Good morning. Friday was quite a wild day on the FT100 with follow through selling from the ECB news on Thursday then positive news from the US jobs data. However miners and oil stocks reversed gains following a statement by OPEC members saying they had failed to agree an oil production ceiling. I believe there was also a fair bit of “stop hunting” by the markets with some platforms going sub 6200 for a few minutes on Thursday evening. “Spiking” prices/indices seems to be the order of the day now so that is why it can be good to setup ‘orders to open’ and close on ‘limits’ and play them at their own game! The U.S. non-farm payrolls data signalled that a rate rise in the U.S. was on the cards for December, however this is already built into market prices now. Sector wise the main fallers were oils and miners with house builders the best sector on the back of a positive statement from Berkeley Group.

US & Asia Overnight from Bloomberg

Asian stocks rose after a U.S. employment report boosted optimism in the world’s largest economy, with Japanese shares climbing as a weaker yen sent exporters higher.

The MSCI Asia Pacific Index advanced 0.4 percent to 132.62 as of 9:00 a.m. in Tokyo. The Standard & Poor’s 500 Index rose the most in almost three months on Friday, while the yen weakened 0.4 percent against the dollar after the bigger-than-expected increase in American nonfarm payrolls. Japan’s Topix index added 0.9 percent on Monday. The data supports the case for the Federal Reserve lifting interest rates next week, according to Shane Oliver, head of investment strategy in Sydney at AMP Capital Investors Ltd., which oversees about $115 billion.

“Providing the Fed undertakes a dovish hike as we expect, in stressing that future moves will be gradual, then confidence is likely to return,” he said. “The Fed is unlikely to do anything to threaten global growth.”

South Korea’s Kospi index rose 0.7 percent. Australia’s S&P/ASX 200 Index added 1.2 percent and New Zealand’s S&P/NZX 50 Index advanced 0.2 percent.

Friday’s report showed a 211,000 increase in November U.S. payrolls, following a 298,000 gain a month earlier that was bigger than previously estimated. The jobless rate held at 5 percent, a more than seven-year low. A healthy rate of hiring has raised the odds that Fed officials will boost rates this month for the first time since 2006. The pace of future increases is contingent on progress toward the central bank’s inflation goal and probably depends on how quickly wage pressures mount as the job market tightens.

Draghi Comments

Meanwhile, European Central Bank chief Mario Draghi tried to soothe investors disappointed by his move on economic support last week, signaling on Friday that the bank will add stimulus as needed.

Futures on the S&P 500 were little changed. The underlying equity measure jumped 2.1 percent on Friday, its strongest gain since Sept. 8, with the gauge posting its ninth weekly advance in the last 10. A measure of volatility plunged the most in two years.

Futures on the Hang Seng Index added 0.5 percent in most recent trading, while contracts on the FTSE China A50 Index gained 0.8 percent. The Shanghai Composite Index lost 1.7 percent on Friday, paring its weekly advance to 2.6 percent, as speculation of increased monetary stimulus faded and investors prepared for the first initial public offerings in five months.

Energy shares retreated in Asia on Monday as oil traded below $40 a barrel after OPEC tossed aside the idea of limiting production to control prices at a meeting in Vienna on Friday. The Organization of Petroleum Exporting Countries said it will keep pumping as much as it does now — about 31.5 million barrels a day — effectively endorsing limitless output. [Bloomberg]

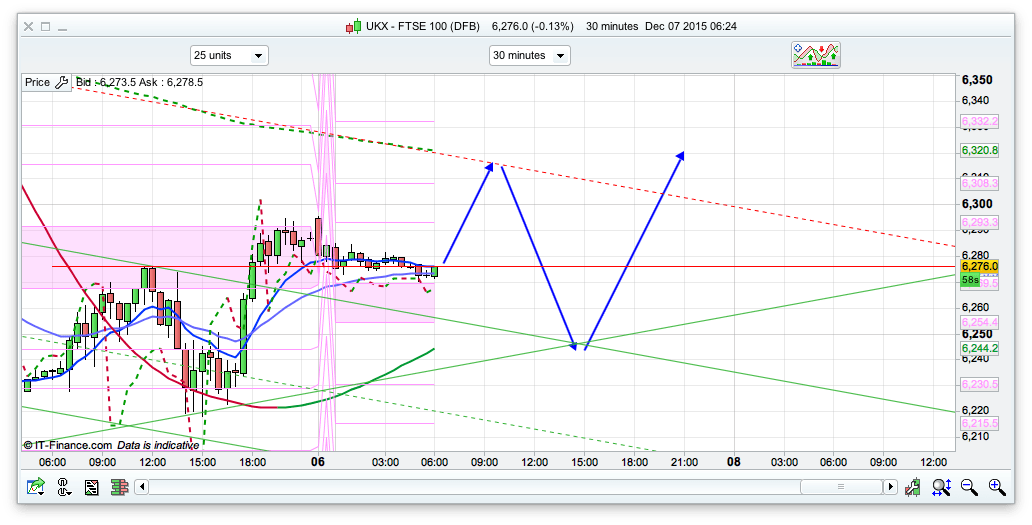

FTSE Outlook and Prediction

We have the daily pivot for initial support at the 6366 level for today (live charts one slightly lower at 6345 though) and also more favourably the 2 Bianca channels at 6230 and 6215. As such I think we are going to have a slightly bullish day today and probably test the 6315 area, where we have the top of the declining 30min channel and also the 200ema on the 30min chart. Additionally we have the daily EMAs (10 and 25) here so this level could act as fairly decent resistance. We have had a decent bounce and held the gains from the 6200 level so its distinctly possible that that will be the December low. However, a break of 6200 today will likely see the bottom of the 30min channel at 6183, though I feel more bullish than that for today.