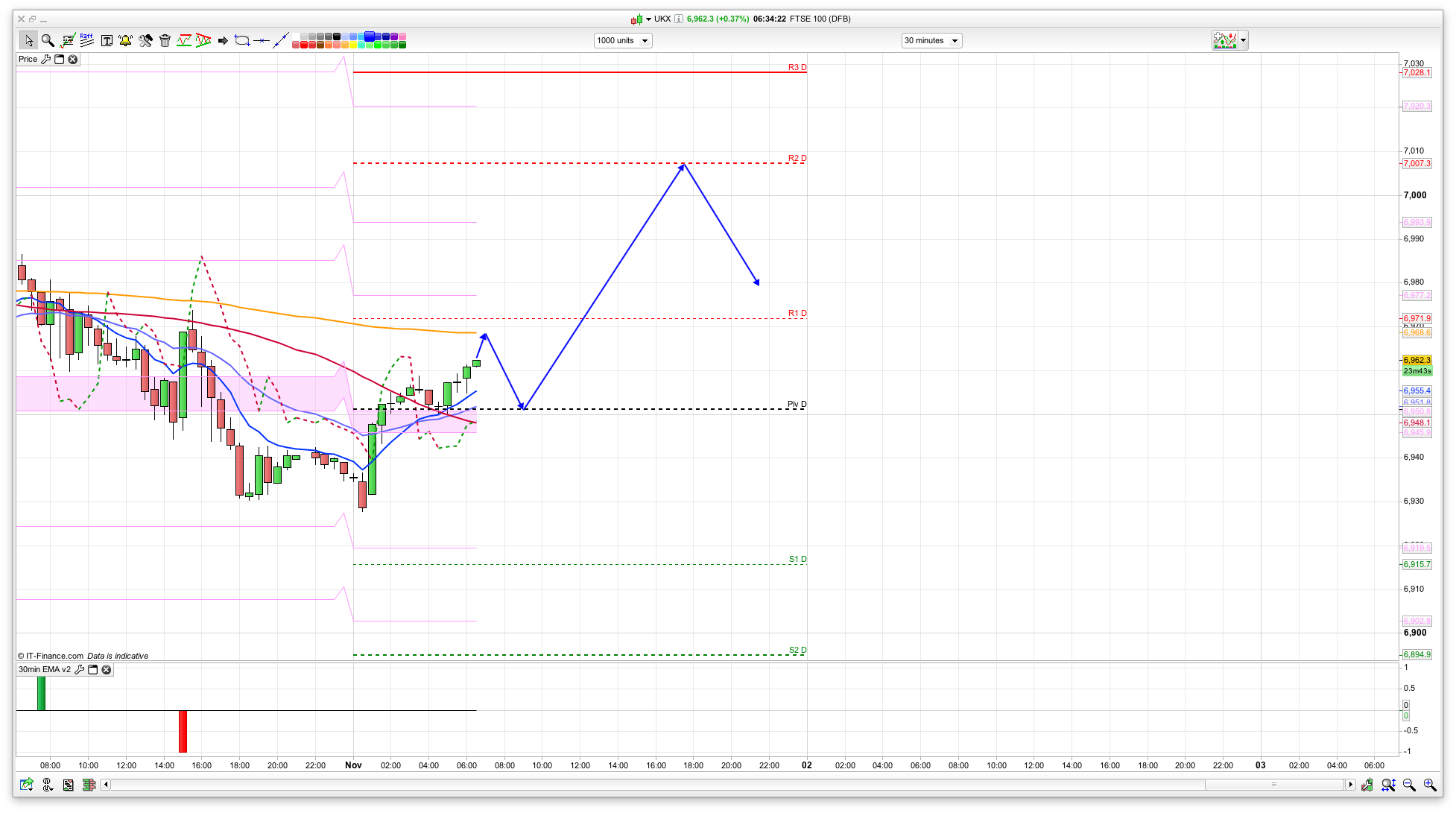

FTSE 100 Outlook and Prediction

Start of yet another new month as the year zips by, so we should see some optimism, at least initially. The daily pivot is 6952 and also the 100 Hull moving average on the 2 hour here so if there is an initial dip back this looks a good area to go long. The Bianca 10 day channel has resistance at 7005 for today, with the 20 day just above at 7031, so a level likely to be seen of the bulls break 7005. For the bears, they need to break that 6928 level which has held twice now – Friday last week and overnight – which would lead to 6910 for the 20 day Bianca channel bottom, then 6850.

For today, I think the pivot area will hold initially, and the bulls have managed to bring the FTSE 100 back up off that support so will be keen to keep it going. New monthly money coming in, plus clarity with Carney at the BoE will help too. So, fairly simple plan really but keep watching the 6925 level – if that breaks then the bears are gaining momentum. Cautiously optimistic/bullish is how I feel for today.

Morning all, back after a week away. I went short at 6984.8 this morning based on rsi levels on 30 min chart which were in mid 70s and yesterdays intraday high of 6986 acting as resistance. targeting 6884.8. Looking good so far

What a great prediction!!! I would quit my day job if I were you….well done sir.

Morning guys.

Pretty half hearted gap up open for a nice short and a lousy rejection candle.

Stuck now with a dodgy 38 long looking for the bounce which doesn’t look like coming.

If we break 48/50 may have another 12 up in it, but looks like sideways for a while.

dumped at 57 a bit hot, pullback to 48/50 might be a good re entry

Flirting with ~50% correction and overbought in low 60’s but looking too strong to short atm

Looking a bit tired in the low 70’s, trying a little 10 either way short.

Not sure what’s happening with the forum posts clock….

and +13 for a bounce and re short.

Hmm, no bounce, all the way back down again methinks

tfmp, Looks like its heading for 6930 again. I’m still hanging in there

Got the bounce in the end and nicked 10.

Turning into a bit of a pennant, resolving one way or the other off 64 within the hour.

Hands being sat on now.

So here we are, boxed into the apex, which way’s it going to jump? Fake move first probably…

Pretty boring after that big build up, they usually provide a bit of fun.

Doesn’t really look like it wants to go anywhere much, especially not down, although we’re getting near the DOW open.

Si, look away…

B*tcoin $730, going like a train. 🙂

Good call the other day!

I saw that! Amazing, well done! I’ve been quiet, I’m sure everyone got bored of me calling a crash… I’m still short dow, long gold.

Not for a moment suggesting longing Bitcoin around here, but I reckon $1000 is on the cards sooner rather than later.

I don’t like this, it seems to be going down, using what i can only suspect, the powers of the dark side.

bought back out at 6954, will do for today. 30 points aint bad

30 points is great, but I just logged back in to congratulate you on your 10.15 call of the 880’s today…..

Yeah wish I had stuck to my trade plan. It started rising and fear of turning a winning trade into break even took over. Should of stuck to the plan!

How is this still going down?

Will bounce heavily about 6.15.

Err can someone pinch me! I’m in bear heaven

That said I am partial bull to catch retrace.