FTSE 100 Support 6845 6839 6826 6761

FTSE 100 Resistance 6895 6924 6972 6978 7034

Good morning. Decent steady fall on the FTSE 100 yesterday as expected after that Sunday night spike up on the oil news. Needed to trap a few bulls and also finish off the last of the shorters with that spike up. I bet a lot of early Monday morning bulls got burned yesterday! That said the long from 6895 worked well for a nice quick bounce to bag 30 points, We are nearing “Fed Wednesday” now where it looks pretty likely that interest rates will be raised, along with some additional tightening of stimulus. In contrast to the ECB! Mixed performances on Wall Street and Asia overnight sees the FTSE open at the close area from yesterday, around 6885. Its really going to be all eyes on the upcoming economic data. We have daily support today at 6844 so this area may act as the springboard for the Santa Rally, but the bulls need to break 6977 to push higher.

Good morning. Decent steady fall on the FTSE 100 yesterday as expected after that Sunday night spike up on the oil news. Needed to trap a few bulls and also finish off the last of the shorters with that spike up. I bet a lot of early Monday morning bulls got burned yesterday! That said the long from 6895 worked well for a nice quick bounce to bag 30 points, We are nearing “Fed Wednesday” now where it looks pretty likely that interest rates will be raised, along with some additional tightening of stimulus. In contrast to the ECB! Mixed performances on Wall Street and Asia overnight sees the FTSE open at the close area from yesterday, around 6885. Its really going to be all eyes on the upcoming economic data. We have daily support today at 6844 so this area may act as the springboard for the Santa Rally, but the bulls need to break 6977 to push higher.

US & Asia Overnight

Shanghai stocks extended their worst losses in six months and the dollar’s rally faltered as investors weigh the impact of monetary tightening in the world’s two largest economies. Bonds consolidated following a two-month collapse.

Shares in Shanghai slipped even as China’s official data showed stronger-than-expected industrial output and retail sales, while yuan government bonds extended losses. Sovereign debt in most other markets snapped declines as oil failed to build on a rally spurred by OPEC’s deal with rivals to curb production. The yen held its advance versus the dollar, while the Korean won and Indonesian rupiah gained.

Investors are focused on the impact of People’s Bank of China monetary tightening and this week’s Federal Reserve meeting, with inflationary pressures coming to the fore of global central-bank thinking. The market sees 100 percent odds of a rate hike in the U.S. Wednesday, and a two-in-three chance of additional tightening by June. Chinese regulators are pushing money market rates higher and curbing leveraged purchases of both stocks and bonds, just as U.S. President-elect Donald Trump’s throws relations with China into disarray.

“The figures are good but the market sentiment remains cautious after a big drop yesterday,” said Linus Yip, a Hong Kong-based strategist at First Shanghai Securities Ltd. “For the past two months people were quite excited that insurers’ money was helping to push up the market but they did it too drastically.”

Stocks

The Shanghai Composite Index slid 0.7 percent as of 12:40 p.m. local time, after dropping 2.5 percent on Monday, while Hong Kong’s Hang Seng index lost 0.4 percent. Industrial production rose 6.2 percent in November from a year earlier, while retail sales surged 10.8 percent, giving policy makers room to switch focus from stimulus to curbing financial risks.

Almost 60 more stocks fell than rose on the dollar-denominated MSCI Asia Pacific Index, which was little changed. Japan’s Topix Index swang between gains and losses, the Jakarta Composite index lost 0.5 percent and the Philippine benchmark dropped 1 percent.

Australia’s S&P/ASX 200 Index slid 0.3 percent, while New Zealand’s S&P/NZX 50 Index slipped 0.4 percent.

S&P 500 Index futures were little changed following a 0.1 percent decline in the underlying benchmark last session that knocked it from a record high.

Currencies

The yen weakened by 0.1 percent to 115.13 per dollar, following Monday’s 0.3 percent climb.

The won added 0.1 percent versus the dollar amid President Park Geun-hye’s impeachment, while the rupiah and the peso added 0.2 percent.

The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, steadied after sinking 0.6 percent last session, its steepest drop since September.

“With a rate hike at this week’s FOMC fully priced and given the strong rally in the dollar, we are likely seeing some paring of positions,” said Khoon Goh, head of regional research at Australia & New Zealand Banking Group Ltd. in Singapore. “Market participants are also reassessing whether the Trump rally has gotten a bit ahead of itself.”

Bonds

Australian 10-year bonds led gains in the Asia-Pacific, with yields falling three basis points to 2.82 percent.

Japanese notes maturing in a decade yielded 0.075 percent, unchanged, as Nomura International Plc said investors are watching the Bank of Japan’s response to the decline in bonds.

Yields on Treasury notes due in 10 years fell one basis point to 2.47 percent. Rates ended Monday little changed after rising by as much as six basis points to touch 2.53 percent, their highest level since September 2014.

The yield on China’s three-year sovereign bond climbed four basis points to 2.85 percent.

Commodities

West Texas Intermediate crude fell 0.3 percent to $52.67 a barrel, after soaring more than 5 percent on Monday.

U.S. shale output could top 4.542 million barrels a day, a modest increase from December forecasts, the country’s Energy Information Administration said Monday.

