FTSE 100 Support 6855 6830 6825 6810

FTSE 100 Resistance 6895 6901 6924 6933 6948 6977

Good morning. The early rise yesterday was pretty short lived as the bulls failed to reach the 7000 level again, and a poll was released that put Donald Trump ahead for the first time since May. That saw markets react to the downside and continue to slide all day, with the Dow breaking below 18000 and the SP breaking 2100. Both rallied a little bit at the end of the day though. The growing possibility of a Trump presidency has made investors nervous and they expressed their worries by selling stocks and selling the U.S. dollar. When Trump wins it’s really going to slide! Gold continues its rise from the 1250 level now, and looks to be on track for 1300+. Resisting the urge to cash in those long term longs from 1250!

US & Asia Overnight from Bloomberg

A global equities selloff deepened in Asian trading and Mexico’s peso weakened as polls indicated a tightening race ahead of next week’s American presidential election. The yen gained with the Swiss franc and gold as investors favored haven assets.

The MSCI Asia Pacific Index dropped by the most since September and futures signaled further losses for U.S. equities after the S&P 500 Index sank to its lowest since July. The yen rose for a second day, while the Swiss franc and gold were near their highest levels in almost a month. New Zealand’s dollar strengthened as jobs data damped prospects for interest-rate cuts in the nation and U.S. Treasuries edged higher ahead of a Federal Reserve policy decision. Crude oil fell after a report showed American stockpiles expanded.

An ABC News/Washington Post tracking poll on Tuesday showed Republican Donald Trump with 46 percent support to Democrat Hillary Clinton’s 45 percent, putting him ahead for the first time since May. Poll aggregator FiveThirtyEight estimates that the chance of a Clinton victory has fallen by about 10 percentage points in the past week to 72 percent and a Bank of America Corp. index tracking volatility expectations in equities, bonds, currencies and commodities rose for five days through Monday, the longest run of increases since before the British vote to quit the European Union.

“The markets’ anxiety levels have moved up a gear,” said Chris Weston, Melbourne-based chief market strategist at IG Ltd. This “suggests the bears have the upper hand, with the buying drying up and funds keeping their cash deployed for more certain times,” he said.

While the Fed is expected to leave policy unchanged when a two-day meeting concludes Wednesday, futures indicate a 68 percent chance interest rates will be raised in December. Bloomberg’s dollar index retreated over the last three days as some analysts said a Trump victory could spur volatility in financial markets and reduce the odds of borrowing costs being hiked.

Stocks

The MSCI Asia Pacific Index declined 1.3 percent as of 1:36 p.m. Tokyo time. Japan’s Topix index slid more than 2 percent, retreating from its highest close since April before the nation’s financial markets shut on Thursday for a holiday, and South Korea’s Kospi index fell to its lowest level in almost four months.

“The Trump risk is in revival,” said Chihiro Ohta, a Tokyo-based senior strategist at SMBC Nikko Securities Inc. “With Trump, there always follows an uneasiness over whether policies will be managed properly in the U.S., and given the holiday tomorrow in Japan, there’s no need to build positions at an uncertain time like this.”

Sony Corp. sank to a two-month low after the Japanese electronics maker reported a quarterly profit that missed analysts’ estimates. Sumitomo Electric Industries Ltd. tumbled more than 10 percent after the company lowered its full-year earnings target by 15 percent. Standard Chartered Plc plunged by the most since June in Hong Kong after reporting a lower-than-expected profit and revenue declines for all four of its divisions.

Futures on the S&P 500 Index fell 0.3 percent after the underlying gauge slipped 0.7 percent in the last session. Alibaba Group Holding Ltd. and Facebook Inc. are among companies reporting earnings on Wednesday.

Currencies

The yen climbed 0.4 percent to 103.71 per dollar, after surging 0.6 percent in the last session. The franc rose 0.2 percent following a 1.4 percent jump that marked its biggest gain in about five months.

Mexico’s peso slid as much as 0.8 percent to its weakest level since Oct. 7. The currency tends to lose ground when support builds for Trump, who has said he would revisit the North American Free Trade Agreement that governs commerce between the U.S. and Mexico. The Republican candidate’s prospects have improved since it was announced Friday that the Federal Bureau of Investigation had reopened a probe of Clinton’s use of private e-mail while Secretary of State.

