FTSE 100 Support 6766 6737 6707 6680 6610

FTSE 100 Resistance 6814 6826 6838 6897 6909 7002

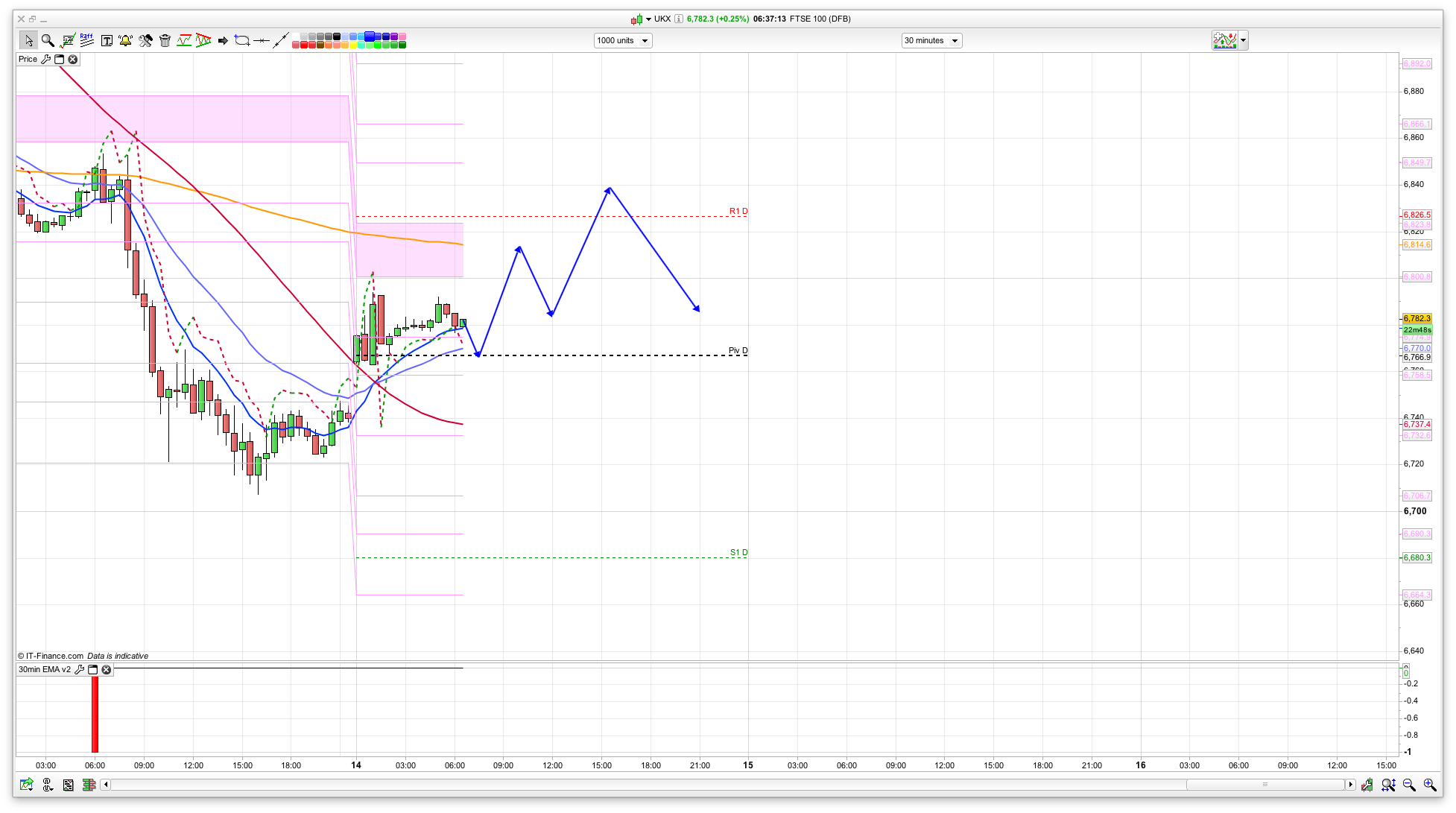

Good morning. I hope you had a good weekend. I mentioned on Friday that we might be in for a bit of a rise after the current leg down has shaken out the weak longs and we have 6760 and 6700 as fib retracement levels to watch. We dipped to just above the 6700 level on Friday and have subsequently bounced pretty well, with futures steadily climbing overnight. 6760 held for a short while but was broken in the end. However, for the bulls, there is resistance at 6838 to jump. News was mostly about Trump’s victory as you would expect, with last week ending pretty positively for indices, but not so much for gold – reversals on both after the move on election night when gold was 1330 and the FTSE 100 was 6500!

