FTSE 100 Support 6691 6682 6722 6673 6599 6513

FTSE 100 Resistance 6710 6715 6724 6730 6800

Good morning. The long worked well yesterday for that second leg up from 6693 to 6730. Dropped back overnight ahead of the ECB today, who are largely expected to keep things as they are, whilst some are predicting further easing later this year. Heads up for that at 12:45.

US & Asia Overnight from Bloomberg

- Euro gains before ECB policy review as yuan strengthens

- Malaysian stocks, ringgit slide as 1MDB fraud probe heats up

Asian equities rose to this year’s high, while the yen and New Zealand’s dollar hit six-week lows amid signs regional policy makers are preparing to step up stimulus. Stocks are also finding support as U.S. corporate earnings prove more resilient than analysts anticipated.

The MSCI Asia Pacific Index surpassed its April peak as Hong Kong’s benchmark erased its loss for the year. The Topix index gained after Japan was reported to be considering a 20 trillion yen ($187 billion) stimulus program. The kiwi fell versus major peers after New Zealand’s central bank said interest rates are likely to be cut, while the euro rose before the European Central Bank reviews policy. Malaysia’s stocks and currency were Asia’s worst performers as alleged fraud at a state investment fund returned to the spotlight.

The quarterly earnings season is giving fresh impetus to a global equities rally that’s added almost $5 trillion to stock values since the post-Brexit low on June 27. So far, about four in five of S&P 500 Index members that have reported results beat analysts’ profit estimates. While the ECB is seen leaving policy unchanged on Thursday, most economists predict further easing this year. Indonesia’s central bank is forecast to lower interest rates, following cuts in Malaysia and Turkey since the start of last week.

“We have better corporate earnings, likely bold fiscal stimulus in Japan, zero interest rates helping to absorb every macro shock we hear about and broad monetary easing,” said Chris Weston, chief market strategist at IG Ltd. in Melbourne. “If equity markets can’t rally in this environment they never will and really the key concern holding back fresh capital is significantly elevated valuations.”

AT&T Inc., General Motors Co. and Visa Inc. are among U.S. companies set to release results on Thursday, while Europe’s lineup includes Daimler AG and Unilever Plc. American home-sales data and U.K. retail sales figures are also scheduled.

Stocks

The MSCI Asia Pacific Index rose 0.2 percent as of 2:15 p.m. Tokyo time. Hong Kong’s Hang Seng Index was set to enter a bull market, having rebounded more than 20 percent from a February low.

The Topix climbed 0.2 percent, led by gains in exporters amid the yen’s retreat. The Japanese government is considering a 20 trillion yen stimulus package, about double its initial plan, to counter the possible effects of the U.K.’s decision to leave the European Union, Kyodo News reported, citing people close to the matter.

The FTSE Bursa Malaysia KLCI Index dropped 0.4 percent. U.S. prosecutors said they plan to seize assets after more than $3.5 billion was misappropriated from 1Malaysia Development Berhad, a state development fund known as 1MDB that was previously headed by Prime Minister Najib Razak. Singapore said it seized S$240 million ($177 million) in assets linked to the alleged fraud.

S&P 500 Index futures were little changed, after the gauge closed at a record high. Better-than-expected earnings from Volkswagen AG and software maker SAP SE helped lift the Stoxx Europe 600 Index to a four-week high in the last session.

Currencies

The yen fell as much as 0.6 percent versus the dollar, before recouping almost all of its loss. The kiwi dropped 0.6 percent after the Reserve Bank of New Zealand said further monetary easing is likely to be required to lift inflation, reinforcing expectations interest rates will be cut next month.

“The yen should continue to ratchet lower against the dollar into next Friday’s Bank of Japan meeting,” said Sean Callow, a senior foreign-exchange strategist at Westpac Banking Corp. in Sydney. “As for the kiwi, an August rate cut is effectively a done deal.”

The Bloomberg Dollar Spot Index held near to its highest close since May. A Citigroup gauge that tracks the degree to which American economic data are exceeding projections is at an 18-month high and futures put the chance of a Federal Reserve interest-rate increase this year at 47 percent, up from 9 percent at the end of June.

Malaysia’s ringgit slumped 0.7 percent amid the 1MDB controversy. Indonesia’s rupiah traded near a one-week low as economists forecast the central bank will reduce its benchmark interest rate by a quarter of a percentage point for the fifth time this year. The yuan rose for a third day, its longest winning streak in three months, after the People’s Bank of China strengthened its daily fixing in a show of support for the currency before Group of 20 finance chiefs meet for talks in China this weekend. Turkey’s lira rose 0.5 percent, after plunging to a record low on Wednesday. S&P Global Ratings downgraded the country’s debt on concern about an increase in political risk after a failed coup last week and the government declared a state of emergency as it pursues those responsible.

Commodities

Oil for September delivery rose 0.4 percent in New York, advancing toward $46 a barrel after weekly U.S. government data showed crude stockpiles fell for a record ninth week and refining activity climbed to a 2016 high.

Gold held near this month’s low as the global equities rally damped demand for haven assets amid a period of dollar strength. Copper rose 0.3 percent in London, nearing its highest close since April, and zinc traded near a 14-month high.

Bonds

U.S. Treasuries due in a decade were little changed, yielding 1.57 percent. The yield sank to a record 1.32 percent on July 6 and analysts see it ending the year at 1.74 percent, a Bloomberg survey shows.

