FTSE 100 Outlook and Analysis for 30th October 2019

Markets were forced to fly blind into last night’s crunch Commons vote on a general election. High expectations that a bill calling for a December ballot would pass were dampened slightly by a report just ahead of the bell that the Labour party could be pushing for the participation over over-16s and EU citizens. It was later confirmed that there will not be a vote on lowering the voting age to 16 or on extending the vote to EU citizens.

While the pound’s movements were muted through the London session, stocks toyed with losses, with the FTSE 100 spending most of the day in the red as UK-exposed stocks sagged and BP put a major drag on the index. The oil giant closed down 19.5p at 492.6p, after announcing its profits had plunged during the third quarter.It was the second day in a row where the mood on the blue-chip index was dominated by a single heavyweight, following HSBC’s poor results on Monday. The lender dropped for a second session, closing down 6.4p at 588p. The blue chip index ended down 0.3pc at 7306.26.

On the FTSE 250, which pulled back deeper losses to close down 0.21pc at 20,168.33, there were few standout performances.

Markets Mixed

Stocks in Asia were poised for a mixed start Wednesday after a lackluster session for U.S. equities as markets await the Federal Reserve’s policy decision. The central bank is widely expected to lower rates again Wednesday, and the key for markets will be the tone of Chairman Jerome Powell’s press conference later in the day. Treasuries and the dollar were flat, while equity futures dipped in Japan and nudged higher in Hong Kong. A report that China and the U.S. might not sign a partial deal next month dented U.S. stocks exposed to the battle. Elsewhere, the pound was flat, gold held at $1,487.71 an ounce and crude decreased 0.6%.

Trump

In its most direct intervention yet to manage trade and production, the Trump administration wants to dictate how and where global auto companies make cars and parts, according to people familiar with the effort. The issue is being discussed between Trump administration officials, congressional staff, and domestic and foreign auto makers. The White House wants specific language that would allow it to unilaterally administer the production rules for companies, but the companies, lawmakers and even the U.S. International Trade Commission have cautioned that the rules are so strict that they would result in higher car prices and lost sales. The push illustrates how much Trump’s administration has drifted from Republicans’ free-market ways.

