FTSE 100 Support 6826 6817 6808 6799 6791

FTSE 100 Resistance 6857 6860 6866 6940 6978 7000 7060

Good morning. Well that was an interesting session yesterday – the bulls took it up to the 6850 resistance area and then we dropped back down but not really that far, before another push higher. The momentum has swung to the bulls again and buying the dips Friday through Tuesday has been the right play. The FTSE 100 is being a little odd though in terms of the levels that it is reacting from. Slight overshoot of the resistance (stop hunt maybe) and not quite reaching yesterdays support level at 6790, instead bouncing at 6810. Todays big event is of course the Chancellors Autumn Statement, at 12:30pm. This will be Chancellor Philip Hammond’s first Autumn Statement, and his first opportunity to outline his priorities for taxes and spending in the wake of the Brexit vote.

US & Asia Overnight from Bloomberg

Asian stocks rose amid optimism the global economy is strong enough to withstand higher U.S. interest rates. Oil slipped after OPEC deferred a decision on production cuts, while Malaysia’s ringgit weakened for an 11th straight day.

Australian and Chinese shares paced regional gains after U.S. equity indexes advanced to all-time highs. Government bond yields in Australia and New Zealand climbed as market-implied odds of a Federal Reserve rate hike in December held at 100 percent, while the ringgit slumped toward a 13-month low before a Malaysian central bank meeting. Oil slid for the first time in four days after OPEC left unresolved how Iran and Iraq will participate in planned output cuts.

The MSCI All-Country World Index headed for its third day of gains, the longest winning streak in two months, as equity traders took an optimistic stance before America’s Thanksgiving holiday on Thursday. Developed-market shares and the dollar have been among the biggest winners since Donald Trump’s surprise election victory fueled speculation of more fiscal stimulus, while government bonds and emerging markets have slumped. Traders will look for further confirmation of the Fed’s policy intentions when minutes from the central bank’s November meeting are released on Wednesday.

“Bulls have got control here and U.S. equity and many other developed markets are going higher, at least in the short term,” Chris Weston, chief markets analyst in Melbourne at IG Ltd., said in an e-mail. “The Fed has been guiding market participants to believe they always wanted a hike in December. They just needed a little more information before increasing rates and now they have more than enough information to convince them.”

Along with the Fed minutes, U.S. data on durable goods orders, jobless claims, home prices and manufacturing are due Wednesday. Malaysia is projected to keep interest rates on hold, while Singapore will release inflation figures for October.

Stocks

The MSCI Asia Pacific excluding Japan Index advanced 0.6 percent at 12:26 p.m. Hong Kong time, building on last session’s 1.1 percent increase. Raw-material and financial shares led gains.

Australia’s S&P/ASX 200 Index added 1.2 percent and the Hang Seng China Enterprises Index climbed 0.9 percent. Singapore’s benchmark gauge gained 0.5 percent, while the Philippines market lagged behind with a 1.2 percent drop. Futures on the S&P 500 Index were little changed, following last session’s 0.2 percent advance in the underlying benchmark.

“I’m not looking for anything spectacular in trading today,” Michael McCarthy, chief markets strategist in Sydney at CMC Markets, said by phone. “I expect we would be mildly positive to flat across the region.”

Bonds

New Zealand 10-year notes led a retreat in Asian bonds, with yields increasing seven basis points, or 0.07 percentage point, to 3.13 percent. Rates on similar-maturity Australian notes rose five basis points to 2.72 percent.

With Japan closed for Labor Thanksgiving Day, trading in Treasuries was delayed until the European open. Ten-year U.S. yields were little changed on Tuesday at 2.31 percent after jumping about 26 basis points since Trump’s election victory.

Currencies

The Bloomberg Dollar Spot Index, which tracks the greenback against 10 major peers, was little changed after climbing 4 percent since the election.

“A December Fed funds 25 basis-point rate hike is fully priced in,” said Elias Haddad, a senior currency strategist at Commonwealth Bank of Australia in Sydney. “The dollar will continue to be driven by the pace of the Fed’s tightening cycle beyond December.”

Malaysia’s ringgit fell 0.5 percent against the dollar, heading for the longest losing streak since December 2013. All 19 economists surveyed by Bloomberg predict Bank Negara Malaysia will hold its overnight policy rate at 3 percent on Wednesday, after surprising the market with a reduction in July. The central bank has shifted focus to supporting the ringgit as expectations of a Fed rate increase spur capital outflows.

China’s yuan weakened to a record in offshore trading, sliding 0.1 percent to 6.9222 per dollar.

Commodities

Brent crude declined 0.2 percent to $49.01 a barrel as West Texas Intermediate dropped 0.3 percent to $47.90.

While Libya’s OPEC governor Mohamed Oun said talks Tuesday in Vienna ended with a consensus, the meeting didn’t resolve whether Iraq and Iran will join any output cuts proposed by major global oil producers and deferred the matter to a meeting scheduled for Nov. 30, two delegates said. U.S. crude stockpiles fell by 1.28 million barrels last week, the industry-funded American Petroleum Institute was said to have reported Tuesday, ahead of government data.Copper for three-month delivery rose 0.1 percent to $5,620 a metric ton on the London Metal Exchange, while most other industrial metals were little changed. [Bloomberg]

FTSE 100 Outlook and Prediction

I am still of the mind that we are going to slowly grind higher and am expecting us to see 7000 again at some point soon. The FTSE is making hard work of rising though but I feel that going long at supports and riding it out will work out fine over the next few weeks. Gold has remained relatively depressed since that flourish to 1330, hovering around the 1212 area, so I would be expecting a bit more risk on for equities and for the price to rise.

