FTSE 100 Support 6988 6980 6974 6969 6948 6931 6880

FTSE 100 Resistance 7033 7056 7111 7131

Good morning. Well there was 7000 then, but the Dow couldn’t quite reach 20000 for the double whammy. Our early short from the 6964 level saw a bit of a dip down to 6942 but the bulls fought back, determined to reach 7k. Gold continued to slip further testing 1124 – wouldn’t be surprised if we are nearing a low on that soon. It looking quite strong to hold above 7000 as we head towards Christmas, however I am looking at buying a dip today around the 6974 level. We have support on the 2 hour chart here, and Australia (ASX200) followed a similar dip and rise pattern.

US & Asia Overnight from Bloomberg

The dollar is cementing its domination of the currency market, trading near an almost 14-year high versus the euro as the Federal Reserve’s more hawkish outlook invigorates its post-election rally. Asian stocks advanced.

The greenback headed for its best week in a month against major peers after surging to its strongest point since 2003 versus the euro and to a 10-month high against the yen. The Japanese currency’s losses helped the Topix index extend gains at its highest this year while Chinese stocks and the yuan halted declines. Yields on Japanese debt due in a decade touched the highest level since January after the Fed’s only interest-rate hike of 2016 came with a boost to the number of increases expected next year. Oil edged higher.

The Fed’s pivot toward hawkishness marks a shift away from central-bank policy dominating market sentiment, with the potential for an increase in fiscal stimulus now in focus. While stocks have rallied and debt has tumbled since Donald Trump’s election as U.S. president fueled bets on an uptick in spending, the Fed stands largely alone in actively tightening policy, fueling the dollar’s surge. The Bank of England kept its key rate at a record low Thursday, a week after the European Central Bank extended quantitative easing.

“It’s all about the dollar at the moment,” said Cameron Bagrie, chief economist in Wellington at ANZ Bank New Zealand Ltd. “The U.S. economy is growing and the labor market is improving so monetary normalization is a good thing and markets have responded as such.”

Stocks

The MSCI Asia Pacific Index added 0.3 percent as of 12:35 p.m. Singapore time, reducing its decline in the week to 1.4 percent, still the worst weekly performance since October.

The Topix gained 0.3 percent, bringing its sixth straight weekly advance to 1.4 percent and erasing its loss for 2016.

China’s Shanghai Composite Index was little changed, halting two days of declines.

New Zealand’s S&P/NZX 50 Index added 0.2 percent, snapping a five-day retreat and trimming its weekly decline to 1.9 percent.

U.S. index futures were little changed.

The S&P 500 Index ended last session up 0.4 percent after sinking the most since October after the Fed’s statement on Wednesday.

Currencies

The dollar lost 0.2 percent to $1.0435 per euro, after climbing to as high as $1.0367 Thursday, its strongest level since January 2003.

The yen was steady at 118.12 yen per dollar, set for a slump in the week of 2.4 percent, it’s sixth straight weekly drop. The yen is the worst-performing major currency against the dollar this week.

The Korean won fell for a third day, losing 0.5 percent.

“At the moment it feels like going long dollar is free money, no one loses,” said Stuart Bennett, head of Group-of-10 currency strategy at Banco Santander SA in London.

Bonds

Rates on Japanese bonds due in a decade advanced as much as 1 1/2 basis points to 0.10 percent. The benchmark’s yields gave up the earlier increase to trade at 0.09 percent.

Yields on Treasury notes due in a decade were little changed at 2.58 percent, set for their steepest weekly advance in a month after touching their highest level since September 2014.

New Zealand debt extended losses, pushing yields up 3 basis points to 3.43 percent.

Commodities

West Texas Intermediate crude rose for the first time in three days, adding 0.6 percent to $51.22 a barrel, still on track for its second straight weekly retreat.

Gold for immediate delivery edged up 0.1 percent to $1,130.05 an ounce, set for a weekly decline of 2.6 percent, its worst week in a month.

[Bloomberg]

