FTSE 100 Support 6821 6800 6757 6696

FTSE 100 Resistance 6872 6875 6878 6922 6944 7003

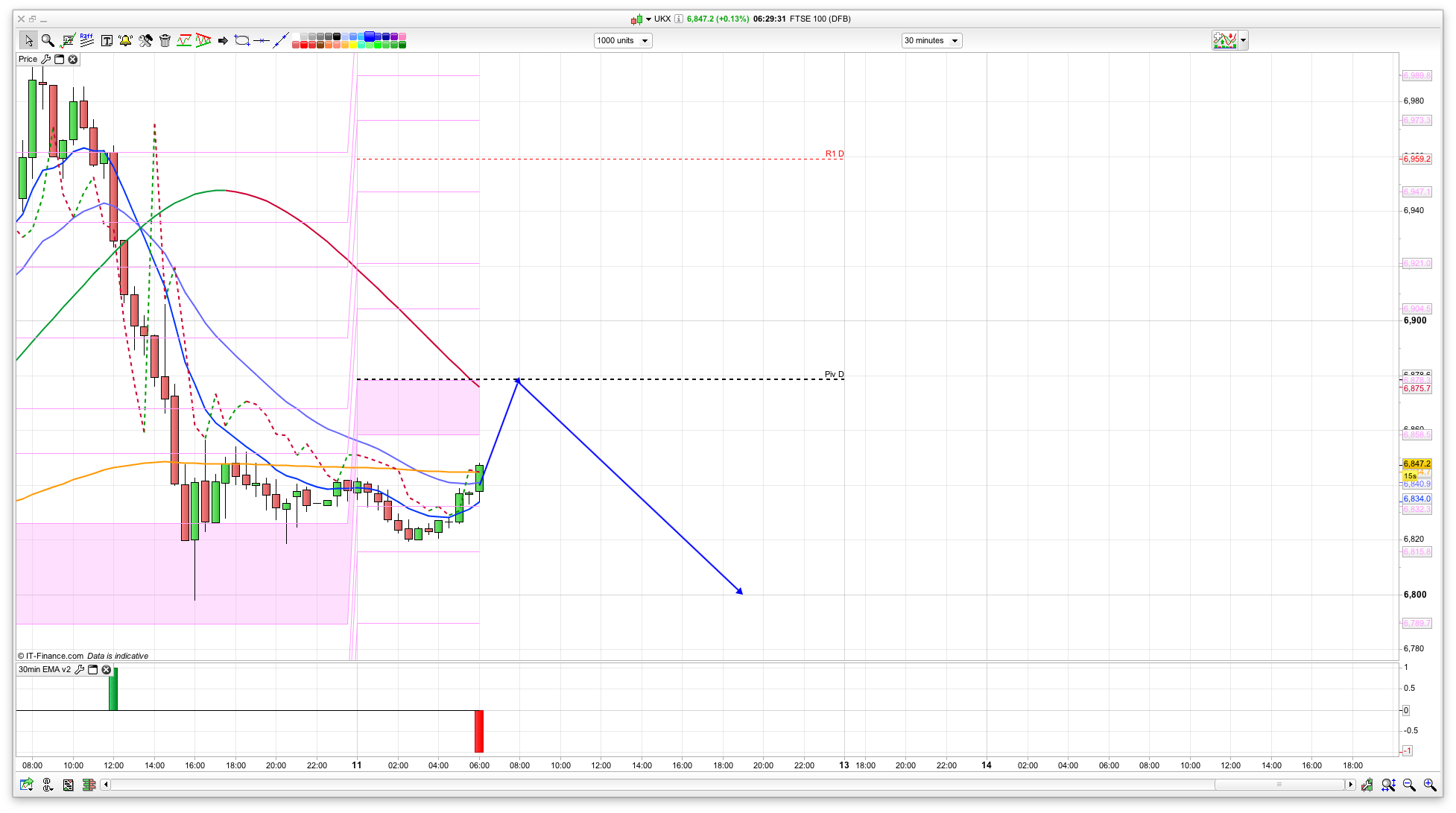

Good morning. Well we got the rise and dip yesterday though I didn’t expect it to get as high as 7000 – just entered the short a bit early at 6960, but it dropped all the way down to 6800 before a late bounce. The hangover kicked in yesterday for the bulls that had chased it up the day before. All still pretty volatile while the dust settles since the vote – a 200 point range yesterday for example on the FTSE. To end the week, we have resistance on the 2 hour chart at 6875 so may well see a pull back from this area.

