FTSE 100 Support 6819 6815 6781 6736

FTSE 100 Resistance 6854 6859 6861 6889 6936

Good morning. Was a little bit early with the first short yesterday at 6865, however the 6885 short worked much better, as did the S&P and Gold shorts. The ECB left things largely unchanged and also started to question the benefits of QE. Its a bit like a drug addict once you start really – you need more and more to have the same effect and its only ever going to end one way. Large parts of the eurozone are slipping deeper into a deflationary trap despite negative interest rates and one trillion euros of quantitative easing by the ECB, leaving the currency bloc with no safety buffer when the next global recession hits. The ECB is close to exhausting its ammunition and appears increasingly powerless to do more under the legal constraints of its mandate. It has downgraded its growth forecast for the next two years, citing the uncertainties of Brexit, and admitted that it has little chance of meeting its 2pc inflation target this decade, insisting that it is now up to governments to break out of the vicious circle.

Mr Draghi dashed hopes for an expansion of the ECB’s monthly €80bn (£60bn) programme of bond purchases, and offered no guidance on whether the scheme would be extended after it expires in March 2017. There was not a discussion on the subject.

North Korea tested their 5th nuclear weapon overnight, sending jitters through South Korea.

US & Asia Overnight from Bloomberg

Asian stocks fell the most in a month and regional bonds joined a global debt selloff after signs central banks in Europe and Japan are starting to question the benefits of further monetary easing. South Korean equities slid with the won after a nuclear weapons test in North Korea.

Technology companies were the biggest drag on the MSCI Asia Pacific Index after Apple Inc. dropped by the most since June. Korean stocks were the region’s worst performers, while Hong Kong shares rallied after China opened up a new channel for its insurers to invest in the securities. The euro rose to a two-week high after the European Central Bank downplayed the need for more stimulus, rhetoric that torpedoed sovereign debt globally. Crude surged more than 6 percent this week following an unexpected plunge in U.S. stockpiles.

Swings in financial markets are largely being dictated by monetary policy outlooks in the world’s largest economies and global equities are on track for a weekly gain after prospects for a September interest-rate hike in the U.S. receded. ECB chief Mario Draghi played down the prospect of an increase in asset purchases on Thursday, a day after his counterpart at the Bank of England signaled he’s in no rush to boost stimulus. The head of the Bank of Japan said a comprehensive review of its policy will take into account the costs as well as the benefits of its actions.

Central bankers in Europe and Japan “probably realize they cannot solve this problem with monetary policy,” said Kim Youngsung, the head of overseas investment in Seoul at South Korea’s Government Employees Pension Service, which has $13.6 billion in assets. “They probably need fiscal policy, not just monetary policy.”

More light may be shed on the outlook for U.S. interest rates when regional Fed chiefs for Boston and Dallas speak Friday, while euro-area finance ministers and central bank governors will be meeting in Bratislava. France and Spain are due to report industrial output figures for July, while Turkey has second-quarter gross domestic product data coming.

Stocks

The MSCI Asia Pacific Index was down 0.6 percent as of 1:13 p.m. Tokyo time, trimming this week’s advance to 2.2 percent. Samsung Electronics Co. and Taiwan Semiconductor Manufacturing Co. were the biggest contributors to the benchmark’s decline.

“While the ECB disappointed, we could still expect additional stimulus later in the year as there’s so much uncertainty in Europe,” said James Woods, a strategist at Rivkin Securities in Sydney. “Investors will probably sit on the sidelines ahead of the Fed and Bank of Japan policy meetings.”

The Kospi index slid 1.5 percent after North Korea conducted its fifth nuclear arms test. South Korean President Park Geun Hye said the move was an act of “maniacal recklessness” and said pressure will be increased on the North to give up its nuclear weapons.

Hong Kong’s Hang Seng Index rose to a one-year high and a gauge of Chinese shares listed in the city rallied for a seventh day. Chinese insurers can buy the city’s shares through an exchange trading link with Shanghai, the industry regulator announced late Thursday, without saying when it would take effect. Hong Kong Exchanges & Clearing Ltd. jumped as much as 7.4 percent, its biggest intra-day gain this year.

Shanghai shares were little changed after data showed China’s factory-gate deflation eased for an eighth straight month and consumer prices rose the least in almost a year.

Futures on the S&P 500 Index were also steady after the U.S. benchmark slipped 0.2 percent in the last session, led by a 2.6 percent decline in Apple.