US & Asia Overnight from Bloomberg

- U.S. stock futures rise after S&P 500’s best week in two years

- Topix advances to six-month high as Japan GDP beats estimates

Routs in global bonds and emerging markets intensified, while the dollar climbed with U.S. equity futures and industrial metals as investors position for the wave of fiscal stimulus that Donald Trump plans to unleash.

Sovereign bonds in the Asia-Pacific region slid with U.S. Treasuries, extending a record debt selloff, amid speculation President-elect Trump’s pledge to boost infrastructure spending will trigger U.S. interest-rate hikes as economic growth and inflation pick up. Bloomberg’s dollar index climbed to a nine-month high as an earthquake weighed on New Zealand’s dollar. Japanese shares were set for their best close since April after gross domestic product data, while shares in developing nations fell. Copper surged to a 16-month high and gold slumped.

Trump’s election victory continues to send shockwaves through global markets, having already led to $1.2 trillion being wiped off the value of bonds worldwide last week as equities added about $1 trillion and industrial metals soared by the most in four years. Emerging markets are being hit by an exodus of capital as speculation builds that the U.S. is headed for an era of rising interest rates and more protectionist trade policies.

“In the short-term the election of Donald Trump as president is causing a bit of uncertainty and markets tend to overreact to that,” said Shane Oliver, Sydney-based head of investment strategy at AMP Capital Investors Ltd., which manages about $121 billion. “I suspect the dust will settle down in the next couple of months and this sort of market overreaction will provide opportunities.”

Bonds

Ten-year U.S. Treasury yields increased by five basis points to 2.20 percent as of 1:35 p.m. Tokyo time, the highest since early January. They surged 37 basis points last week, the most in three years, amid speculation fiscal stimulus planned by Trump will widen the budget deficit and stoke inflation.

Federal Reserve Vice Chairman Stanley Fischer said Friday that the central bank was close to achieving its goals of maximum employment and price stability, strengthening the case for an interest-rate increase. Pacific Investment Management Co. says long-term yields may have bottomed out and predicts three rate hikes by the end of next year. Futures prices indicate an 84 percent chance of a tightening at the December policy meeting.

“Yields will continue to rise over the next year,” said Hiroki Shimazu, an economist and strategist at the Japanese unit of MCP Asset Management in Tokyo. “The fundamentals are very strong, particularly in the U.S. There are some signs of higher inflation pressures. Trump is pushing this phenomenon. ”

Government debt extended losses across the Asia-Pacific region, pushing benchmark bond yields in Australia, New Zealand and South Korea to their highest levels since at least April. Thailand’s 10-year yield jumped by the most since May after foreign investors pulled a record 27 billion baht ($763 million) from the nation’s bond market on Friday, while similar-maturity debt in China dropped for a seventh day, the longest losing streak in three years.

Currencies

The Bloomberg Dollar Spot Index climbed 0.3 percent. The euro fell versus the greenback for a sixth day, its longest run of declines in six months, and the yen sank as much as 0.9 percent to its weakest level since early June. Japan’s economy expanded by an annualized 2.2 percent in the last quarter, exceeding the 0.8 percent expansion forecast in a Bloomberg survey and easing pressure on the Bank of Japan to add stimulus.

“The dollar is strengthening along with the rise in U.S. yields, reflecting expectations for economic expansion from fiscal spending,” said Yunosuke Ikeda, Nomura Holdings Inc.’s head of Japan foreign-exchange research in Tokyo. “Japan’s 2 percent growth can be used as a reason for the BOJ not lowering interest rates for a while.”

The kiwi dropped to a one-month low after a massive earthquake rocked New Zealand early Monday, causing widespread damage. South Korea’s won dropped to its weakest level since June amid growing calls for President Park Geun-hye to be impeached over an influence-peddling scandal, while China’s yuan slid to its weakest level in six years.