US & Asia Overnight from Bloomberg

An emerging-markets selloff deepened amid concern developing economies will face capital outflows and weakening exports once Donald Trump is in The White House, while Treasuries capped their worst week since 2009 before a U.S. holiday on Friday.

MSCI gauges of emerging-market equities and currencies sank to four-month lows since the election of Trump, who pledged to restrict imports and add fiscal stimulus that’s seen hastening interest-rate hikes by the Federal Reserve. More than $1 trillion was wiped off the value of bonds this week, something that’s happened only once before in the last two decades, and Bloomberg’s dollar index rallied the most since May 2015. Shanghai shares were poised to enter a bull market, while industrial metals were headed for their biggest weekly jump in five years.

Developing-nation assets have been roiled since Trump’s surprise win in Tuesday’s vote and central banks in India and Indonesia were said to have intervened Friday in support of their currencies. Futures indicate an 80 percent chance that the Fed will raise rates next month and expectations are building for more increases. Ten-year Treasury yields have climbed above 2 percent for the first time since January amid speculation the president-elect’s plans to cut taxes and boost spending will widen the U.S. budget deficit and stoke inflation.

“Rising U.S. yields will cause volatility in capital flows into emerging markets, and with the Fed still likely to hike rates in December, the risk is for further outflows,” said Khoon Goh, head of Asian research at Australia & New Zealand Banking Group Ltd. in Singapore. Trump’s plans to revisit trade agreements is “is also a factor,” he said.

Stocks

The MSCI Emerging Markets Index dropped 1.5 percent as of 2:41 p.m. Tokyo time. The Jakarta Composite Index tumbled by the most in a year and the Philippine Stock Exchange Index was headed for its biggest loss since January. Benchmarks in Argentina, Mexico and Brazil plunged more than 3 percent on Thursday.

The Shanghai Composite Index gained 0.8 percent, taking the advance from its Jan. 28 low to more than 20 percent. This quarter’s rally has been led by commodity producers and construction companies as the government boosts spending to bolster growth, driving raw-materials prices higher amid a clampdown on speculation in the housing market. Friday is Singles Day, the Chinese e-commerce event that has morphed into the biggest online shopping event in the world.

“Liquidity is abundant and property curbs will prompt more money to flow into stocks, which look undervalued relative to homes in large cities,” said Li Jingyuan, general manager at Shanghai Bingsheng Asset Management.

Futures on the S&P 500 Index fell 0.1 percent, after the underlying benchmark capped a 4 percent weekly advance, its best performance in two years. U.S. banks and health-care shares surged last session on bets a Trump administration will roll back regulatory scrutiny of the industries. Utility and real estate stocks tumbled as higher bond yields damped demand for the shares’ relatively high dividend payouts.

Currencies

The MSCI Emerging Markets Currency Index fell 0.4 percent. Indonesia’s rupiah and South Korea’s won sank about 1 percent versus the dollar to their weakest levels in more than four months. China’s yuan was set for its steepest weekly drop since January.

Malaysia’s ringgit slipped to its lowest level since January, prompting the central bank to say it may intervene at times of extreme volatility. The nation’s economy expanded by more than economists forecast in the last quarter, data showed Friday.

Latin American currencies tumbled Thursday on concern Trump’s administration could usher in a host of protectionist measures after he campaigned on a pledge to protect U.S. workers and companies from unfair trade deals. A trade war would be a blow to economies such as Mexico, which gets 80 percent of its overseas sales from the U.S. and has seen its currency plunge more than 7 percent this week.

The Bloomberg Dollar Spot Index held near an eight-month high, having surged 2.3 percent this week. The yen pared its weekly loss to 3.2 percent.

“The dollar is up against most major currencies supported by an upward revision to U.S. interest expectations and focus on President-Elect Donald Trump’s pro-growth and inflationary economic policies,” said Elias Haddad, a senior currency strategist at Commonwealth Bank of Australia. “Trump’s economic policies will force the Fed to raise the Funds rate at a faster pace than otherwise, which is dollar bullish.”