Yields on similar-maturity sovereign debt in Japan and Australia were little changed, while New Zealand’s declined three basis points to a two-week low of 2.26 percent. Swaps traders are pricing in a 90 percent chance the RBNZ will cut its interest rate from a record low next month, up from 64 percent a week ago. [Bloomberg]

FTSE 100 Outlook and Prediction

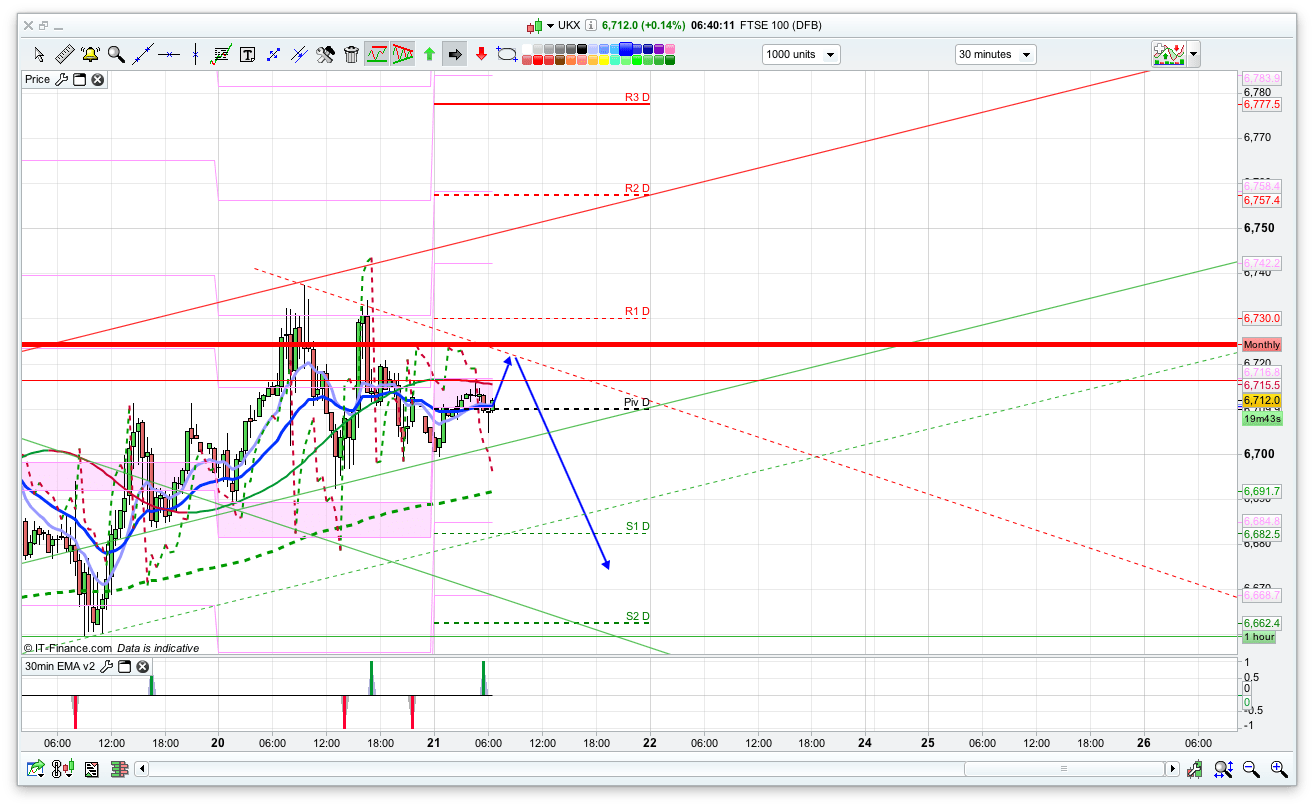

We have the ECB today at 12:45 so expect some movement around then, even though expectations are for no changes. For today I have put in an initial little move up to 6720 then a decline down to the bottom of the 10 day Bianca channel at 6673. We might end some support here, but looking at the 30min and 2 hour chart it feel like after yesterdays failure to really break 6730 that we might be on for a decline today. The 2 hour chart is still bullish at the moment but might well change to bearish if we have a flat to weak morning – the key level will be a hold below 6710 which will set that up to confirmed bear. So, fairly simple plan for today really – short at 6720, and long at 6674 off the 10 day channel. If the bears break the latter then we could be on for further downside, but at the moment the bulls seem to be piling in on any dips.

Well Done Nick!! Spot on !! Morning short @ 22 closed @ 97 curretnly long from 700.. might be looking to get out if that soon .. expect some bigmove today

out @10

Not trading today as it looks too volatile.

Can’t decide if a big drop is coming or a big rise!

its v tricky – trading within a 20 pt range for last few hours… and even tighter for most of it…

Unchanged it is !! But what would it mean in coming days ?

What’s the chart looking like Nick? Doesn’t seem to want to break 6700…

Still bullish?

It’s not letting me post !! But never mind shorted @30 will try to hold till bells

I wonder people who were short from 300-400level how they are doing now?

I was short at 500 and had to take a hit…

Knock knock !! Nobody here??

I’m here!!

Afternoon chaps….been lurking but nothing much to post…..didn’t close any trades yday….missed my chance twice!….wasn’t on top of my game…anyway held overnight and sold first thing……that was weds target met…..this morning…..and I’ve hit my target for today already….been a good consistant week pleased….presently long from 90…..good luck chaps….

Hey anstel stay lurking might get overnight drop

Long at 82 as well……never know :0)

Looking good so far :0)

Let’s get some momentum going :0)

Out all at 91.5 :0) goodnight all…

Hello All

I am new here and testing..

Hi rdl, welcome!