Support 5746 5700 5713 5689 5677 5675 5583

Resistance 5788 5847 5895 5950 5997

Good morning.

Market Summary for Friday 12th February

After a week of big falls the FT100 managed to kick back up on Friday. The FT100 recorded its best one-day percentage gain in more than five months with banking and commodities sectors being the best performers, however they were also the ones most affected in the downturn. The main driver for the oil sector appeared to be comments from the energy minister of the United Arab Emirates on prospects for a coordinated production cut which sparked an oil prices rise of 10%. For banks it was positive results from Commerzbank which gave a lift to banks across Europe.

In after hours trading the FT100 moved up a shade more and consolidated around the 5730 level.

US & Asia Overnight from Bloomberg

U.S. index futures rallied as Japanese stocks soared the most since 2008 amid speculation a selloff that brought global equities into a bear market has gone too far.

Contracts on the Standard & Poor’s 500 Index due in March jumped 0.9 percent to 1,874.75 as of 1:45 p.m. in Tokyo. Japan’s Topix soared more than 7 percent, China’s yuan jumped by the most since a dollar peg ended in 2005, while the yen dropped with gold as haven assets fell out of favor.

“Japan is massively oversold,” said Andrew Clarke, Hong Kong-based director of trading at Mirabaud Asia Ltd. “Everyone is scrambling to get back in. Long-only investors are coming in along with retail and hedge funds. Plus, I would say there’s a lot of short covering going on. Also, U.S. shares rallied and we have China’s market back on today.”

Equities around the world are rallying after an MSCI gauge of global equities capped a 20 percent slide from a May record last week. The U.S. Federal Reserve acknowledged the volatility around the world and signaled it may delay further monetary tightening. China’s central bank stepped up efforts to restore stability to the nation’s currency and economy, with Governor Zhou Xiaochuan saying there’s no basis for continued yuan depreciation.

Japan’s Topix surged 7.3 percent, the most since October 2008, after a bigger-than-expected decline in fourth-quarter gross domestic product spurred speculation the central bank will boost stimulus. Financial markets in the U.S. and Canada are closed Monday for holidays.

The global rally started Friday with U.S. stocks halting a five-day decline, its longest losing streak since September, as crude prices rebounded and data showed retail sales increased for a third month in January. The S&P 500 rose 2 percent while the Stoxx Europe 600 jumped 2.9 percent. [Bloomberg]

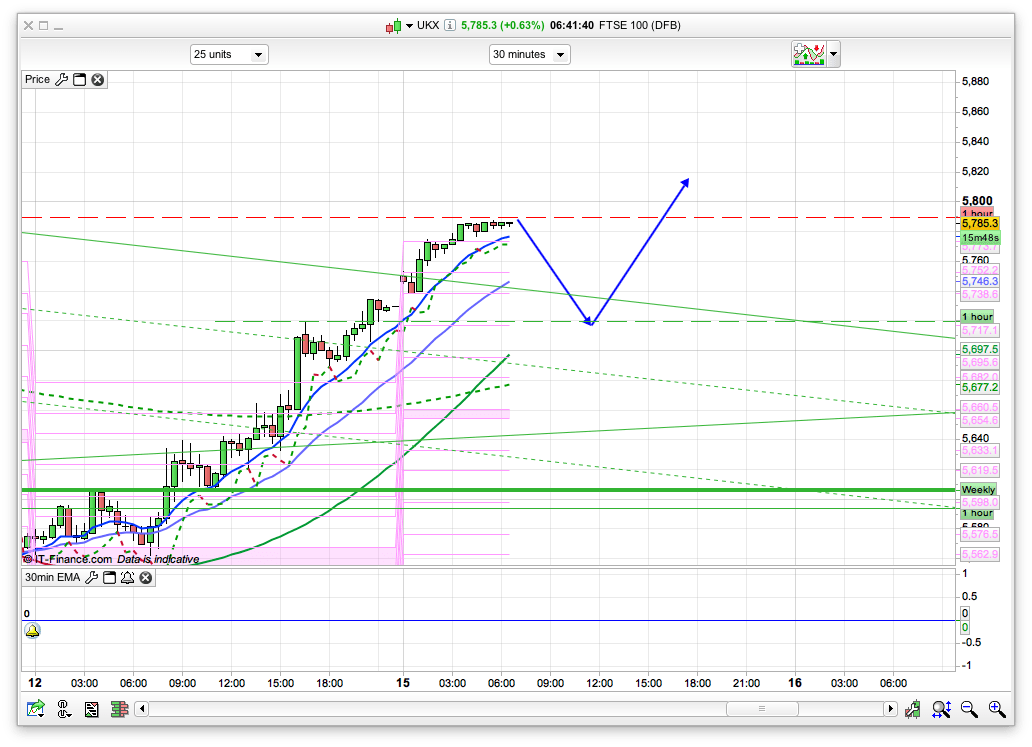

FTSE 100 Outlook and Prediction

We are sitting on the R1 level as I am writing this at 6am, and I think that we may well get an initial pullback towards the 5715 area to start with this morning. China is back today after their Lunar New Year break and things have remained fairly upbeat with Asian stocks rebounding from a three-year low, led by Japanese shares, amid speculation losses that pushed global equities into a bear market were excessive. As you know I had been looking at 5400 as the low for this leg down, but maybe 5500 is the bottom for the moment, and if this week remains upbeat then we could be on for some upside now. Maybe I was just a bit too bearish! For today, there is support at 5715 which is a backtest of a couple of daily channels , namely the Raff and Bianca, so if we do drop back then this area could well hold. The daily pivot is at 5675 below this for support there, not sure we will get a 100 point drop this morning though but you never know! Things might have bounced a little to far too fast off that 5500 level so a pull back would shake off a bit of the overbought conditions. The 2 hour chart has support at 5583 though I really don’t think we will see that level today. Above the R1 level of 5788 the next resistance level is 5848 for R2 then a major PRT at 5895. Generally feeling bullish at the moment.