The U.S. forecast comes after the Organization of Petroleum Exporting Countries agreed to cut output by 1.2 million barrels a day starting in January, and other countries led by Russia agreed to trim production by 558,000 barrels a day.

Copper futures lost 0.6 percent, while zinc declined 0.5 percent.

[Bloomberg]

FTSE 100 Outlook and Prediction

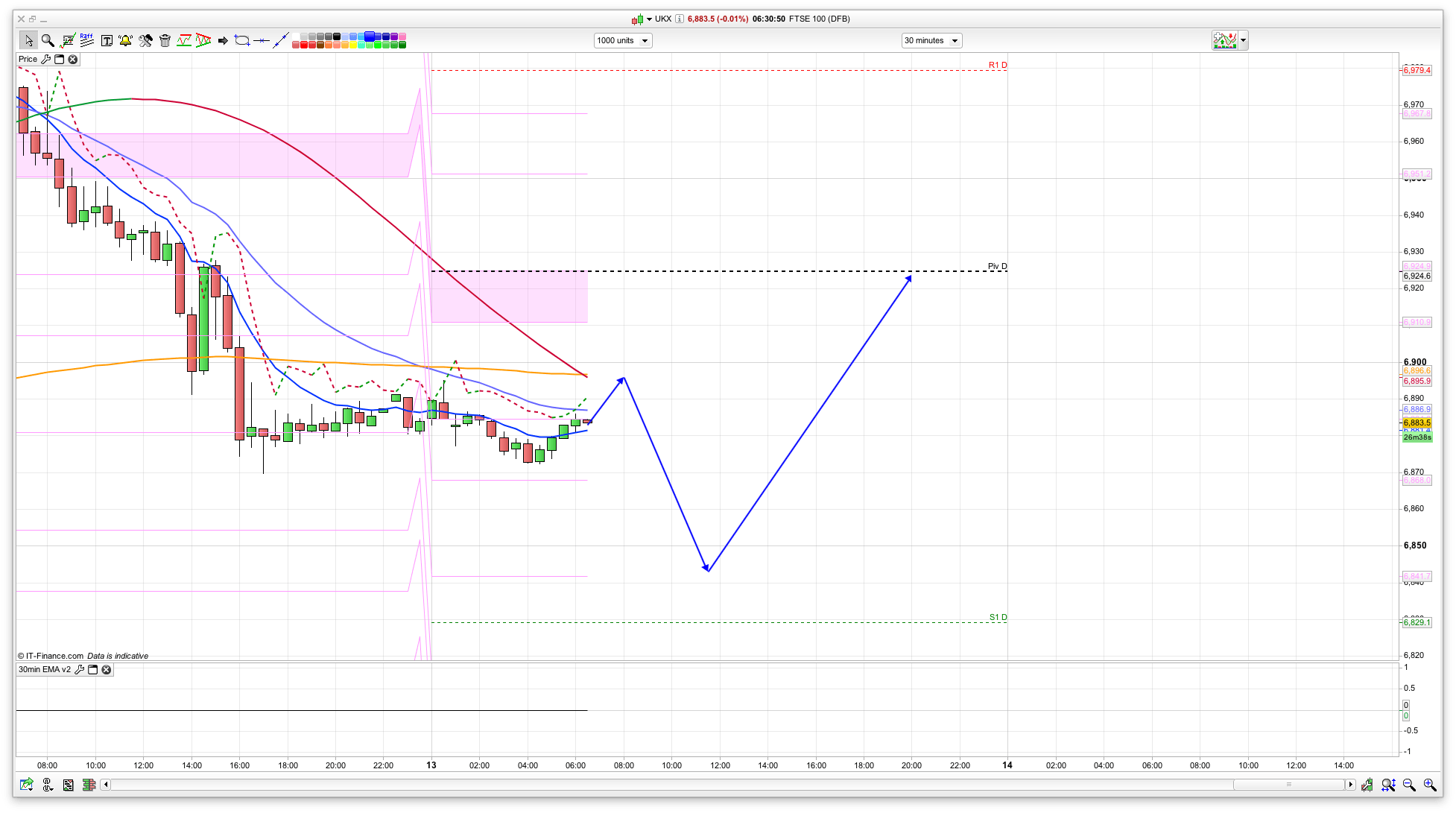

As we get nearer to the Fed decision on Wednesday we will likely see a bit more chop (again!). However, for today I am watching 3 main areas – initial resistance at the 6895 area, support at 6845, and then bigger resistance at 6978. If we dip down to 6845 area then I feel that a long here is definitely worth a go as we have 10 day Bianca and 25daily ema support here, for a run back towards 6900. This area may even act as a springboard for the Santa Rally to kick in. Bet there are some bulls willing it to rise now as well! Below 6845 then 6815 is the line in the sand and it will get pretty bearish if it breaks below this.

Resistance wise we have 6978 on the 2 hour char and the bulls will have to clear this to push higher in the next few sessions. If not then the Santa Rally probably wont start till next week. We are also probably seeing some pricing in of rate rises to be announced on Wednesday. Prior to that level we have 6895 on the 30min which we are not far off to start with. Whilst it is initial resistance and I think that we might see a reaction there I think a further test later on today is likely to break through that level. So, its a tentative buy the dip at 6845 really and see what it does.

6870 has held well so far; rise to 6924 maybe now

6924 done, 6970 next