FTSE 100 Support 6778 6752 6727 6685 6658 6625

FTSE 100 Resistance 6797 6804 6818 6825 6850

Good morning I hope you had a good weekend. Another strong close to the week after the positive US Jobs (NFP) data on Friday, and the FTSE flirting with the 6800 level. Didn’t quite manage to break and hold above that last week, but maybe today, though we are once again testing the top of the Bianca channels. The main story early this week will be the 36 point dividend on Wednesday.

US & Asia Overnight from Bloomberg

Asian equities climbed toward a one-year high and copper rallied after U.S. jobs data burnished sentiment toward the world’s largest economy. Thailand’s stocks and currency rose after voters backed a new constitution, while South Korean assets were buoyed by a debt-rating upgrade.

The MSCI Asia Pacific Index gained for a third day, led by Japanese shares as the greenback extended its advance against the yen following the bigger-than-estimated increase in American payrolls reported on Friday. The baht was Asia’s best-performing currency, while the won erased losses after S&P Global Ratings raised South Korea’s credit ranking. Crude traded near $42 a barrel amid a pickup in U.S. drilling and copper rebounded from a four-week low. Sovereign debt fell in Australia and Japan.

U.S. data showing improvements in employment, retail sales and factory output have bolstered confidence that the world’s biggest economy can withstand faltering growth elsewhere, reviving speculation that the Federal Reserve will raise interest rates this year. China’s exports and imports dropped last month in dollar terms, a report showed Monday after Asian equities retreated last week.

“A possible pullback in U.S. jobs figures had kept some on guard, and the latest data have quenched those concerns,” said Hitoshi Asaoka, a senior strategist with Mizuho Trust & Banking Co. “It does leave room for a rate increase within this year.”

Odds on the Fed increasing rates by the end of this year rose to 47 percent in the futures market after the U.S. jobs report, up from 37 percent on Thursday. Exports from China, the world’s biggest trading nation, declined 4.4 percent from a year earlier in July and its imports dropped 12.5 percent. Germany, Europe’s largest economy, is scheduled to report industrial output figures on Monday and France has a gauge of business sentiment due.

Stocks

The MSCI Asia Pacific Index added 1.2 percent as of 1:51 p.m. Tokyo time. Japan’s Topix index jumped 1.7 percent, after sliding 3.2 percent last week. Hong Kong’s benchmark was headed for its best close since December, while gauges in Indonesia, Taiwan and Thailand climbed to their highest levels in more than a year.

Futures on the S&P 500 Index were little changed, after the gauge climbed 0.9 percent in the last session to an all-time high. With more than three-quarters of the benchmark’s members having released quarterly results so far, 78 percent have beaten analysts’ profit estimates.

Currencies

The yen weakened 0.2 percent to 102.01 per dollar, after sinking 0.6 percent on Friday, and New Zealand’s dollar lost 0.4 percent. All of the 16 economists surveyed by Bloomberg predict the Reserve Bank of New Zealand will cut its benchmark interest rate to a record at a review this Thursday.

The baht climbed 0.4 percent after voters approved a military-backed constitution, putting the nation on track for elections next year. The won recovered from a loss of as much as 0.6 percent after S&P raised South Korea to AA, its third-highest rating.

The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, held near a one-week high. U.S. payrolls increased by 255,000 workers last month, following a 292,000 gain in June that was larger than previously estimated. Hedge funds and other large speculators boosted bullish dollar bets to the most since February last week, even before the payrolls report.

Commodities

Gold for immediate delivery rose 0.2 percent, after dropping 1.9 percent to a one-week low on Friday. The growing prospect of a Fed rate hike dims the appeal of the precious metal versus yield-paying assets.

“Gold was the big casualty from the strong jobs data,” analysts at Australia & New Zealand Banking Group Ltd. wrote in a note. “The case for a Fed hike was bolstered, but the market is not getting too gung-ho.”

Copper rose 0.8 percent in London, aluminum climbed to a three-week high and nickel was headed for its strongest close in a year.

West Texas Intermediate crude rose 0.1 percent to $41.86 a barrel after falling 0.3 percent in the last session. Rigs targeting crude in the U.S. increased by seven to 381 last week, the highest level since March, Baker Hughes Inc. said Friday.

Soybeans climbed as much as 1.5 percent in Chicago amid strong demand for U.S. exports. China’s soybean imports rose to 7.76 million metric tons in July from 7.56 million tons in June, data showed Monday. Wheat for September also advanced as much as 1.5 percent amid concern about the outlook for European crops.

Bonds

Australian bonds led losses in the Asia-Pacific region, with 10-year yields increasing by eight basis points to 1.94 percent. Rates on similar-maturity Japanese and New Zealand debt rose by about five basis points.

The yield on Treasuries due in a decade was little changed at 1.59 percent, having increased by nine basis points on Friday. That compares with the all-time low of 1.32 percent reached last month.

“The economic situation is not so gloomy,” said Park Sungjin, the head of principal investment in Seoul at Mirae Asset Securities Co., which oversees $8 billion. “We have seen the bottom in Treasury yield levels,” he said, predicting the 10-year yield will be above 1.90 percent by the end of December.

South Korea’s 10-year yield was up two basis points at 1.41 percent, having climbed as high as 1.44 percent prior to the announcement of S&P’s debt-rating upgrade.