FTSE 100 Outlook | Trading Signals | Forecast | Prediction | Analysis

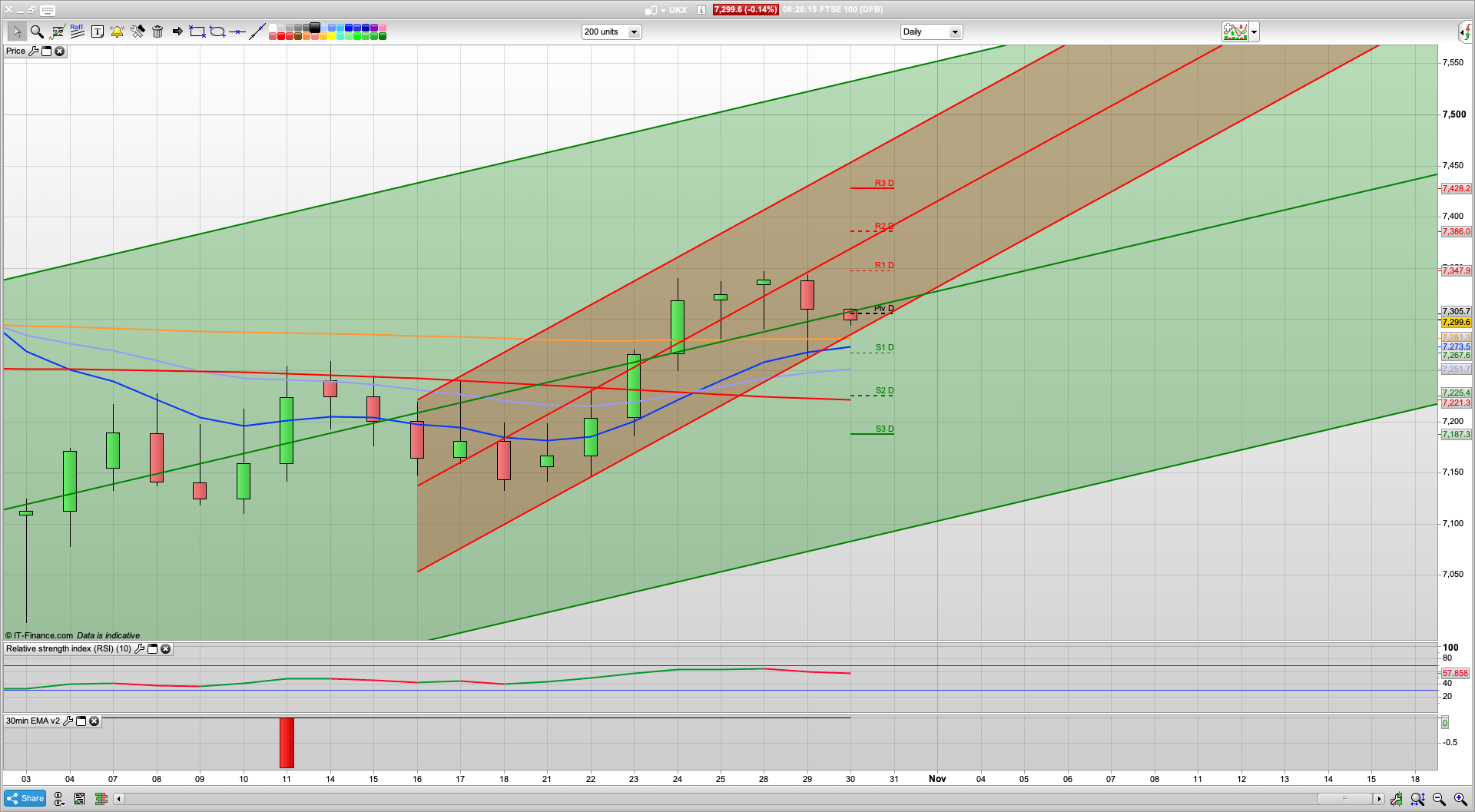

We bounced just above the daily support level of 7250 yesterday, at a session low of 7263, and the bulls showed some buying appetite there to get the price back above the 7300 level, where we have hovered around all night. Everything today is going to be focussed on the Fed later (at 6pm this evening) and whether rates will be cut again. The forecast is for them to do so.As such, we may well see buy the rumour, sell the news once the US session gets underway. Though with the S&P climbing to 3047 yesterday and already dropping back a bit we may have seen an early assault from the bulls!

For the FTSE today, the main levels are along similar lines to yesterday – daily support at 7250 still looks good, while daily resistance at 7350 also looks viable. Above this the 10 day Raff channel top has climbed further to the 7450 level now, though we may well see a stutter at 7395 if we were to get that high. Buying the dip yesterday didn’t really work as the 7320 level didn’t hold, nor the recent low of 7290 as political uncertainty ruled the day. Labour decided to about turn and support the election after all. Was a bit annoying that it didnt drop down to the 7250 level yesterday before that bounce, but it keeps it in play for today.

The daily chart is still bullish, which is what is showing the 7250 support level, along with a key fib at this level. Should the bears break below 7250 then a test of 7200 (and S3 at 7191) is likely. If the Fed keep rates as they are then we may well see the bears take control and move it lower, especially as the US markets are making record highs, and that only goes on for so long before the inevitable wave of profit taking. Talking of which, the S&P 2 hour chart has gone bearish with that drop down from 3047 and has resistance at 3041.

Recommended Broker

IC Markets – offers market leading pricing and trading conditions by providing clients with True ECN Connectivity; this allows you to trade on institutional grade liquidity from the world’s leading investment banks, hedge funds and dark pool liquidity execution venues. Highly recommended!

Membership and Live Trading

If you would like more detailed analysis for FTSE 100, DAX, Gold and S&P, including the trades that I am looking to take myself, then please join my active members community.

What you get

- Daily Analysis pre market open (sent around 7am each day) for FTSE, DAX, Gold and S&P.

- Daily email pre market includes my trading plan for the day including ORDER levels, with stops and targets/limits

- Telegram live trading room and webinar group membership for discussion and realtime trade updates

Keep up to date with new content, free sign up below

[yikes-mailchimp form=”4″]