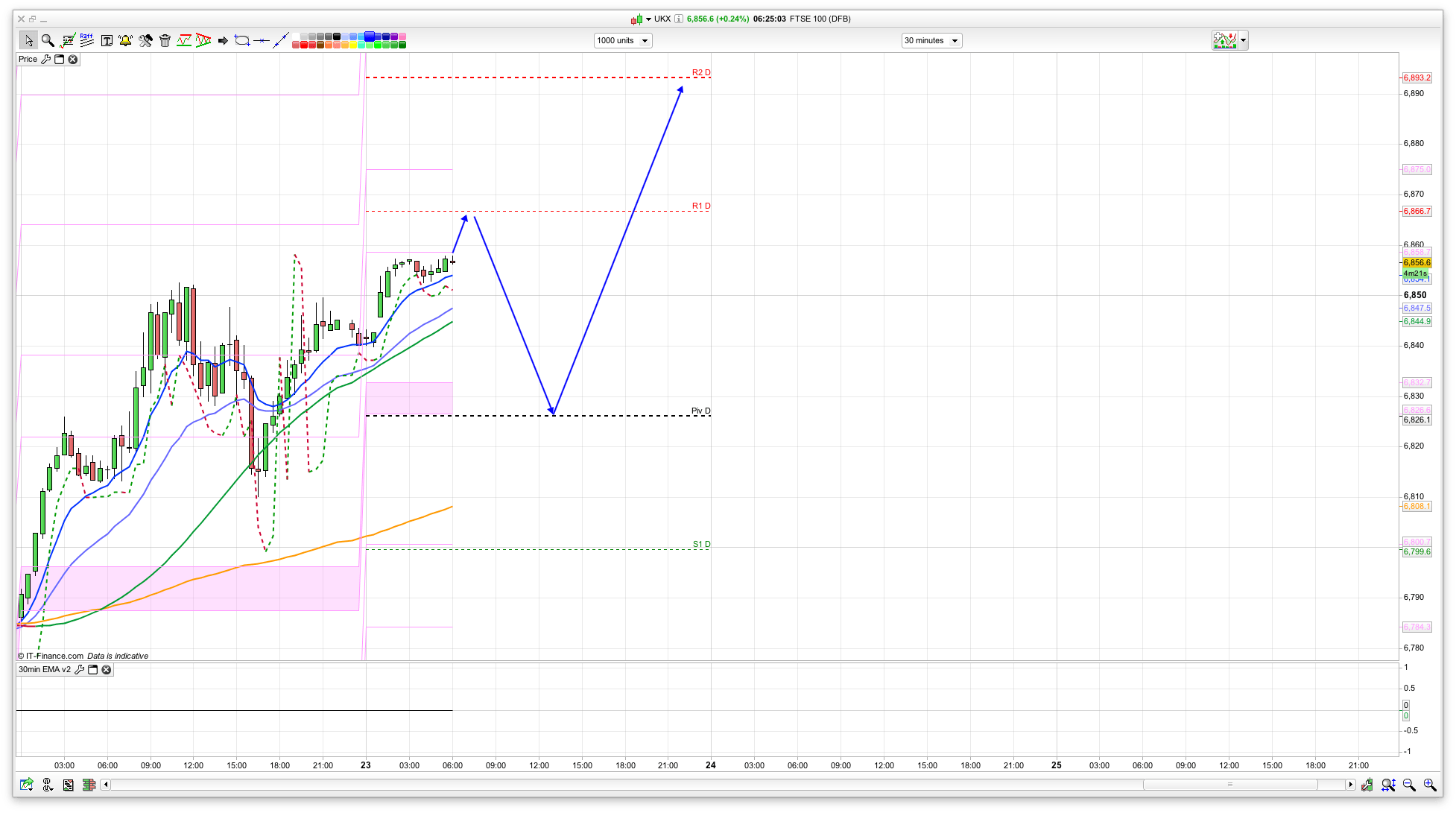

For today, we have initial resistance at R1 at 6866, just above the 2 Bianca channels which are around 6860 so we may see an initial bit of profit taking here from the longs that have been holding since 6750 on Monday. Of course, we have the Autumn Statement at 12:30 so that will have an effect on things. We also have a 7 point dividend tonight, so bear that in mind. We may well get the divi chasers appear around 4pm or slightly before.

Support is at the pivot at 6826 initially, with 6799 below that where we have S1. The pivot may well hold for a long entry, but if the usual scenario plays out it will overshoot before climbing back. 6799 would be a good spot to long from if seen also, with a stop around 6785. The bulls are just breaking above the 25ema on the daily at the moment (6849) so if they can hold above that area with a decent close today then we could see some impetus for further upside towards 7000.

I think Ftse will pull back to 6840 area before pushing up later in session.

Dax looking poorly

hey all.

just listening to the autumn statement. Need a surprise of some such to make it exciting 🙂

FTSE looks like a head and shoulders patttern on the daily chart…

Crikee. Gold looking good value?…