Good morning. Well that was an interesting day; the market was spooked by the Scotland poll showing the Yes vote slightly ahead, with sterling taking a real bashing. If yesterdays action has done anything then it might have shown what might be, therefore there might be a desire to get the FTSE higher so that an effect from a Yes vote in 9 days has a lesser effect. Initially today I am looking at support at 6812 as another dip starts to make things look rather bearish, with 6770 below that.

Asia Overnight from Bloomberg

Asia-Pacific stocks fell a fourth day, with the benchmark index heading for a three-week low, after the Standard & Poor’s 500 Index retreated from a record and as consumer shares slipped.

The MSCI Asia Pacific Index (MXAP) slipped 0.3 percent to 147.84 as of 11:40 a.m. in Tokyo, heading for its lowest close since Aug. 14. The equity gauge rebounded 14 percent from a February low through yesterday amid signs the U.S. economy is strengthening and as China introduced stimulus. The S&P 500 Index retreated from an all-time high yesterday following a five-week rally.

“The market is taking its lead from the U.S.,” Daphne Roth, head of Asian equity research at ABN Amro Private Banking, which manages about $218 billion said by phone. “We’re seeing a temporary consolidation after the recent rally. Global economic growth is still on track. We’re still overweight on equities.”

New Zealand’s NZX 50 Index slipped 0.1 percent. The Jakarta Composite Index fell 0.2 percent, while the Philippine Stock Exchange Composite Index declined 0.5 percent. Taiwan’s Taiex index and Australia’s S&P/ASX 200 Index each rose 0.2 percent. The Shanghai Composite Index and Singapore’s Straits Times Index each added 0.1 percent. Markets in South Korea and Hong Kong are closed for a holiday.

Relative Value

The MSCI Asia Pacific Index traded at 13.7 times estimated earnings at the last close, compared with 16.7 for the Standard & Poor’s 500 Index and 15.5 for the Stoxx Europe 600 Index.

Futures on the S&P 500 fell 0.1 percent today. The U.S. equity benchmark gauge retreated 0.3 percent from an all-time high as declines in energy companies along with oil prices overshadowed a rally by Yahoo! Inc.

European Union governments abruptly put on hold for at least a “few days” new sanctions against Russia, allowing more time to assess the viability of a cease-fire in Ukraine without risking further trade retaliation by the Kremlin.

FTSE Outlook

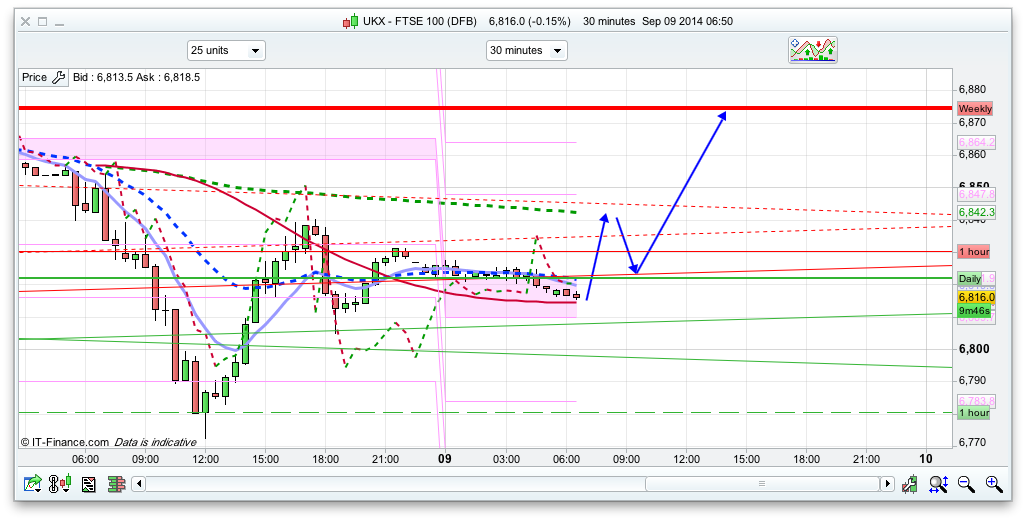

I wouldn’t be totally surprised if there was a rise over the next few sessions, to get the FTSE generating some positive headlines before the vote. Yesterdays action certainly caused a bit of worry with the Yes vote showing a lead in the polls, albeit only at 51%. Still neck and neck really. For today we have the daily pivot at 6822 so there is initial resistance there, but we have some initial support at 6812 – where we have the 30 minute coral line. Looking at the Raff chart then we have support below that at 6780 and a PRT support line at 6768 below that.

I have plotted a fairly bullish day, maybe surprising all things considered though. I can see an early rise to 6842 before some stutters there, but then a later rise to resistance at 6876. The proviso for this is that the 6812 area holds initially; if that breaks then 6770 looks likely. We are below the 10 and 20 day Bianca channels currently, and as mentioned above I wouldn’t be surprised if they engineer a rise to 6937ish.