FTSE 100 Support 6742 6736 6692 6655 6647 6612

FTSE 100 Resistance 6790 6808 6828

Good morning. As was widely expected the BoE cut interest rates yesterday by a quarter of a percent, and increased QE – sending the FTSE 100 up 100 points in fairly short order. Bit unlucky that the 6630 long got stopped out near the lows before the bounce though. The FTSE 100 has held up well since, with 6800 looking likely (though we do have the 20 day Bianca at 6790).

One thing that was slightly glossed over but is still significant is the growth downgrade from 2% to 0.8%. Whilst these are always just guesses anyway, this action and that statement does make you feel like there are trying to pre-empt anything negative that may be on the horizon. I think mid to end of August could be an interesting time for the bears as we could start another down leg then. Invocation of Article 50 around then maybe?

Today we have NFP in the US at 1330 so expect more movement around 1330, forecast is 180k, versus 287k previously.

US & Asia Overnight from Bloomberg

- Bank of England reduced key rate to record low on Brexit

- Focus now shifts to U.S. payrolls as greenback dawdles

Asian stocks rose amid a surge in government debt after the Bank of England’s policy easing soothed concern over the impact of the Brexit vote and as oil declined toward $41 a barrel. The dollar meandered ahead of U.S. jobs data.

Consumer and energy stocks drove equity gains, paring the Asian benchmark’s first weekly drop in about a month. Yields on 10-year Australian and Japanese debt sank at least one basis point, as the notes joined a rally in bonds globally. The yen was little changed for a second day against the dollar, while the Australian currency strengthened. U.S. crude slid after the biggest two-day increase in more than a month as prices fluctuated following a drop into a bear market this week.

The BOE cut growth forecasts for the U.K. by the most ever as policy makers unveiled a stimulus package aimed at containing the fallout from the British decision to leave the European Union. Investors are now switching their focus to Friday’s update on nonfarm payrolls in the U.S. Economists predict the report will show continued improvement in the labor market, a key factor for the Federal Reserve, which is mulling whether to stick to its plan to continue tightening monetary policy in 2016.

“The BOE’s move looked like an inevitable choice, but it was taken as a positive signal for investors in terms of boosting expectations for increased liquidity in the global market,” said Heo Pil Seok, chief executive officer at Midas International Asset Management Ltd. in Seoul, which oversees about 10 trillion won ($9 billion). “While improved sentiment is reflected especially in the equities market today, the U.S. data is something to keenly watch as it may fuel concerns of a rate hike.”

Payrolls probably rose by 180,000 workers in July, following a 287,000-person increase in June, according to the median of economists’ estimates compiled by Bloomberg. The jobless rate is projected to fall to 4.8 percent, from 4.9 percent in the previous month.

Stocks

The MSCI Asia Pacific Index climbed 0.7 percent as of 12:41 p.m. Tokyo time, with groups of consumer-discretionary shares and energy producers rising at least 1.2 percent.

In Australia, the S&P/ASX 200 Index increased 0.4 percent, as the Kospi index in Seoul added 0.8 percent. New Zealand’s S&P/NZX 50 Index was up 0.2 percent after rising 0.3 percent last session. The measure is due to snap a five-week run of gains, falling 0.5 percent so far this week. The Topix index in Japan was little changed after earlier rising as much as 0.5 percent. It’s down 3 percent this week, the most in a month. In Hong Kong, the Hang Seng index jumped 1.4 percent and the Hang Seng China Enterprises measure advanced 1.5 percent. Futures on the S&P 500 Index were up 0.2 percent to 2,163, after the underlying benchmark added less than one point on Thursday.

The U.S. “employment number is the catalyst for the market — that’s what is going to rule the pricing trends over the next few weeks,” said Jim Davis, regional investment manager at the Private Client Reserve of US Bank, which oversees $128 billion.

Bonds

Australian bonds drove gains in Asia, with yields on debt due in a decade down six basis points, or 0.06 percentage point, to 1.89 percent. Similar maturity Japanese notes yielded negative 0.090 percent, down one basis point, while rates on New Zealand bonds four basis points to 2.18 percent.

Yields on 10-year Treasuries shed another one basis point to 1.50 percent, after declining five basis points over the past two sessions. U.S. debt climbed with European bonds last session as the BOE’s move reinforced the trend for monetary easing globally.

Almost all economists in a Bloomberg survey had forecast the BOE would cut its benchmark interest rate and most predicted other measures as well. Futures trading showed about a 47 percent chance that the European Central Bank will ease by year-end while wagers on a 2016 increase by the Fed have been cut to 37 percent from 59 percent two months ago.

Currencies

The Australian dollar climbed to a three-week high after the nation’s central bank gave no interest-rate guidance in its quarterly statement Friday and left its growth and inflation forecasts little changed.

The Aussie rose 0.4 percent to 76.59 U.S. cents, after touching 76.60, the strongest level since July 15. It has appreciated by 0.8 percent since July 29, adding to last week’s 1.8 percent advance.

The pound rose 0.2 percent to $1.3129, following a 1.6 percent drop Thursday after the Bank of England cut interest rates for the first time since 2009 and said it would buy corporate bonds to combat sluggish growth.

The Bloomberg Dollar Spot Index, which tracks the U.S. currency against a basket of its major peers, has gained less than 0.1 percent since July 29, when it completed a 1.7 percent weekly decline. It was little changed on Friday.

