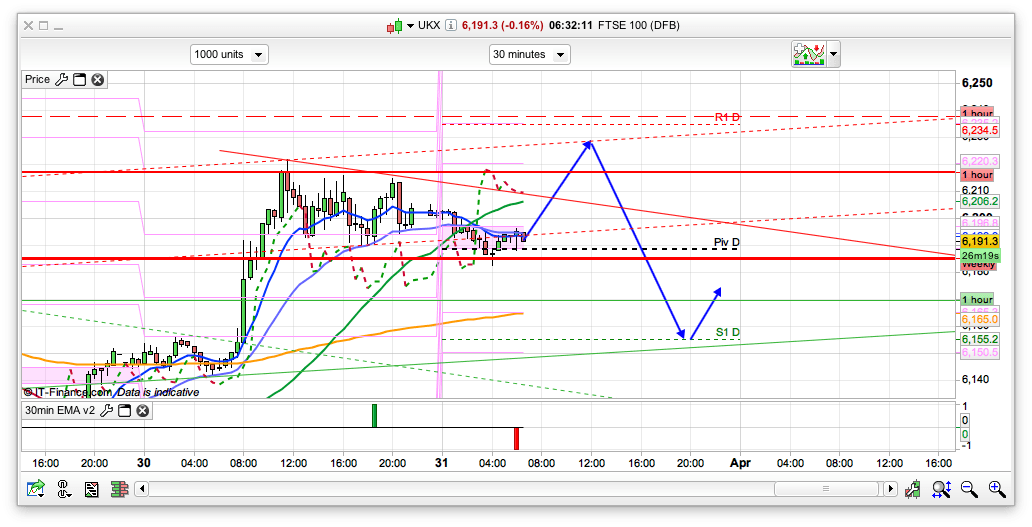

Support 6188 6165 6155 6088

Resistance 6229 6230 6234 6242

Good morning. Bit frustrating to have the FTSE and Gold trades stopped out to the pip yesterday (6222 and 1244) but from those levels they both fell back, with the FTSE hovering around the 6200 level. Generally, European shares advanced for a second day after Federal Reserve Chair Janet Yellen reiterated that interest rates will be raised gradually in light of uncertain global growth.

US & Asia Overnight from Bloomberg

- Dollar set for worst month since 2010 as rate-hike bets cut

- Chinese shares traded in Hong Kong are close to bull market

The prospect U.S. borrowing costs will stay put for longer sent Asian stocks toward their best month since October, with Chinese shares in Hong Kong near a bull market. South Korea’s won strengthened, while crude oil fell with copper.

Shares in Sydney rose the most in two weeks amid a global rally that has the MSCI All-Country World Index on the brink of erasing its losses for 2016. The won climbed 0.6 percent, Malaysia’s ringgit extended gains at a seven-month high and the Bloomberg Dollar Spot Index headed for its worst month in more than five years after Federal Reserve Chair Janet Yellen reiterated that slackening global growth called for a gradual approach to raising rates. U.S. crude dropped back below $38 a barrel as an increase in American supplies kept stockpiles at their highest level since 1930. Copper and zinc fell.

After stimulus efforts from Japan and Europe failed to arrest a global stock selloff at the start of 2016, the prospect of American rates staying where they are for at least the first half has salvaged the quarter for riskier assets. Chicago Fed President Charles Evans reinforced Yellen’s message on Wednesday, signaling the central bank would tolerate above-target inflation for a “brief period” amid threats to American expansion.

“A lot of the recent rebound has been down to the Fed back-tracking on rate hikes,” Mark Lister, head of private wealth research at Craigs Investment Partners in Wellington, which manages about $7.2 billion, said by phone. “We’ve seen a big rally but there are still some genuine worries out there. Markets had been overpricing some of the risks, whereas now they’re probably underpricing them.”

Futures now show no chance of the Fed altering monetary policy at its meeting next month and only 45 percent odds of a rate increase by November. Private American jobs data came in better than analysts expected last session, boding well for official payrolls figures due Friday.

