FTSE 100 live outlook prediction analysis for 17th August 2020

Retail sales in the US rose by another 1.2pc in July, rising to new record highs as consumers buy more than they did before the pandemic struck. The increase is slightly smaller than economists anticipated, with sales of cars dropping a touch, but indicates this part of the world’s largest economy has fully recovered.

“The retail sales figures are encouraging because they suggest the recovery has continued to grind on even in the face of the resurgence in virus cases,” said Michael Pearce at Capital Economics. “Admittedly, the expiry of additional Federal unemployment benefits at the end of July poses a downside risk to spending in the near term, but with virus infection numbers falling again the high-frequency indicators have continued to edge higher in early August.”

Industrial production also climbed by 3pc on the month, led by reopening car factories ramping up to increase output by more than a quarter.

However, manufacturing is still down by around 8pc compared to 2019 levels. “The scope for further large gains on factory re-opening appears limited so additional gains will be determined much more by underlying economic fundamentals,” said economist James Knightley at ING. “Based on the high-frequency consumer sector data there is evidence of a plateauing in the recovery and it will be hard for the manufacturing sector to buck that trend.”

Here’s a reminder of some of Friday’s top stories:

- Chinese data showed the country’s economic comeback may be losing momentum, with retailer sales down 1.1pc year-on-year.

- Second-quarter GDP figures for the EU showed a record 12.1pc fall in output as the pandemic ravaged the bloc.

- European stock markets dropped, with the travel sector under pressure after Britain expanded travel restrictions.

- The European Commissioned announced it has reached a deal with AstraZeneca to buy 300m doses of the pharma giant’s Covid-19 vaccine.

- US retail sales growth missed expectations, with signs a bounceback in demand is losing steam. Industrial production also rose at a slowing pace.

Fraying Relations

The almost daily drumbeat of tensions between the U.S. and China shows little sign of letting up, while touching on everything from the coronavirus to trade to defense issues to monetary policy. U.S. President Donald Trump has made his tough positions on China a key element in the lead-up to the U.S. presidential election — now less than three months away —and he seems intent on keeping up the pressure. Tensions have been mounting since the Covid-19 pandemic spread across the globe early this year. Some China hawks in the Trump administration, from Secretary of State Michael Pompeo to White House trade adviser Peter Navarro, see a historic opening to re-balance decades of U.S.-China relations. Senior officials from Washington and Beijing late last week postponed trade talks that had been set for this past weekend to discuss the status of the “phase one” trade deal signed early in the year.[Bloomberg]

FTSE 100 Outlook | Trading Signals | Forecast | Prediction | Analysis

Stocks in China climbed after the central bank’s injection of cash raised hopes of more supportive monetary policy, with equities elsewhere trading mixed as investors assessed soured U.S.-China ties. The dollar slipped. The Shanghai Composite was more than 2% higher after the People’s Bank of China boosted liquidity in the financial system to support banks. Hong Kong also rose. Equities in Japan and Australia were lower along with European equity futures. S&P 500 contracts rose and crude oil climbed. Gold fell, building on last week’s slide. Treasuries were steady, with the 10-year yield at 0.70%.