Commodities

West Texas Intermediate crude slipped 0.9 percent to $41.56 a barrel following a two-day, 6.1 percent rebound. U.S. government data Wednesday showed gasoline inventories decreased, while crude stockpiles unexpectedly rose for a second weekly gain. Both are at the highest seasonal level in at least two decades.

Aluminum and zinc rallied in the wake of losses on Thursday, climbing at least 0.2 percent in London. Gold for immediate delivery was little changed at $1,360.81 an ounce before the payrolls data, headed for a 0.7 percent climb in the week, the safe-haven asset’s second straight weekly advance.

Corn for December delivery headed for a 3 percent decline this week. November-delivery soybeans rose 1.2 percent to trim this week’s 3.5 percent drop. [Bloomberg]

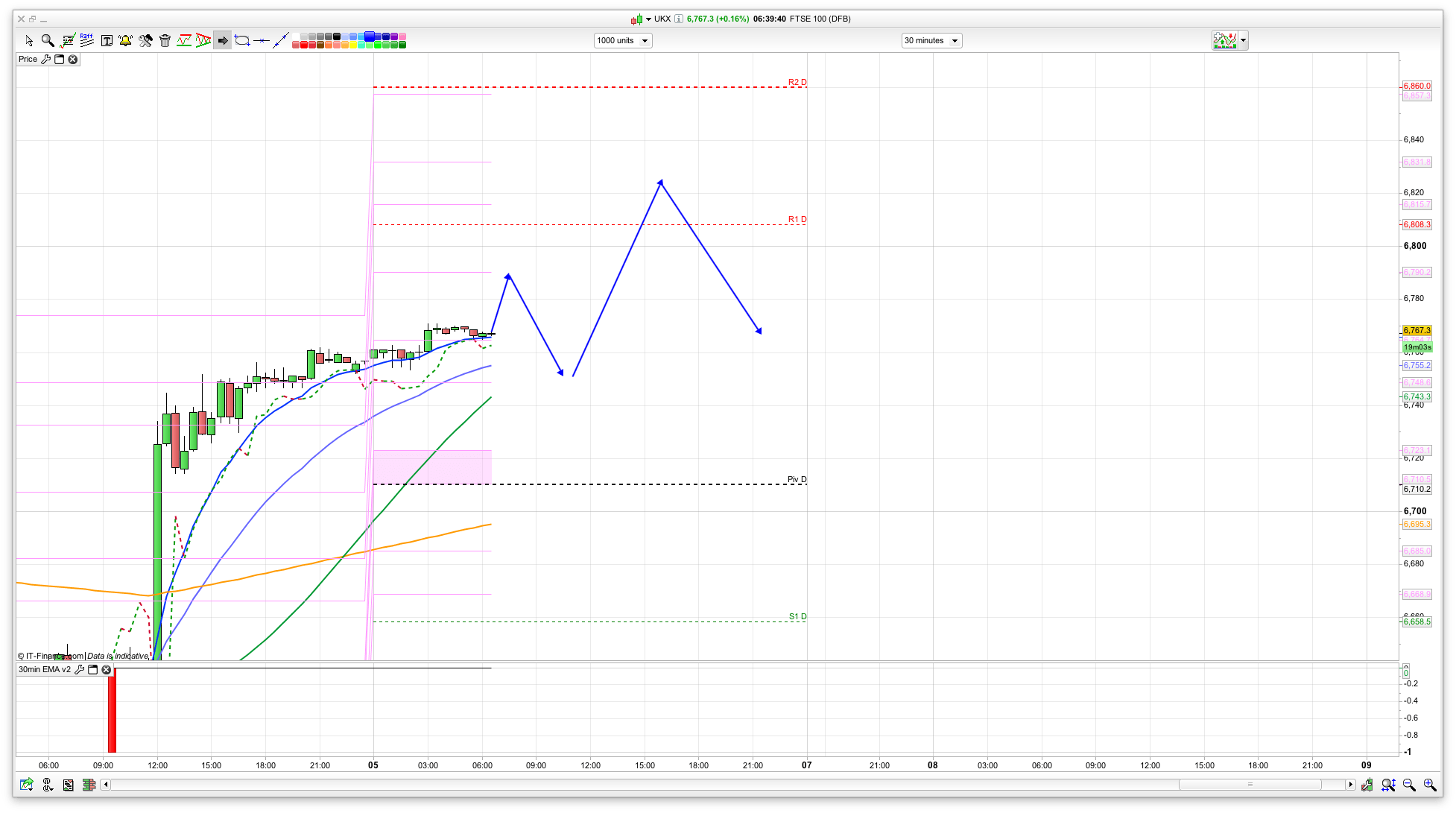

FTSE 100 Outlook and Prediction

Bit of a tricky one to call today with that rise yesterday distorting the technicals a bit. However, I am watching 6790 as initial resistance with 6828 above that which is resistance on the daily chart. Both these levels could be worth shorting from and see how they go. As mentioned above its NFP news today at 1330 so likely to get some movement then.

Support wise, 6740 is first up, with the pivot at 6736 and then the 200ema on the 30min at 6692. The momentum is with the bulls again so there probably wont be massive downside today – more of an up then down day and ending back where we started I am thinking – around 6750.