Support 6143 6138 6128 6067 6045

Resistance 6170 6177 6200 6209 6242

Good morning.

Market Summary for Monday 14th March 2015

A largely non eventful day on the markets apart from Brent crude dropping nearly 3 percent after Iran dashed hopes of a coordinated production freeze.

The FT100 oscillated in a small range between 6160 and 6180 as traders took to the sidelines after last week’s move up and the FED this week.

So stalemate for most traders.

On the upside were some commodity shares and housebuilders and to the downside oils, insurance and gold. The gold short worked well yesterday, as did the S&P long. FTSE and Dax orders weren’t triggered.

US & Asia Overnight from Bloomberg

- Yuan weakens as PBOC cuts fixing by most in two months

- Aussie, ringgit decline as commodities prices retreat

Asian stocks retreated from a 10-week high and the yen strengthened the most in a week as the Bank of Japan held off from adding to record monetary stimulus at a review on Tuesday.

The MSCI Asia Pacific Index declined for the first time in four days as all 10 industry groups lost ground. The yen strengthened against all 31 major peers as the BOJ maintained a negative policy rate and kept asset-purchase plans unchanged. The yuan depreciated as China’s central bank cut its daily fixing by the most in two months. Malaysia’s ringgit and Australia’s dollar led losses among the currencies of resource-exporting nations as oil dropped below $37 a barrel. Gold fell to its lowest level in almost two weeks.

While world equities have staged a comeback since reaching a 2 1/2-year low in mid-February, so far there are few signs that monetary easing in China, Europe and Japan is pulling the global economy out of a slump. The Bank of Japan’s decision to maintain policy was forecast by most economists and the authority said it’s prepared to ease further if needed to revive inflation expectations.

“As a whole, this is not a negative and not something that will derail the market’s recent trend in the risk-on direction,” said Yusuke Kuwayama, a portfolio manager at Tokio Marine & Nichido Fire Insurance Co. in Tokyo. “The focus now is on tomorrow’s FOMC.”

The European Central Bank announced unprecedented stimulus last week, while the Federal Reserve will conclude a review on Wednesday and the Bank of England a day later. Investors will be seeking guidance from the Fed on the trajectory of U.S. interest rates as expectations build for policy makers to add to December’s increase.

Stocks

The MSCI Asia-Pacific gauge fell 0.8 percent as of 2:52 p.m. Tokyo time, led by declines in raw-materials producers. Benchmarks declined across the region with Japan’s Topix index losing 0.5 percent and Australia’s S&P/ASX 200 Index sliding 1.4 percent. The Shanghai Composite Index declined 1.2 percent.

Standard & Poor’s 500 Index futures retreated 0.2 percent, while contracts on the U.K.’s FTSE 100 Index dropped 0.4 percent.

Currencies

The yen strengthened 0.3 percent to 113.47 versus the dollar. While only five of 40 economists surveyed expect further easing at Tuesday’s BOJ meeting, 88 percent forecast more stimulus by the end of July.

“The BOJ conceded that inflation expectations have weakened, pointing to a high near-term risk of more policy easing,” said Joseph Capurso, a currency strategist at Commonwealth Bank of Australia in Sydney. “The yen will test 110 per dollar before the middle of the year.”

The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, was little changed Tuesday after rising 0.4 percent last session. While traders are pricing in little chance of a Fed rate increase on Wednesday, they have boosted bets on a move happening later in the year. Fed funds futures show the probability of a June increase is now about 50 percent, having risen from less than 10 percent a month ago as U.S. economic data improved and equities rebounded.

The ringgit declined 0.3 percent versus the dollar as the dip in oil prices dimmed prospects for Malaysia, Asia’s only major net exporter of crude. The currencies of Australia, Canada and South Africa all lost 0.3 percent or more as the Bloomberg Commodity Index fell for a second day.

The yuan fell 0.12 percent after the People’s Bank of China lowered its reference rate for the currency by 0.26 percent. That’s the biggest cut since the first week of January, when a series of weaker fixings heightened concern about the state of China’s economy and spurred a global stocks rout. China’s central bank has drafted rules for a so-called Tobin tax on foreign-exchange transactions that would help curb exchange-rate speculation, people with knowledge of the matter said Tuesday.

Commodities

The Bloomberg Commodity Index was headed for its lowest close in a week. West Texas Intermediate crude fell 0.7 percent to $36.91 a barrel, extending Monday’s 3.4 percent slide. U.S. stockpiles probably expanded last week, keeping supplies at the most since 1930, analysts predicted ahead of data due on Wednesday.

Gold for immediate delivery dropped 0.5 percent to $1,229.43 an ounce, after sliding more than 1 percent on each of the last two trading days. The precious metal, regarded as a hedge against inflation and a haven asset, is still up 16 percent this year. Copper declined 0.4 percent in London, falling for a second day.