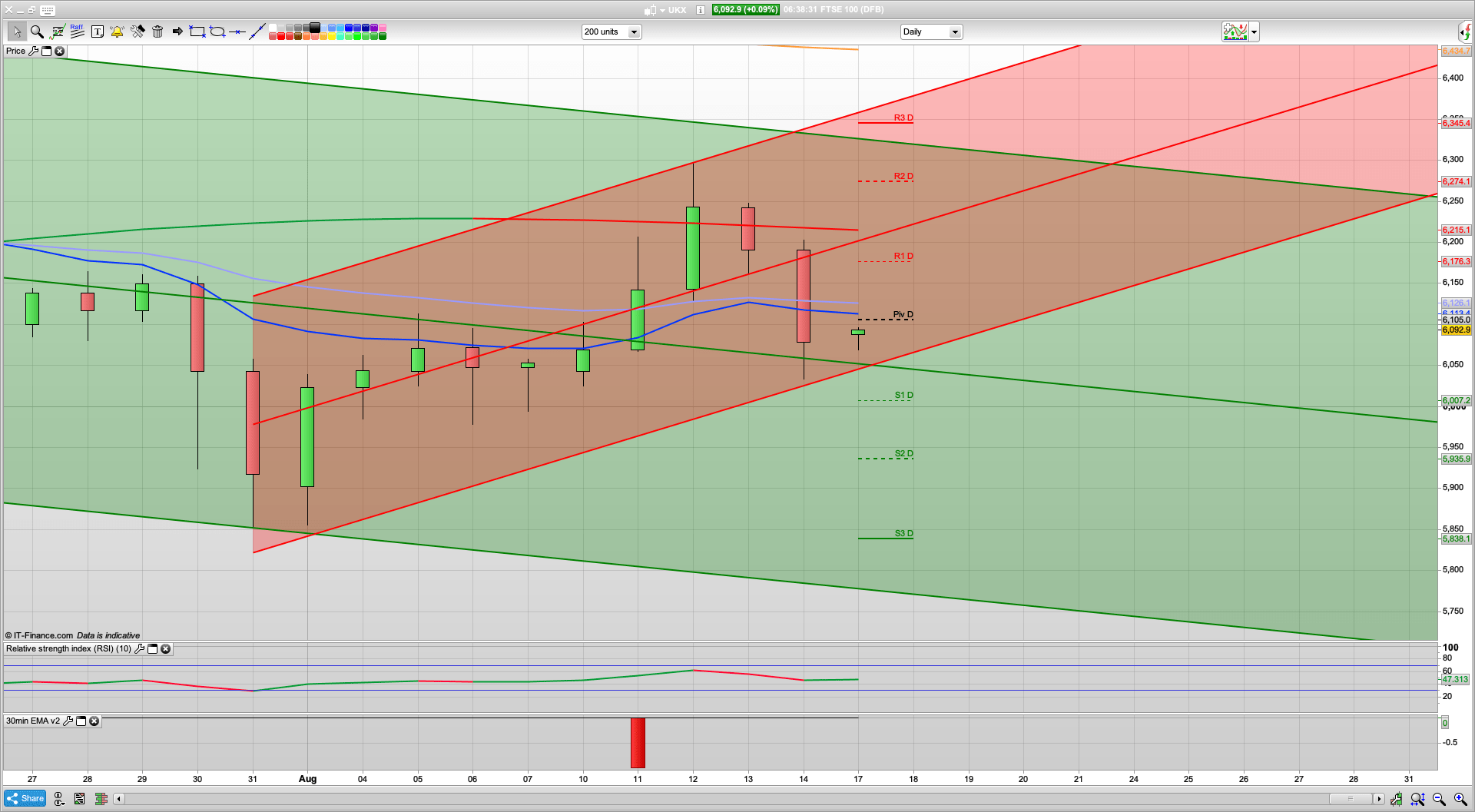

The bears took it a bit lower than the 6060 support level on Friday, getting down to the 6034 level before a decent bounce to the 6100 level, helped by the S&P bouncing off its fib at 3353. The S&P still needs to break above the 3385 level to test that 3399 resistance level, though an overshot towards the 3413 level may well play out. We have R3 there for today. The daily Raff channels on the S&P are still firmly up as it remains the strongest market, with 3500 distinctly possible before the year end!

For the FTSE the futures have held up well despite negative virus news from Australia and a ramping up of preventative measures in Italy. Measures there include mandatory face masks and closing of gathering places that had reopened. Measures that will be here in the next few weeks I expect. Looking at the charts we now have decent 2 hour resistance at 6190 and 6201 after Friday’s bearish session and as such should we get a rally to this area then a short here looks worth taking. The daily coral is red still and resistance from that at 6215 for today.

Looking at the Raff channels, we are not far off the bottom of the 10 day channel which is at 6045 for today, so a long here may well be worth a go again as per Friday. The bears will need to break 6060 again though as that may still hold as daily support initially. We also have the key fib level at 6050 today. Will we get a bull Monday and a bounce of any initial dip?

The bulls will be keen to break above 6100 and also the daily pivot at 6105, and that does open up a possible climb as far as 6200. There is however initial resistance at the 6137 level where we have the 200ema (30m) and also 6145 with a key fib here. As such we may see an initial stutter in this area on any bullishness today.

To start with the 30min chart is just on the cusp of going bullish as I write this and 6088 is support initially. Could be an interesting pre open to see if that holds, or we get the spike down. The ASX was fairly flat, despite news of a lot of C-19 deaths, and their deadliest day to date, with 25 fatalities in the state of Victoria. The nation’s second-most populous state, which has imposed a lockdown and nighttime curfew in its capital Melbourne, on Monday also reported 282 new cases in the past 24 hours, down from daily tallies in the 700s in late July.

So, looking at a possible rise towards 6200 today, with 6135-6145 as an area to also watch and possibly short from as well. Support wise 6060, then 6045 are the levels to watch. With a possible drop to S1 at 6007. The bulls will be keen to defend a drop that low and also defend the round number.

Recommended Broker

IC Markets – offers market leading pricing and trading conditions by providing clients with True ECN Connectivity; this allows you to trade on institutional grade liquidity from the world’s leading investment banks, hedge funds and dark pool liquidity execution venues. Highly recommended!

Membership and Live Trading

If you would like more detailed analysis for FTSE 100, DAX, Gold and S&P, including the trades that I am looking to take myself, then please join my active members community.

What you get

- Daily Analysis pre market open (sent around 7am each day) for FTSE, DAX, Gold and S&P.

- Daily email pre market includes my trading plan for the day including ORDER levels, with stops and targets/limits

- Telegram live trading room and webinar group membership for discussion and realtime trade updates

Keep up to date with new content, free sign up below

[yikes-mailchimp form=”4″]