The cost of insuring Asia-Pacific bonds against default fell to the lowest level in about a year, according to prices from Australia & New Zealand Banking Group Ltd. and data provider CMA. [Bloomberg]

FTSE 100 Outlook and Prediction

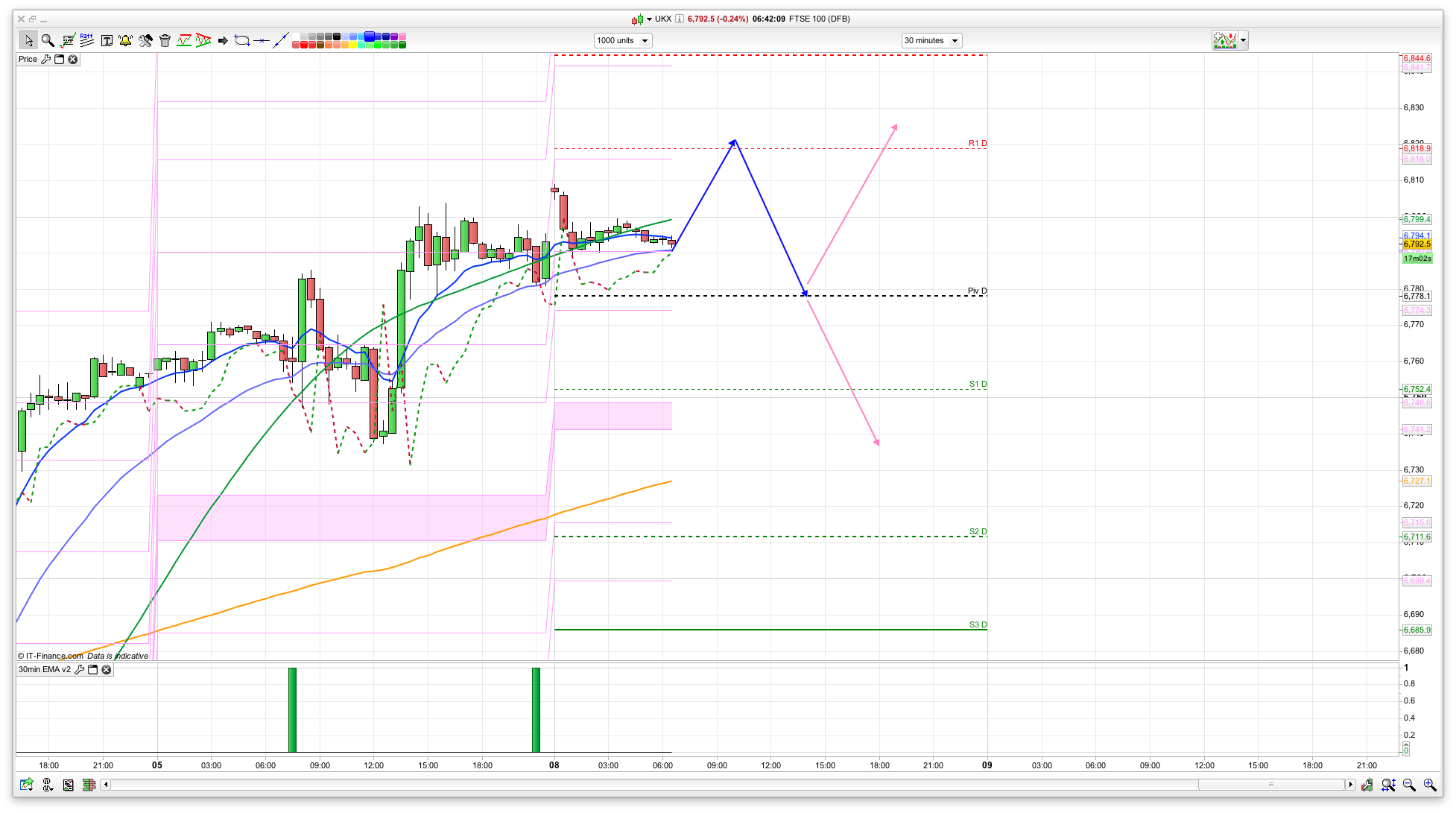

For today I am expecting a bit of a rise and then fall. The 6820 level looks good for a shorting area as we have the R1 level at 6819 and the top of the 10 day Raff at 6826 as well. We haven’t really tested the Raff channels much recently, only bouncing off the bottom of the 10 day the other day at the 6620 level.

So, if we get a morning rise to that level then a dip back to the pivot at 6780 that play looks viable. At that point it will either bounce back or decline further, hence the pink arrows as it could really do either. If the latter then the 6726 and 6690 levels open up as support, with the bottom of the 20 day Bianca below that at 6658. 6720 is the 200ema on the 30min, and also the 100 Hull MA on the 2 hour, along with the coral at 6690ish on the 2 hour.

I am thinking more that shorting the rallies for the moment is the best play (ignoring the divi for the moment as that will be Wednesday), mainly as we are just at the top of the Bianca channels with this rate cut bounce having taken us quite far quite fast, and also the top of the Raff channels coming into play as well. I still have mid to end August pencilled in as a bearish period to watch so we may see some more dramatic declines then.