Currencies

The Bloomberg Dollar Spot Index fell 0.2 percent. It dropped 0.9 percent this week after data pointing to slowdowns in hiring and business activity cooled expectations for a U.S. interest-rate increase this month. The chance of a hike dropped four percentage points this week to 28 percent, futures prices show, and the greenback lost ground versus all 10 major peers.

“In order for the dollar to bounce back, rate-hike expectations have to heighten,” said Yasuhiro Kaizaki, vice president for global markets at Sumitomo Mitsui Trust Bank in New York. “The market will need fresh factors and that may not come until retail sales next week.”

The won fell 0.7 percent versus the greenback, paring this week’s advance to 1.6 percent. The Bank of Korea kept its benchmark interest rate at a record-low 1.25 percent on Friday and said it’s prepared to intervene to curb volatility in the currency market if herd behavior is evident.

The euro gained 0.2 percent, headed for a weekly gain of about 1 percent. The ECB refrained from adding to its unprecedented stimulus at a policy review on Thursday and Draghi said an extension of its quantitative-easing program wasn’t even discussed. About half of respondents to a Bloomberg survey conducted last week foresaw easing, with almost all the others predicting changes in October or December.The yuan was down 0.15 percent in Shanghai, set for a third weekly loss. China will allow a gradual depreciation of its currency and policy makers should keep opening up the nation’s capital account despite fund outflows, said Fan Gang, head of the National Institute of Economic Research and an adviser to the nation’s central bank.

Bonds

The yield on 10-year U.S. Treasuries was little changed at 1.59 percent after climbing six basis points on Thursday. Rates on similar-maturity bonds in Australia and New Zealand rose by at least seven basis points to 1.96 percent and 2.34 percent, respectively.

SoftBank Group Corp. raised 471 billion yen ($4.6 billion) in its biggest yen bond sale on record. The offering comes after the Japanese wireless carrier completed this week its acquisition of British semiconductor designer ARM Holdings Plc for about $32 billion.

Commodities

Crude oil declined 0.8 percent to $47.23 a barrel in New York, paring this week’s jump to 6.3 percent. U.S. inventories fell last week by the most since January 1999, official data show. The priced climbed since early August amid speculation members of the Organization of Petroleum Exporting Countries and Russia would agree on measures to stabilize the market at talks in Algiers this month.

“The possibility of OPEC and Russia agreeing on an output freeze is low, but there’s a chance they may come to a partial agreement that puts a ceiling on output to accommodate countries that are trying to recover production,” said Hong Sung Ki, a commodities analyst at Samsung Futures Inc. in Seoul. [Bloomberg]

