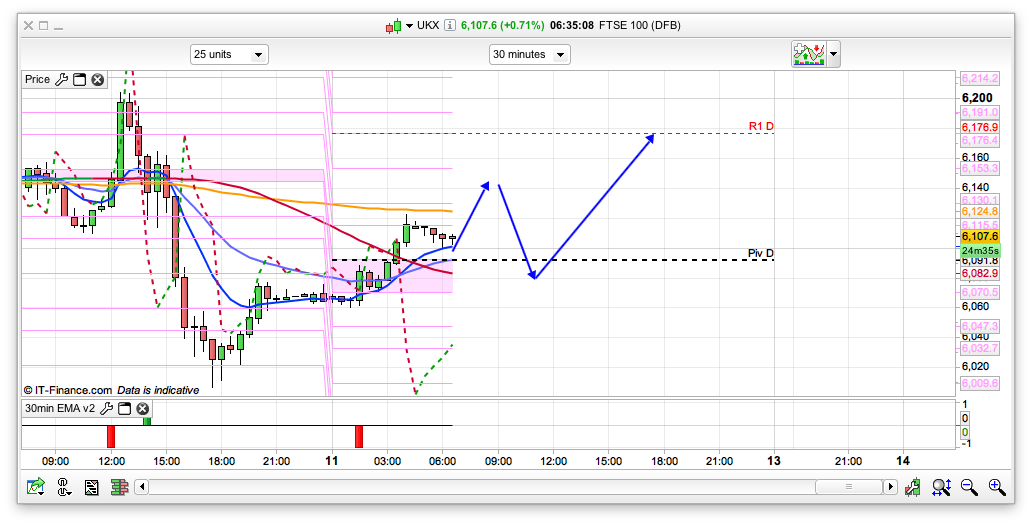

Support 6092 6081 6057 6038 6013 5980

Resistance 6124 6134 6146 6176 6215

Good morning

Market Summary for Thursday 10th March 2016

In the morning the FT100 had dipped a bit then started to gradually rally into the ECB presentation at lunchtime.

There was a spike up above 6200 when the ECB announced a cut to its deposit rate deeper into negative territory and increased monthly asset buys to 80 billion euros from 60 billion euros, exceeding expectations for an increase to 70 billion.

Then European shares fell after the European Central Bank President Mario Draghi said more rate cuts were unlikely which pushed the FT100 down to 6036 at the close.

This gave an intraday swing of about 170 points or almost 3%.

The moves also mirrored a reciprocal of the Euro, which also had one of its biggest intraday volatility levels for a long time.

Banks and commodities were the biggest fallers with gold and insurance shares the biggest gainers.

Got the analysis spot on yesterday but just missed the short order at 6205 by 1 point before dropping 200 points so wasn’t ideal for the automated trades. Earlier in the day the 6116 10 day Bianca support level held well. A day of fairly wild swings with the ECB big guns being wheeled out but not convincing the market.

US & Asia Overnight from Bloomberg

- China’s raises yuan onshore reference rate by most in 4 months

- Asia-Pacific index erases loss, heads for 4th weekly advance

Asian stocks climbed for a second day, with the regional benchmark index heading for a fourth weekly gain, as investors reassessed fresh stimulus measures unleashed by the European Central Bank.

The MSCI Asia Pacific Index advanced 0.8 percent to 126.59 as of 12:56 p.m. in Hong Kong, erasing earlier losses of 0.6 percent and heading for a 0.2 percent increase this week. Mounting concern that central banks have lost the ability to jolt financial markets out of turmoil has threatened to derail a rally in global equities, with the MSCI All-Country World Index on track for its first weekly decline in a month. ECB President Mario Draghi’s indication that he doesn’t expect more rate cuts sparked stock declines in Europe and in early Asian trading. Asian investors reassessed the ECB move in the afternoon as focus now shifts to next week’s meetings of the Bank of Japan and the Federal Reserve.

“The market is trying to go back and re-digest that yesterday was an over-reaction and that that one statement was the wrong focus,” said Kay Van-Petersen, a strategist at Saxo Capital Markets in Singapore. “It was taken out of context. It said we don’t anticipate that it’ll be necessary to reduce rates further, but nothing could be further from the truth. It’s QE-for-life for the next four to five years in the euro zone.”

Regional Gauges

Japan’s Topix index added 0.8 percent, erasing morning losses of as much as 1.5 percent. South Korea’s Kospi index added 0.3 percent. Australia’s S&P/ASX 200 Index, Singapore’s Straits Times Index and Taiwan’s Taiex index each increased 0.4 percent. New Zealand’s S&P/NZX 50 Index gained 0.1 percent. Hong Kong’s Hang Seng Index jumped 0.8 percent.

The Shanghai Composite Index was little changed. China’s central bank raised its onshore daily reference rate for the yuan by the most in four months on Friday. The National People’s Congress continues, with reports on industrial production, retail sales and fixed assets scheduled for Saturday.

Futures on the Standard & Poor’s 500 Index added 0.7 percent. The underlying U.S. equity benchmark index closed little changed on Thursday after swinging between gains and losses amid tempered optimism on the ECB’s latest package of monetary stimulus.

The ECB cut all its interest rates and expanded the scope of its bond-buying program as Draghi strives to fend off the threat of euro-area deflation. The moves exceeded market expectations and initially spurred demand for risky assets.

Investors took less than 90 minutes to go from overwhelmed at the scale of his move to underwhelmed at the stimulus outlook, with the Stoxx Europe 600 Index retreating to close 1.7 percent lower. Draghi said at a press briefing that risks to the euro-area growth outlook are still to the downside, and the rate of inflation will remain negative before picking up later in the year. Still, he said he doesn’t anticipate more rate cuts. [Bloomberg]

FTSE 100 Outlook and Prediction

Well we have had the dip down to 6000 as expected and bounced pretty well from there, so the bulls were keen to defend that. Watching it all unfold yesterday I had a pretty wild thought and that is a rise from that low at 6010 to 6350 before a bigger move down to sub 5500 (the most recent low). I’m in the camp that all those stimulus measures announced yesterday are actually a bad thing as it shows how screwed everything still is, coupled with the fact that the ECB now has nothing left to fight deflation. If they get it wrong its going to be messy. For today we have initial support at the pivot at 6092, and have held the rises from the 6010 low yesterday so I am expecting a rise towards the 6145 area to start with before a dip back. Its a Friday so liable to be weird, especially as the ECB news is further digested. If the bulls stay in control today then any dip back towards 6080 is likely to be bought up for a push back. Being a Friday I will reduce my stake size a bit as it can be odd. If that 6080 holds then we could get a push up later and bullish going into the weekend. We have the bottom of the 2 Bianca channels at 6057 and 6038, as well as both Raffs at 6006 so some decent daily supports still above the 6000 level. I don’t think “they” will want it to tank so soon after announcing all those measures as it makes them look a bit pointless!