Mexico’s peso rebounded 0.7 percent after a Trump adviser hinted in an opinion piecein the Financial Times that the the president-elect is open to negotiations before imposing import barriers. It tumbled 12 percent in the three days following the election of Trump, who had campaigned on promises to tear up the North American Free Trade Agreement, crack down on illegal immigration, and build a wall along the southern U.S. border.

Stocks

S&P 500 Index futures rose 0.4 percent, pointing to further gains after the underlying benchmark had its biggest weekly jump in two years. Stocks in the developed world outperperformed bonds last week by the most since 2011, based on the MSCI World Index of equities in developed nations and the Bloomberg Barclays Global Aggregate Index.

Japan’s Topix index climbed 1.6 percent, while benchmarks in Hong Kong, Indonesia and Singapore slid to their lowest levels in more than three months. Markets in India are closed for a holiday.

The Shanghai Composite Index rose to a 10-month high and a gauge of Chinese shares in Hong Kong fell to a three-month low after a raft of Chinese data suggested the economy held ground last month following new measures to cool property markets in almost two dozen big cities. Industrial production rose 6.1 percent from a year earlier in October and retail sales climbed 10 percent.

New Zealand’s S&P/NZX 50 Index added 0.6 percent, led by a 4 percent jump in construction company Fletcher Building Ltd. following the earthquake.

Commodities

Copper rallied as much as 3.4 percent in London. It surged 11 percent last week as Trump, has pledged to spend more than $500 billion rebuilding U.S. infrastructure, pulled off his surprise win in the U.S. election and Chinese investors stepped up purchases. The metal soared by a record 19 percent last week on the Shanghai Futures Exchange and the bourse said late Friday that it will adjust transaction fees for commodity contracts including copper, zinc and steel from Nov. 15.Iron ore climbed to a two-year high on the Dalian Commodity Exchange as data showed rising steel output in China, the world’s largest steelmaker. Goldman Sachs Group Inc. said the initial reaction of iron ore and copper prices to the infrastructure spending proposed by Trump has been excessive and analysts reiterated their view for sequentially lower prices.

Gold fell to a five-month low, after last week sliding by the most in three years. [Bloomberg]

FTSE 100 Outlook and Prediction

With this bounce from Fridays lows gaining some traction I am thinking that we will see a rise towards the 6838 level. This level is fairly key for the bulls to break as it is resistance on the 2 hour chart from both the 100 Hull Moving average and also the coral has turned red at this level. So this area is worth a short and might stop this bounce in the short term. If the bulls were to break this level then the next area of resistance is the Bianca channels around the 6900 level, then 7000 above that. Lots of round numbers!

Support wise, initially we have the daily pivot at 6767, and then 6737 below that, with 6700 bringing up the rear. With the cable rate dropping back from $1.27 to $1.25 that has helped the FTSE to rise. Markets seem to have realised that maybe it wont be as bad as feared and with the likely rush of fiscal stimulus that Trump is going to unleash to kick start all sorts of infrastructure projects. We shall see anyway, but having said that the bond markets aren’t very happy!

Morning all,

It was looking like a push through 6800 ftse and 10800 dax was on the cards, but some decent pullbacks going on at the moment. Dax has double topped and moved down, but needs to break 10750 / 26 to prove definitively negative.

I’m staying out for the moment!

GL all

actually can add 10715 to those levels

Bit unsettled isn’t it. I had 6814 for a bit of a pull back but then another push higher. Doesn’t seem to want too though. 6838 still possible though

If I wanted to take a punt, I’d go long from here (6808, 10770), but not willing to put money into it – trying to learn to stay out when my edge is weak.

glad I didn’t do that! 🙂

Looks messy – hard to read

The 6814 was stronger resistance thank i thought it was going to be. Did expect to see it push to 6830 today then drop off

Was all very messy today on the indices – though seem to be some fairly clear channels on cable and eurusd.

Indices seem to be in an intraday downtrend, but uptrend on higher timeframes.

I escaped with a profit – more through luck than judgement 🙂

See you tomorrow (where is everyone today?? 🙂