FTSE 100 Outlook and Prediction

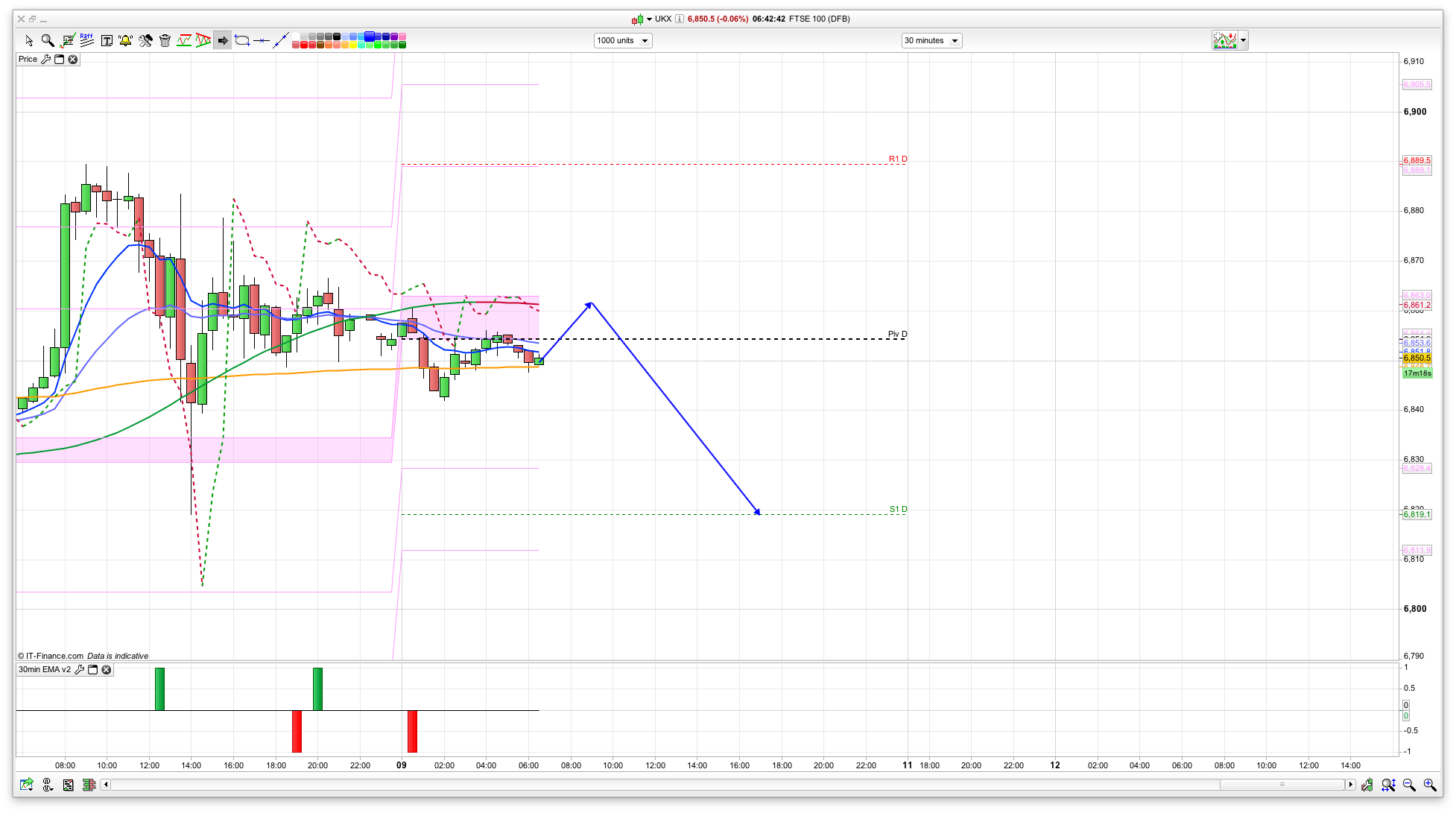

The FTSE 100 bounced back from its lows yesterday and is currently at 6850. However, I have a few resistance levels at 6860 so feel that a short here is worth a go for a drop down to S1 at 6820 – which is also the low area from yesterday. The 2 hour chart is bearish now, with resistance at 6859, and we have a red coral on the 30min at 6861. The SP and Dax have stayed lower since the dip yesterday so I am thinking that the FTSE still has some more downside potential. If the bulls were to break above 6861 though, then that changes things, and we could be back on for a rise towards 6950. Certainly tricky to call at the moment, but that 6860 area looks worth a short to start with.

We are at the mid point of the Bianca channels, with 6889 as first resistance and 6781 as the first support. The daily pivot is 6854 for another bit of resistance to start with.

Anybody In?

I am in with my 66 short lol..how about you

wil b looking to cm out around 93 though

Hello, I pulled some of my SPs but one left in incase it dumps.

I still have a few in FTSE, looking to stage out, 820, 800, 790 and then 750.

That’s my plan at least!

Closed all SP shorts for 16pts

Pulled a few of my FTSE shorts at 800 for 50 to 60 odd points. Still got some in but looking for 780, 750 now? May retrace up in which case I will reshort at 850

I feel like I don’t want to jinx it, but I’m short from 6870.5 – seeing some blue at last…

I’m shorting the @arse off of this.

How’s it looking, what you in at and what level do you need to recover losses from before.

Ya, Its like it wants to dump but just isn’t quite sure.

May turn my phone off and set limits for 750 and hope for the best.

2 positions closed @88 for 50pts

I am going to add a buy after FTSE close as I think it will retrace up.

Only if it’s at or below 785ish

If DOW breaks 300 then I think we will see a big shift down next week

Long on Dow at 275 with 20pt stop. Retrace punt.

What a wonderful day ! Done for the week .. see ya later guys 🙂

Long at 55. Punt

Just gone short on DOw after I lost 100pts attempting to guess the bottom. Watch it rocket now.

Morko, just done the same with the FTSE £1500 in 15 minutes…..

Good skills! I set a tight stop and got whiplashed out.

Still I have had a great week and feel I earnt a punt.

Anyone else feeling a deadcat bounce coming for Monday?

There’s a strong chance, my plan is to go long tonight, will add in if it drops tomorrow or next week by any significant.

I see this as middle to upper middle band. Will use the grid method I have previously tried to explain if this middle ground holds.

I’m still feeling Bearish, I think this could be the start of the correction?.

Possibly so, I’m going short with a big stop at on tomorrow’s resistance. 6500 is going to surface before month end… IMO

Morning all ! Long @ 83 this morning looking for 740-50

Long at 90, and 66

This may just keep falling. Well pleased I pulled my long last night – not!!!