FTSE 100 Support 6640 6635 6630 6629 6610 6600 6548

FTSE 100 Resistance 6668 6671 6718 6812

Good morning. So here we are on what is being billed as Super Thursday, the main reason being we have the BoE rate decision. We also have the MPC meeting minutes, QE report and Inflation report. The BoE is widely expected to cut interest rates but whether its today or not remains to be seen. We may well get a bit of buy the rumour this morning leading up to this announcement at 12pm.

US & Asia Overnight from Bloomberg

- Drop in U.S. gasoline stockpiles sparks crude clawback

- S&P 500 snapped two-day decline as energy shares rose

Asian stocks advanced, rebounding from their worst day since the aftermath of the Brexit vote, as crude oil held onto its recovery and high-yielding currencies climbed.

Mining shares and energy producers drove the regional index up from its lowest level since June 24, the day when referendum results showed Britain had decided to leave the European Union. U.S. crude extended gains into a second session after the steepest drop in American gasoline supplies since April soothed concern over a glut. The rebound burnished risk sentiment, with gold holding losses as Australian government debt continued its retreat. The Aussie dollar strengthened with the South Korean won and the Malaysian ringgit. Metals declined amid concern about increased supply from China.

The global equity rebound that took hold in July started to falter as August opened, with oil descending into a bear market and data failing to bolster confidence in the world economy. While central banks and governments have signaled unprecedented support, Japan’s latest efforts — which include monetary and fiscal stimulus — haven’t had their intended effect amid concern the plans won’t be enough to revive price growth. The Bank of England is expected to cut benchmark interest rates on Thursday, while jobs data in the U.S. Friday could provide clues as to the outlook for Federal Reserve policy.

“The theme remains dominant in markets that monetary policy has effectively done as much as it can and that reflation, if required, should come via other means,” Sharon Zollner, a senior economist in Auckland at ANZ Bank of New Zealand Ltd., said in a note to clients. “The reality is that interest rates remain at record-low levels and, in an environment of moderate growth and low inflation, that is supportive of higher-yielding assets and Asia-Pacific markets should continue to benefit, as long as the growth picture holds together.”Australia reported weaker than forecast second-quarter retail sales on Thursday, and an update on consumer confidence in Thailand is due. China issues figures on its current-account balance, while in Japan, Toyota Motor Corp. — the biggest-weighted stock on the Topix gauge — will report earnings.

Stocks

The MSCI Asia Pacific Index rose 0.7 percent as of 1:54 p.m. Tokyo time, following last session’s 1.9 percent slide. The index, which jumped 5.8 percent in July, is down about 0.9 percent this week.

The Topix climbed 0.7 percent as the yen halted its advance. The stocks gauge had also dropped by the most in more than five weeks on Wednesday.

Oil and gas companies led Australia’s S&P/ASX 200 Index to a 0.4 percent rebound, as the Kospi index in Seoul gained 0.3 percent following last session’s 1.2 percent decline.

Futures on the S&P 500 were little changed, following a 0.3 percent increase in the underlying index on Wednesday. The U.S. benchmark had fallen 0.8 percent over the previous two sessions.

“There’s slow movement in a market that’s looking for a reason to go up or go down — it just hasn’t found any,” said Jeff Carbone, managing partner of Cornerstone Financial Partners, which oversees almost $1.1 billion in assets in Charlotte, North Carolina. “We haven’t seen that breakout that would suggest the market is based on fundamentals, it’s still very tied to central banks.”

In Hong Kong, Hang Seng and Hang Seng China Enterprises indexes each advanced at least 0.5 percent. Chinese shares declined 0.2 percent.

Currencies

The yen was at 101.25 per dollar, after retreating 0.4 percent on Wednesday. NBC Financial Markets Asia said a speech from the Bank of Japan’s Deputy Governor Kikuo Iwata raised doubts about the central bank’s easing stance.

Japan’s currency has gained about 1 percent this week, as traders react to the BOJ’s decision last Friday to only bolster purchases of exchange-traded funds, as well as to a fiscal package flagged Tuesday by Prime Minister Shinzo Abe.

The Aussie added 0.3 percent, erasing its decline last session. The won gained 0.3 percent, as the ringgit bounced with oil, climbing 0.5 percent from a four-day low.

The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, was down 0.1 percent after rising 0.3 percent on Wednesday, when emerging-market currencies led declines.

Chicago Fed President Charles Evans told reporters Wednesday that a rate hike “could be appropriate this year.” Odds on the Fed boosting benchmark borrowing costs in 2016 have dropped to 39 percent, with last week’s weaker-than-expected U.S. growth data damping expectations of tightening.

Bonds

Australian sovereign bonds led a retreat, with 10-year yields rising four basis points, or 0.04 percentage point, to 1.97 percent, building on Wednesday’s 11 basis-point jump. Similar maturity Japanese debt yielded minus 0.09 percent, up 1/2 a basis point.

Treasuries were little changed, with yields on notes due in a decade steady at 1.55 percent. Ten-year rates jumped at the start of this week, as the record-setting rally in global bonds appeared to falter.

Commodities

West Texas Intermediate crude extended Wednesday’s 3.3 percent rebound., rising 0.7 percent to $41.11 a barrel after U.S. government data showed gasoline stockpiles fell by 3.26 million barrels last week, the most since April.

WTI is still down about 1 percent this week, after the commodity sold off on Monday and Tuesday amid resurgent concern over a global glut. Citigroup Inc. to Bank of America Merrill Lynch predicted the slump would be short-lived, while Societe Generale SA said the price correction would be limited due to a better balance between supply and demand.