Bonds

U.S. Treasuries due in a decade were little changed, yielding 1.96 percent. Pacific Investment Management Co. predicts the rate will climb as high as 2.5 percent this year as inflation accelerates and the Fed raises interest rates.

“We see one to two rate hikes this year for the Fed, whereas the market is only expecting only one,” Mark Kiesel, one of the three managers of Pimco’s $87.8 billion Total Return Fund, wrote in an e-mail. “If rates were to head towards 2.5 percent, we would be looking to add at that level.” [Bloomberg]

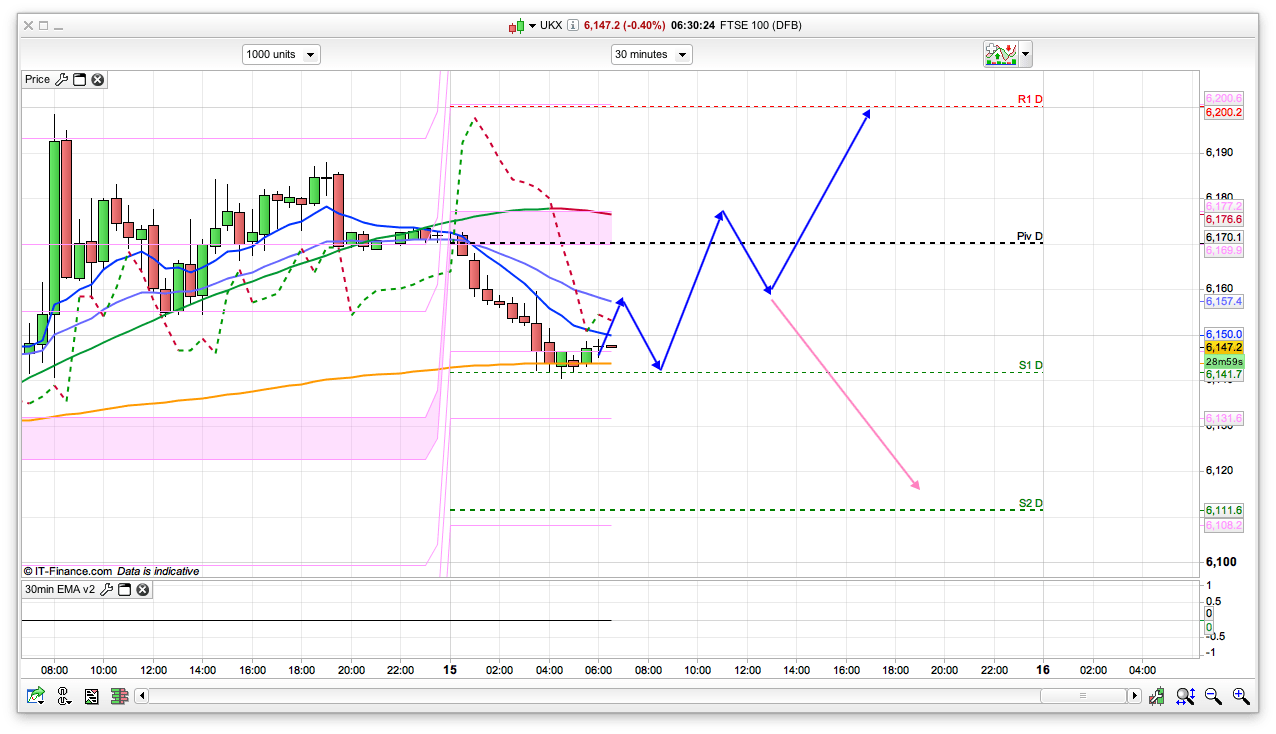

FTSE 100 Outlook and Prediction

Looks like another sideways day at the moment though the decline in gold from 1260 yesterday could help push the FTSE higher today. We are still in the 6100/6200 range for the moment and with the Fed later this week again we might continue this sideways chop for a bit longer. Interestingly my 2 hour chart has decent support at the 6130 area for a push higher, whilst the 30min chart has resistance at 6158 and 6177 to start with. The 200ema on the 30min has held as support initially at the 6140 area. There are a lot of support and resistance levels all clustered quite close together which isn’t ideal. I have put the plan B pink arrow on todays chart which I don’t do too often. Basically if we do hit resistance at 6177 and then drop off, the bears will either continue that drop on a break of 6160 or it will bounce there for a run at 6200 again. Hard to say at the moment so be prepared for both eventualities. Generally, with the 2 hour chart being bullish and support at 6130 I am favouring a bit of a rise today, however, the failure to really break 6200 yet still keeps the bears at the table. Also worth trying shorts at those 30min resistance levels but keep the stops tight. Stay nimble really and I still have my wild though for a rise to 6350 after that Thursday action last week!