Support 6152 6140 6130 6104 6093 6082 6076

Resistance 6182 6194 6225 6249 6251

Market Summary for Friday 4th March 2016

The FT100 was boosted by the market’s mining sector which climbed to a four-month high on Friday, boosted by a rally in the prices of major industrial metals.

The index also benefited at 1:30pm from a surge in U.S. non-farm payrolls, a sign of labour market strength that could further ease fears the economy might be heading into recession.

Both managed to push the FT100 to a close very near to the 6200 level with strong investment demand from 3:30pm into the close.

Commodities was the clear leading sector with interest rate sensitive sectors such as retail and house builders to the downside.

Trade wise, the early short at 6180 was a bust but the 6200 later in the day that was triggered by the NFP news ran nicely down for decent profit, before the bulls retraced that fall to hit a high at 6220. The S&P Long triggered at 1988 on the NFP news and rose well, to 2009 in the end. We have since fallen back a bit to 6170 this morning on the FTSE 100 though.

US & Asia Overnight from Bloomberg

- Copper, Aussie retreat as technical gauge points to declines

- Japanese equities fall with U.S., U.K. stock index futures

Asia’s emerging-market stocks and currencies advanced while oil rose above $36 a barrel after Friday’s U.S. jobs report brightened the outlook for global growth.

The MSCI Asia Pacific excluding Japan Index climbed to a two-month high, while Japan’s Topix and U.S. stock index futures declined for the first time in a week. Malaysia’s ringgit and Indonesia’s rupiah rose to their strongest levels since at least August. Australia’s currency and copper retreated as a technical indicator signaled recent rallies were excessive. Crude advanced to a two-month high in New York, after surging by about 10 percent in each of the last two weeks, while iron ore prices jumped in China.

The latest U.S. jobs figures added to a string of reports that have sketched out a picture of relative health in the world’s biggest economy, helping spur a rebound in global stocks and commodities that began in mid-February. China’s leaders set an expansion goal of 6.5 percent to 7 percent for 2016 at an on-going annual meeting of the legislature, down from last year’s target of around 7 percent, and said they are planning a record-high budget deficit.

“The U.S. recovery remains intact and we have not had a global recession without a U.S. recession in probably 100 years,” Matthew Sherwood, head of investment strategy at Perpetual Ltd. in Sydney, which manages about $21 billion, said in an e-mail to clients. “But I still think that despite the solid risk recovery over the past three weeks, returns are likely to be very modest in 2016, at best, and downside protection will be needed.”

China’s National People’s Congress continues on Monday, when data on the country’s foreign-currency reserves is due. A trade report out of Taiwan is scheduled, while India’s financial markets are closed.

Stocks

The MSCI Asia Pacific excluding Japan Index gained 0.5 percent as of 2:47 p.m. Tokyo time. The Shanghai Composite Index added 0.2 percent, while benchmarks in Malaysia, South Korea and Thailand were headed for their highest closes of the year. The Topix declined 0.9 percent, after surging 15 percent over the last three weeks.

“We’re at a level where we can easily get selling,” said Yoshinori Ogawa, senior strategist at Okasan Securities Co. “There are concerns over earnings, and I get the impression that moves to buy back happened in a state of wariness. Long-term funds probably haven’t come in yet.”

Australia’s S&P/ASX 200 Index gained 1 percent, climbing for the sixth day in a row. BHP Billiton Ltd., the world’s biggest miner, jumped 5 percent after surging 13 percent last week.

Standard & Poor’s 500 Index futures slipped 0.2 percent, while contracts on the U.K.’s FTSE 100 Index fell 0.4 percent.

Currencies

The ringgit gained as much as 1.1 percent to 4.0765 per dollar, the strongest level since August. The increase in crude prices is brightening prospects for Malaysia, Asia’s only major net oil exporter. The rupiah strengthened for a 13th day, its best winning streak since 2010.

The yuan fell 0.1 percent, snapping a four-day run of gains, as China’s leaders refrained from announcing specific support measures for the exchange rate at their biggest gathering of the year.The nation will push ahead with efforts to make the currency more convertible and promote its use overseas over the next five years, according to a development plan released at the National People’s Congress on Saturday.

Australia’s dollar fell 0.4 percent, after a 4.4 percent weekly surge that marked its best performance since 2011. The currency’s 14-day relative strength index was 70 at the end of last week, a threshold that indicates to some traders a reversal of direction is likely.

The Bloomberg Dollar Spot Index, a gauge of the currency against 10 major peers, was little changed after falling for a fifth day on Friday. Odds of the Federal Reserve raising interest rates by December ticked up after the payrolls data, with the probability at 68 percent, up from 53 percent a week ago and 49 percent a month ago, according to Fed funds futures tracked by Bloomberg.