“We’re seeing rebalancing,” Scott Darling, regional head of oil and gas at JPMorgan Chase & Co., said in a Bloomberg TV interview. “We think in the near-term, oil will be under pressure because demand is moderating.”

Gold for immediate delivery dropped 0.5 percent to $1,351.77 an ounce, after declining 0.4 percent on Wednesday. Last session’s retreat halted the precious metal’s longest rally in a month.

Aluminum fell as much as 0.7 percent to $1,631 a metric ton on the London Metal Exchange. Copper declined 0.4 percent, while nickel fell 1.3 percent. [Bloomberg]

FTSE 100 Outlook and Prediction

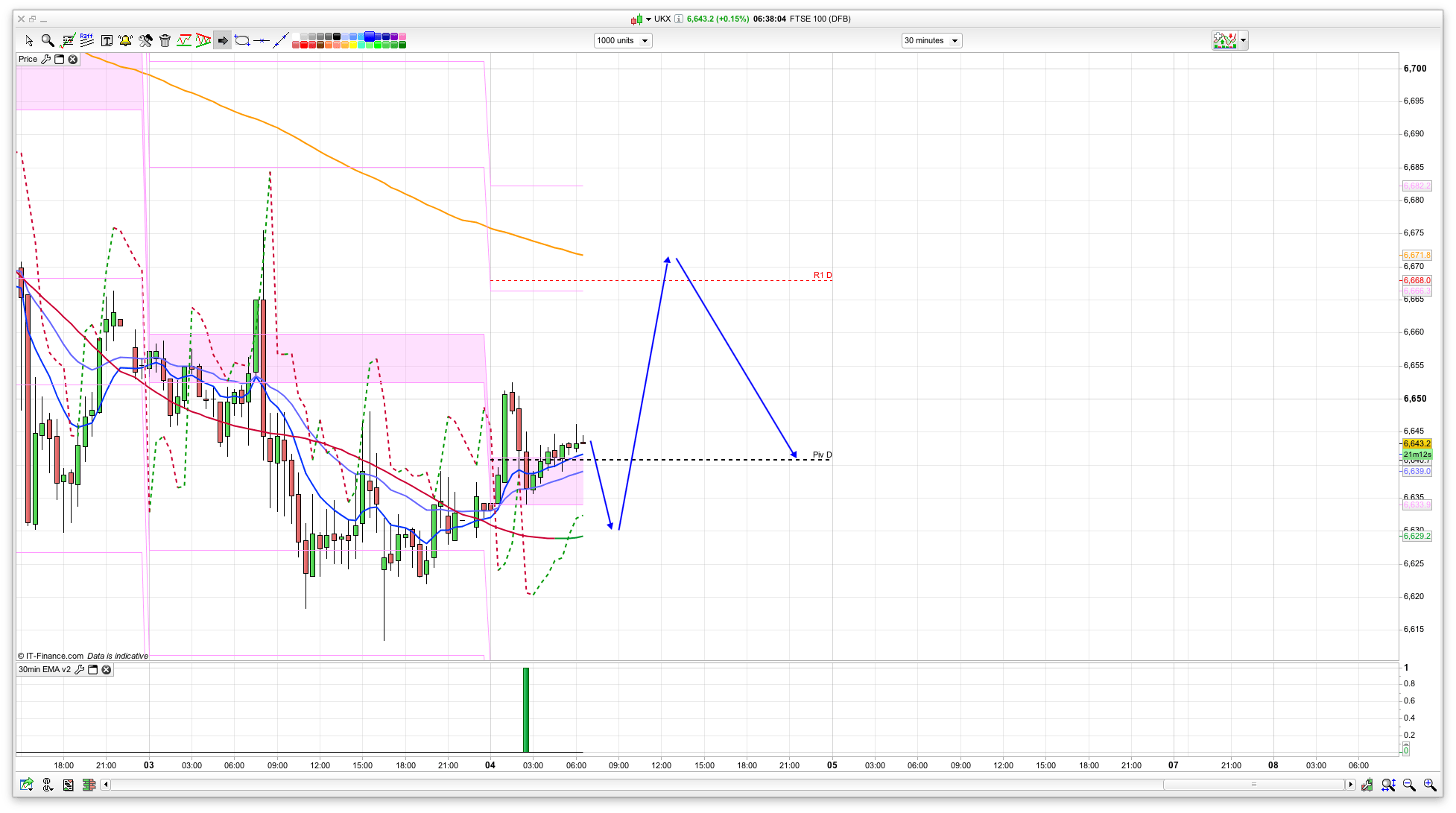

Today its all about the BoE at 12pm so going to be a bit more “gambly” than usual. We will quite possibly see some buy the rumour this morning as its been hinted that there will be a rate cut (personally I think they will probably stay the same). There are quite a few decent support levels popping up around the 6620/6630 area this morning, with that level also holding well yesterday. Resistance wise we have 6671 again, then the top of the 10 day Bianca at 6718 – might be worth a short off this level if seen, even though its not in the trade plan. If there is a rate cut then that should kick the bulls into life and we will probably break higher. The range at the moment is 6630 to 6670 for this morning.

The divi yesterday saw a little bit of a rise towards the bell but not a massive amount – next week should see more of a rise as its 36 points.

Plan for this morning is to buy the rumour, then probably sell the news if things remain as they are. If not then see if it rises past 6670 and hop on long.