Before the FBI announcement, “the market had pretty much priced out most of the risk of Donald Trump becoming president,” said Lee Hardman, a currency strategist at Bank of Tokyo-Mitsubishi UFJ Ltd. in London. “Obviously, the markets had to reassess that view now.”

The Kiwi gained as much as 0.6 percent after New Zealand’s jobless rate unexpectedly fell to the lowest level since 2008. A tightening labor market could help Reserve Bank of New Zealand Governor Graeme Wheeler lift inflation back to the middle of his 1-3 percent target band, negating the need for further policy easing.

Commodities

Crude oil fell 0.8 percent to a one-month low in New York after industry data showed American inventories increased by 9.3 million barrels last week. Organization of Petroleum Exporting Countries members Libya and Nigeria are boosting output, providing a challenge to the group’s effort to finalize an agreement to curb production and stabilize prices.

Gold added 0.4 percent, after surging 0.9 percent on Tuesday. Copper snapped a seven-day winning streak in London and zinc retreated from a five-year high.

Rubber dropped by the most in two weeks in Tokyo after a report showed U.S. auto sales cooled in October.

Bonds

Ten-year bonds rose in Australia, Singapore and South Korea. The yield on U.S. Treasuries due in a decade fell one basis point to 1.81 percent, after touching a five-month high of 1.88 percent in the last session. It’s unlikely the rate will climb too far past 2 percent anytime soon given how the American economy is performing, according to Jim Caron at Morgan Stanley Investment Management, which oversees $406 billion. “Nobody really believes that rates can just rise very very quickly, or that bond prices can fall off a cliff,” Caron, who is based in New York, said Tuesday on Bloomberg Television. “You’re not seeing the growth. You’re not really seeing the inflation.”

New Zealand’s 10-year bond yield increased by three percentage points to 2.77 percent. While investors are almost certain the central bank will cut its benchmark interest rate to a record low 1.75 percent at a policy meeting next week, swaps prices indicate that the chance of a further reduction by the end of next year has dropped to about 11 percent, from 36 percent a month ago. [Bloomberg]

