Support 6172 6160 6153 6130 6109 6068

Resistance 6190 6194 6226 6239 6261

Good morning. A fairly decent day yesterday that saw the longs come good despite that weird start. The Gold short from 2018 worked out really well. Meanwhile UK manufacturing unexpectedly returned to growth in May as a closely-watched survey showed uncertainty surrounding the Brexit vote had “no significant effect” on activity for most businesses. Markit’s latest survey of the sector showed new orders “remained subdued” last month, despite the slight uptick in activity. Growth was driven entirely by domestic orders as new export business fell for the fifth consecutive month. The sector also recorded the fifth straight month of job losses.

Asia slightly weaker as well after Japan held back on expected stimulus.

US & Asia Overnight from Bloomberg

Japanese stocks fell by the most in a month and the yen strengthened after Prime Minister Shinzo Abe held back a widely expected fiscal stimulus package. Oil retreated and the euro rose before Vienna meetings of OPEC and the European Central Bank.

The Topix index dropped as much as 2.4 percent and the yen gained ground against all of its major counterparts. U.S. crude traded near $49 a barrel before the Organization of Petroleum Exporting Countries meet to discuss production policy amid rising U.S. inventories. The euro climbed to a one-week high before an ECB policy review, while the British pound firmed following its steepest two-day loss since March. Haven assets including gold and U.S. Treasuries advanced, while a sale of 10-year sovereign debt in Japan drew the strongest demand in almost two years.

Global markets have entered June on a circumspect footing with the OPEC and ECB meetings Thursday setting the stage for a month that will also see the U.K. vote on whether to remain in the European Union and a possible interest-rate increase by the Federal Reserve. Wednesday data showed the U.S. manufacturing sector grew more than forecast last month and American employment figures this week will help shape expectations for the timing of the next rate hike. Fed Funds futures indicate a 22 percent chance of a move at the June 14-15 meeting.

“The economic situation in America may be solid, but there are still fears that the rest of the world won’t be able to withstand higher U.S. interest rates,” said Mitsushige Akino, a Tokyo-based executive officer at Ichiyoshi Asset Management Co. “If the OPEC meeting results in a negative outcome, we’ll see even more risk being taken off the table.”

The ECB’s rate announcement is due at 1:45 p.m. in Vienna and President Mario Draghi is expected to refrain from adding to record monetary stimulus. U.K. Prime Minister David Cameron will be answering questions about the nation’s relationship with the EU as he seeks to convince voters to support continued membership before a June 23 referendum. A U.S. jobs report from the ADP Research Institute is forecast to show 173,000 workers were taken on in May, up from 156,000 the previous month. Official employment figures are due Friday.

Stocks

The Topix lost 1.9 percent as of 1:49 p.m. Tokyo time. It slid 1.3 percent on Wednesday as Abe announced a planned sales-tax hike will be postponed until October 2019 and vowed to take “bold” economic steps in the autumn, without giving further information. Expectations that fiscal stimulus was imminent were fueled by local newspaper reports, including a Yomiuri Shimbun article that said the premier would unveil a “large” extra budget on Wednesday.

Honda Motor Co. tumbled as much as 4.1 percent and Toyota Motor Corp. dropped 1.1 percent after their U.S. sales fell last month by more than analysts estimated. Yahoo Japan Corp. rallied more than 3 percent after the Nikkei newspaper reported SoftBank Group Corp. may boost its ownership of the search engine operator. Midea Group Co. fell 1 percent in Shenzhen as Germany explored ways to stop a takeover of robot maker Kuka AG by the Chinese company.

Futures on the S&P 500 Index declined 0.2 percent, after ending the last session little changed. While Wednesday’s manufacturing data was better than economists projected, a separate report showed U.S. construction spending unexpectedly dropped.

Currencies

The yen strengthened 0.4 percent to 109.16 per dollar, after surging 1.4 percent in the last two trading sessions.

“This move in the yen is maybe more about a risk-off move, than sort of a positive sentiment,” Sassan Ghahramani, chief executive officer of SGH Macro Advisors, said on Bloomberg TV. “People got a little bit ahead of themselves and were expecting some sort of announcement on a supplementary budget. When that didn’t come, I think there was a bit of a disappointment trade.”

The Bloomberg Dollar Spot Index fell 0.1 percent, after sliding 0.4 percent in the last session. Investors are paying close attention to U.S. data after Fed officials indicated a potential interest-rate hike as soon as this summer was contingent on continued improvement in the economy. Friday’s payrolls data is projected to show the number of workers increased by 160,000 in May, matching the advance in April.The euro strengthened 0.2 percent, after surging 0.5 percent on Wednesday, and the British pound rose from a two-week low before Cameron’s EU question-and-answer session in a Sky News television program on Thursday. The U.K. currency sank 1.5 percent over the last two days as polls indicated support is growing for the country to leave the bloc.

Australia’s dollar fell 0.2 percent versus the greenback, retreating from near a two-week high. The ringgit dropped to a three-month low as lower oil prices dimmed prospects for Malaysia, Asia’s only major net exporter of crude.

Commodities

West Texas Intermediate crude declined 0.1 percent to $48.98 a barrel, falling for a fifth straight session. Saudi Arabia was discussing ideas with fellow OPEC members including restoring a production target scrapped in December, according to delegatesfamiliar with the situation. Still, no formal proposal has yet been made and Iran’s minister said a new output ceiling wasn’t an attractive plan.