FTSE 100 Outlook and Prediction

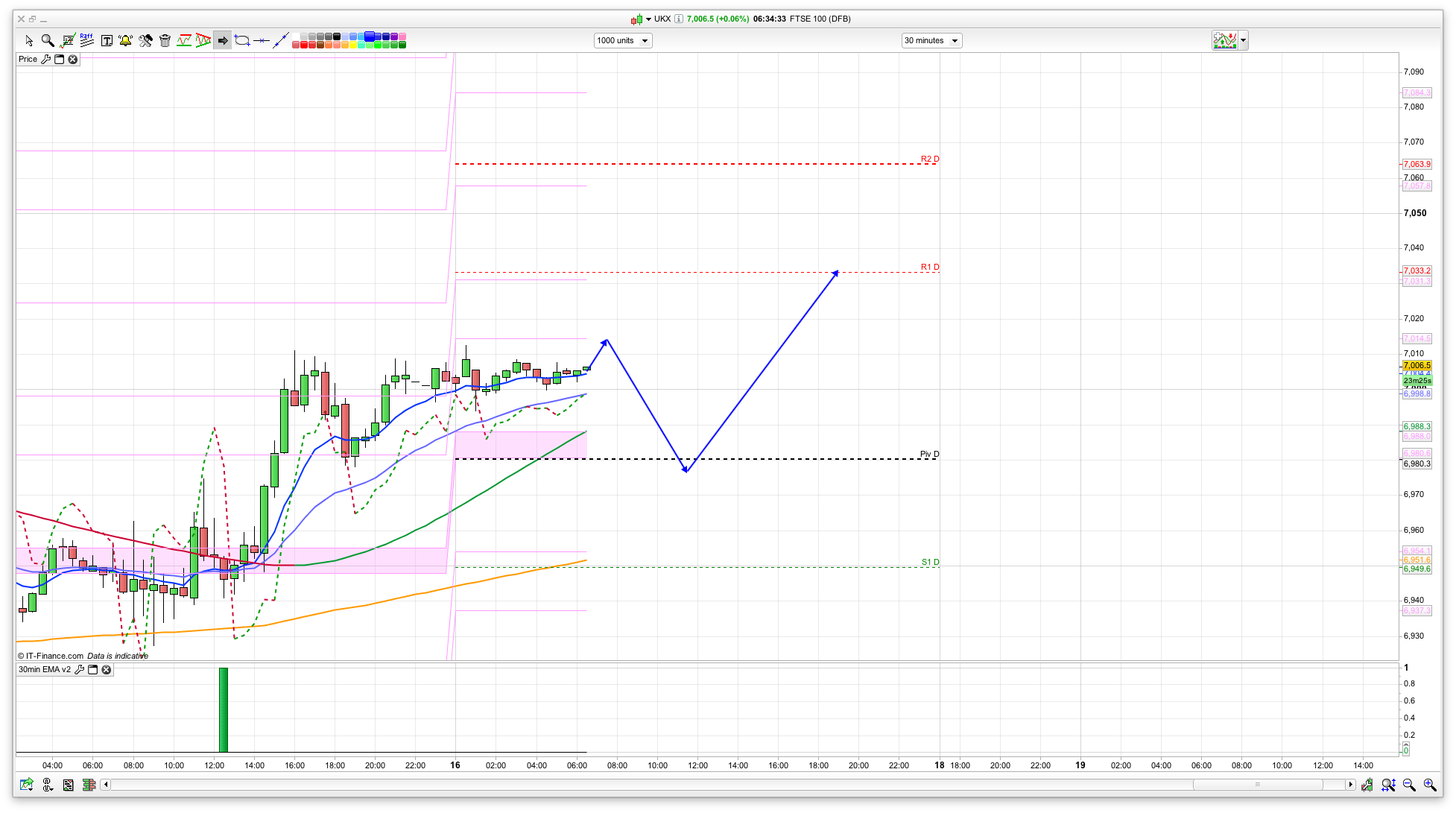

For today I am thinking a dip and rise day. If we are going to get a bit more out of this Santa Rally (or start a new one!) then next week is the last week for the bulls, and looking at the 2 hour chart we now have support at 6975. There are a few other support levels around this area with 6980 as the daily pivot, a green coral on the 30min at 6988 and the 2 hour coral as 6969. Below this 6950 is the 200ema on the 30min and lower still on the daily chart we still have the 25ema at 6880 waiting to be tested – usually holds on the first touch after a trend change so am watching that for a long entry (more of a swing trade here).

We have triple witching option expiry today as well, so will see some choppiness at 10:10am. Bear that in mind – likely to spike up then drop back as all the futures contracts roll over.

Resistance wise, we have 7033 for R1, then the top of the 20 day Bianca at 7056. It will all depend on the bulls holding that 6975 and if they can manage to keep things above 7000. Its the end of the week after a fairly strong run from that 6860 level support we had earlier this week so they may be tempted to take some profit with FTSE at this psychological level, and Dow Jones nearly at 20000. On the other hand, they wont want to miss a possible final push next week as Santa rolls into town. As such, I am going to keep it fairly simple today and look to go long around that 6975 level and see how it goes from there.

I have just posted my 2017 Outlook as well. You can read it here

Is 6974 still likely this afternoon? Thanks for the 10.10am tip.

Holding up well above 7000 at the moment. If the bears break 7004 on this dip back then still possible. Support has risen a bit now to 6982