FTSE 100 Outlook and Prediction

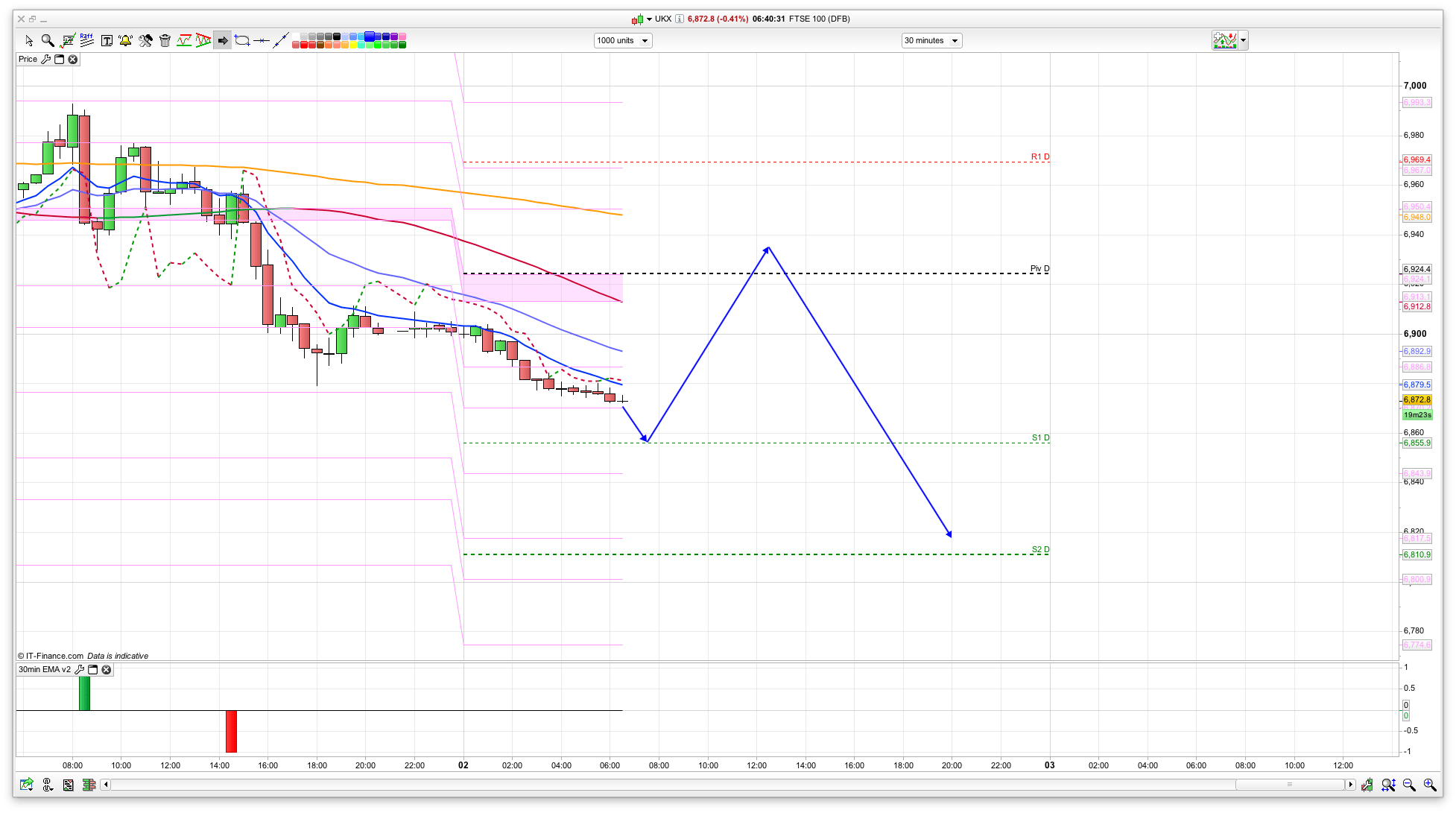

That poll result yesterday scuppered my long plan for the day, and all the while Trump looks like winning investors are going to remain spooked (insert Halloween pun here!). As such, the 2 hour chart has now gone bearish, with resistance at 6933, so this area looks like a decent short entry. We are certainly going to see increased volatility leading up to the election and action after depends on the result.

We have initial support today at S1 at 6855 and I think we might see a bit of a bounce from this level to test the bottom of the Bianca channels around the 6900 level. We may even mange a climb to the 6935 area which is where the shorts kick in. A bounce at 6850 would tally with a bounce on the S&P from 2100 too I think. So, thats the plan really, but if 6850 breaks then we are looking at 6830 and then 6800 as the next supports. The bulls might be a bit tentative to really push it higher now, unless another poll comes out with Clinton ahead. But as with our referendum and Brexit polls they always seem to show everything neck and neck (even when they aren’t!). Polls eh!

Morning guys.

I don’t normally take much of an overall view, just trade reactively, but this morning I’m working off the long side and buying dips.

Although recent low support is broke, I can’t see melty melty unless DOW inspired later which, as Nick says, depends on the Trump ratings. I can see the overnight cash gap to 6900 being closed and on to 920ish depending on the action.

On the daily we’re around 50% pullback of the 6640/7130 Sept/Oct rise and burrowed slightly into the previous triple top support at 6930. Daily RSI is also similar to the readings at that 6640 low.

Short squeeze coming?

Something to be borne in mind, especially given recent antics.

I just don’t see any point in being short around here, just bad r/r.

The Black Swan is Trump, I could see a Brexit type reaction to him winning, but only when/if confirmed.

Well, drifted/struggled up to 900, got rid of some, looking to replace soon, nothing huge.

Could repeat the Brexit move exactly – dip on news then rally for a month

I am long now on Dax, Dow And mixed on FTSE.

I think it will rally after election so long as trump fails.

I’m long more worryingly on oil.

hey morko – I’m hoping you’re long oil from 45 bucks ? 🙂

Hi, no 51!!!! But averaged in and scalped so looking ok.

Made a killing the last few days so I can afford to hold onto one or two bad trades.

I’m long heavy at 6850, and long on Dax and Dow.

In all sorts gold, gbp, oil but averaged an incredible 500 Pts a day last few weeks. Record at 746 yesterday

hey all

Don’t think I’m brave enough to go long today, though double bottom on dax 5m and higher lows being made on dow – close over 18030 would be nice.

If I had to flip a coin, I think I’d prefer to be short right now, but thats on the basis of making up my own sense of panic about things at the moment.

fomc at 18:00 could be fun.

Wonder if its just going to range around and not do much until then (famous last words?)

Pretty lacklustre isn’t it? I’ve got some long average c 60, may keep it for a change.