Bonds

The global debt selloff extended into Friday, with yields on 10-year Australian government bonds surging seven basis points to 2.57 percent, the highest since May.

Yields on U.S. 30-year bonds, which are more sensitive than shorter maturities to the outlook for inflation, have jumped almost 40 basis points since last Friday and a $15 billion auction of the tenor on Thursday showed waning appetite for the securities. The Bloomberg Barclays U.S. Treasury Index slid 1.85 percent this week, its biggest loss since 2009.

“We do view the election of Donald Trump as a game changer,” said Adam Donaldson, head of debt research at Sydney-based Commonwealth Bank of Australia. “The strong bias toward fiscal expansion and inflationary policy represents a stark change to the malaise of recent years. This opens the door for the Fed to hike in December, but also more quickly in 2017 and 2018 than previously expected.”

The market value of Bank of America’s Global Broad Market Index, which tracks more than 24,000 bonds around the world, has declined by $1.14 trillion this week to $48.1 trillion. The only previous week it fell more than $1 trillion was in June 2013, when the Fed was threatening to reduce debt purchases and triggered a bond selloff that became known as the “Taper Tantrum.”

Commodities

A Bloomberg gauge of industrial metals jumped more than 8 percent this week, the best performance in five years, on optimism Chinese demand will firm at the same time as Trump steps up spending on U.S. infrastructure. Zinc is the highest it’s been since April 2011 in London, while copper, aluminum and nickel are all around their best levels in more than a year.

Gold pared its weekly loss to 3.3 percent, having lost ground amid expectations inflation and interest rates are headed higher in the U.S. under a Trump administration. Fed Bank of St. Louis President James Bullard on Thursday signaled a December rate increase is likely.

Crude oil fell 0.3 percent to a one-week low of $44.52 a barrel in New York. Prices may retreat amid “relentless global supply growth” unless the Organization of Petroleum Exporting Countries enacts significant output cuts, the International Energy Agency said Thursday. The group failed last month to agree on quotas for member countries, something that must be done if proposed reductions are to be finalized at a meeting on Nov. 30.Palm oil jumped as much as 6.7 percent on Friday to the highest level since 2012 in Kuala Lumpur, buoyed by the weaker ringgit and falling output. Rubber rose to its highest intraday level since April in Tokyo, having jumped 17 percent this week amid speculation Trump’s policies will boost car sales in the U.S. [Bloomberg]

FTSE 100 Outlook and Prediction

For today we have resistance at 6875 to start with and the bounce from 6800 is holding well, so I expect we will get this level. The SP has resistance at 2178 which might well tally with the same sort of rise and dip scenario. Above 6875 then we have the Bianca channels at 6922 and 6944, with 7003 above that and a double top with the recent high. I am not sure the bulls will be powerful enough today to push past that but if they do then 7123 is still viable which was the most recent highest high. Support wise, 6800 to tally with a double bottom with yesterday, then the S1 level at 6757. The closet Bianca channel support is 6696, while the Raff channels are down at 6500. Resistance from the Raff’s is at 7100 also.

So, for today I am expecting a similar pattern to yesterday with a rise and dip and it will be interesting to see if there is a reaction at 6875. The daily coral has gone red now for the first time in a while (last time was May when we dipped to 5775 on Brexit voting), so I do think for the bigger picture that we are going to get pretty bearish again, probably in January next year. Both daily raff channels are pointing down again for the moment.

Dax and Dow stick with it: don’t ease off. If I didn’t close my loss on Wed. my account would be wiped out.

Morning all, had a bit of fun yesterday and did pretty well during FTSE hours and then gave it all back by 8pm on the Dow. Hey ho.

Currently still looking to be a bit short but interested in the dow/ftse split at 12,000 odd, just shorted that at 12,000. Also, been watching people talk about gold, it seems to have a pretty good bottom at around 1250 so I’ve just had a few at 55, looking for 80 ish.

Good luck all.

Fib supports at 6760 and 6700

https://dl.dropboxusercontent.com/u/20168894/Indices/Fibs.png

Added to gold at 45. Dunno why….guess I’ll find out!!

and chopped the lot at 36. That has made a bit of a dent!