Gold rose 0.2 percent, after falling on 10 of the last 11 trading days. Copper and nickel fell less than 0.3 percent in London.

Bonds

U.S. Treasuries due in a decade rose for a third day, pushing their yield one basis point lower to 1.83 percent. Similar-maturity notes in Japan yielded minus 0.11 percent after a sale of the tenor achieved the highest bid-to-cover ratio since August 2014. [Bloomberg]

FTSE 100 Outlook and Prediction

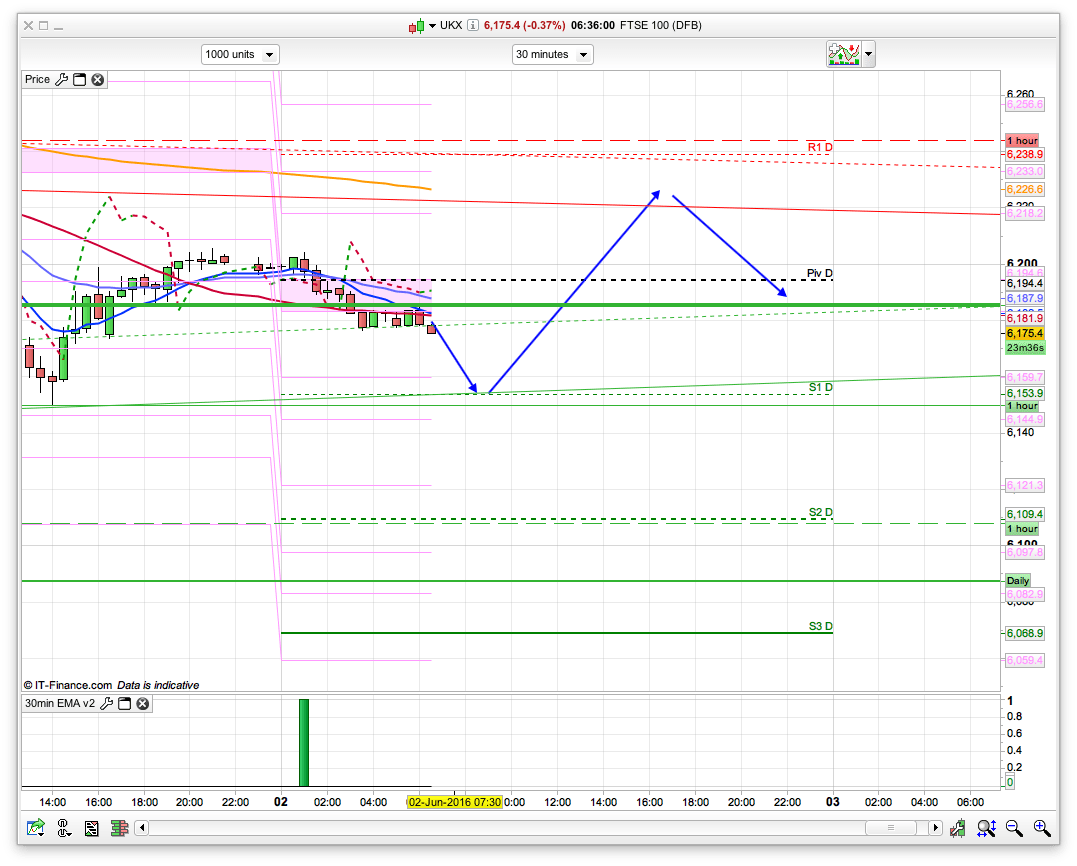

There are a couple of areas of interest for today which is resistance at the 6226 area, and support at the 6155 area. The former is the 200ema on the 30min chart and also a resistance on the 2 hour chart, whilst the 6155 was decent support yesterday and we have S1 and the 20 day Bianca channel here for today. Its not a particularly clear picture (the FTSE has certainly been hard to read and been behaving strangely the past few sessions), however I feel that these levels are worth a go. It did look like the bulls might be able to hold 6200 last night after that bounce from 6150, helped of course by the divi hunters, though the Japan stimulus news scuppered that a bit overnight. It is a level that they will be keen to get back above though, as we have dropped off from the 6295 seen out of hours on Monday. Holding above this level might well change the picture to a slightly more bullish one, as at the moment its fairly bearish in terms of the moving averages. First hurdle for the bulls today is 6194, the daily pivot, so we shall see if they are able to break that fairly early on. If the bears break 6150 then we will probably be on for quite a slide (6000 maybe?) so bear that in mind.

Hello All, has everyone given up?! I’ve been a bit remote as been travelling the Country picking Children up from Uni. In case anyone had an doubts at all I can tell you that the M25 sucks!

Anyway, yesterday was a bit a frustrating, got long at 210, 175 but didn’t get any at 150. Sold the 175’s at 195 last night so small long at 10 which I’m running.

Brexit punt came good, got out of half at 76, I think it could get back down to 70-ish or 2and a bit to 1.

Hello Chippy, Yeah it’s bit quiet over here today!

I guess Anstel is still holding his longs and tmfp is probably still having fun with his bike and I guess WSF is in gym or waiting for a dip to buy lol 🙂

I managed to grab couple of nice shorts this morning at 6212, 6218, 6215 and took +35 and went long at 6200 after 10:00am for +15.

It’s nearly time for ECB now so I am just being bit careful however if we get to 6240 or 6270 then I will be heavy short in this area.

GL

Well the ECB did not spark any great fireworks YAWN