Stocks

The MSCI Asia Pacific Index advanced a second day, rising 0.2 percent as of 12:47 p.m. Hong Kong time. The gauge is poised for an 8.3 percent jump in March. Consumer and phone-company shares drove Australia’s S&P/ASX 200 Index up 1.3 percent, while New Zealand’s S&P/NZX 50 Index rose 0.6 percent, climbing for a third day. The Topix index swung between gains and losses in Tokyo.

The Hang Seng China Enterprises Index added as much as 0.8 percent, extending its rebound from a Feb. 12 low to more than 20 percent, before paring the advance. Futures on the Standard & Poor’s 500 Index were down 0.1 percent following a 0.4 percent climb for the U.S. benchmark that put it back at levels last seen on Dec. 29.

Thailand reports on trade Thursday and Sri Lanka updates on consumer prices. China will provide figures on its current account balance, with Japanese housing starts also due.

Currencies

The ringgit extended its climb into a fourth day, rising 0.3 percent. Malaysia’s currency has jumped 9.4 percent this quarter, on track for its best such performance since 1973 amid oil’s rally from an almost 13-year low. Malaysia is the region’s only major net exporter of oil.

The South Korean won added 0.6 percent. Bloomberg’s dollar gauge, which tracks the greenback against 10 major peers, rose 0.1 percent following a three-day slide. The index has lost 3.7 percent this month, its steepest drop since September 2010.

“The dollar is overvalued, particularly against the major currencies, euro and yen,” said Steven Saywell, BNP Paribas SA’s global head of foreign-exchange strategy in London, in an interview on Bloomberg TV.

The yen, regarded as a haven investment along with gold and government debt, gained for a third day to 112.21 per dollar. After the ringgit, Japan’s currency is the best performer in Asia this quarter, with volatility at the start of the year burnishing its appeal.

The offshore yuan traded in Hong Kong was set for its strongest quarterly performance since 2011, rising 1.46 percent against the dollar as China’s leaders intensified efforts to boost sentiment. The Shanghai rate advanced 0.42 percent, the first gain in four quarters.

Commodities

West Texas Intermediate crude declined 1.3 percent to $37.83 a barrel, dropping for the fifth time in six days as the increase in U.S. stockpiles reinforced concern over a global glut in the commodity. Brent lost 1.1 percent to $38.84, on track for a second straight monthly advance and its first quarterly climb since the second three months of 2015.

Inventories expanded for a seventh week to 534.8 million barrels, according to a report from the Energy Information Administration Wednesday, while imports and production dropped. Ecuador and Venezuela will support a cut to output at a meeting between major exporters in Doha next month, Ecuador’s Oil Minister Carlos Pareja said in a post on the ministry’s Twitter account.

Gold for immediate delivery added 0.4 percent to $1,229.27 an ounce, after sliding 1.4 percent last session, while copper declined with zinc, losing at least 0.5 percent in London trading. [Bloomberg]

FTSE 100 Outlook and Prediction

We are pretty much on the daily pivot as I write this at 6188 and its either going to rise to 6230 or drop to 6155 from here, and its not overly clear first thing which one its going to do. The 6230 area has a few resistance levels in play, including the 10 day Bianca, whilst the 10 day Raff is at 6243. 6155 is the 100 Hull MA and also S1 on the PRT charts to start with. The bulls managed to just about hold onto the 6200 level so will be keen to build on that work yesterday and if they do then that 6350 is still on the cards, if they can break 6240. However, it can also be said thats its struggling a bit here and a drop down is my slightly preferred option, with 6010 still looking like a possible area to drop to if the bears can break 6075. So not falling in love with the upside as they say! We have month end and quarter end today which can produce some irrational moves as well as NFP news out tomorrow. Generally I am thinking a short around the 6230 area, and a tentative long at 6155, with slightly more bias to the bearish side at the moment.