Commodities

West Texas Intermediate crude climbed for the fifth time in six days, rising 1.8 percent to $36.57 a barrel in New York. It’s headed for the highest close since Jan. 4. Speculators reduced their short positions by the most in 10 months in the week ended March 1, CFTC data show.

Signs the Organization of Petroleum Exporting Countries will act to address the global surplus that has depressed prices for at least the past year is buoying oil, along with a decline in the number of active rigs in the U.S. The number of rigs has plunged 75 percent since September 2014 and ended last week at the lowest level since 1999, datashow.

“We’re starting to see U.S. production levels decline and if that continues, it could easily drive momentum in oil a bit further,” Ric Spooner, a chief analyst at CMC Markets in Sydney, said by phone. “Still, the higher prices go, the more vulnerable they are to some sort of correction, given we’re moving into a period of seasonal weakness.”

Copper fell 1.2 percent, after closing above $5,000 a ton last week for the first time in four months. It’s relative strength index was 76 on March 4, above the 70 level that indicates a likely change of direction. Investors in the metal shifted to a net-long position on March 1 for the first time in four months, weekly data show.

Iron ore futures jumped to their daily limit of 407 yuan ($62.47) a metric ton on the Dalian Commodity Exchange, up 4.9 percent and the highest level in almost six months. Steel in China also rose by the daily limit, with steel reinforcement bars for May up 5 percent to 2,073 yuan a ton on the Shanghai Futures Exchange.

The Bloomberg Commodity Index rose 0.1 percent, after a 3.9 percent gain last week that marked its biggest advance since July 2012.

Bonds

Australian bonds led declines among sovereign debt, with yields on notes due in a decade climbing three basis points to 2.58 percent. The rate on similar-maturity U.S. Treasuries increased by one basis point to 1.89 percent, after adding four basis points on Friday.

The cost of insuring Asian corporate and sovereign debt fell to a two-month low, with the Markit iTraxx Asia index of credit-default swaps retreating one basis point to 146 basis points, according to prices from Australia & New Zealand Banking Group Ltd. [Bloomberg]

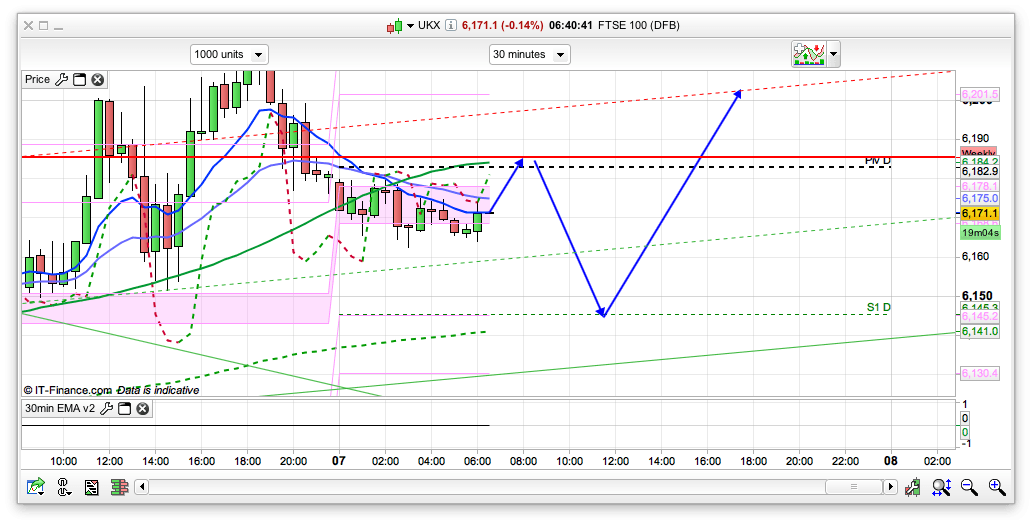

FTSE 100 Outlook and Prediction

Mondays recently have been fairly optimistic and looking at the 30min chart there is decent support around the 6130/6140 area. NFP on Friday came in better than expected and the market wasn’t sure how to react really, hence the drop then rally. Raises prospects of rate rises, despite words that they aren’t coming in the short term. For today the pivot is 6182 and we have a bearish 30min chart to start with. As such I am expecting a dip from the pivot area to test the 6145 area and then if we repeat the usual Monday bull pattern, a rise from there to maybe test 6200, and possibly Fridays high at 6220. However, I am wary about getting too bullish as I still think we have come too far too fast and think we should have a pull back towards 5700. That said, the 2 hour chart has gone bearish despite that rise on Friday and is showing resistance at 6194. So for today I am thinking that a dip from the pivot area, down to the 6145 support area before another rise to test 6194, possibly 6220. I am favouring the bearish side for this week though.