Support 6000 5960 5947 5910 5898

Resistance 6006 6018 6026 6048 6130

Good morning.

Market Summary for Monday 22nd February

The FT100 looked initially like having a negative open as the overnight IG price fell below 5900 only to rise significantly after positive commodity price movements and Far East trading.

The good news outweighed the bad news of the UK referendum which had unsettled markets as it appears it will be far tighter than predicted.

The UK Pound fell by around 2% at one point which helped internationals but domestic companies suffered. A weaker pound also put pressure on property shares as it would indicate an upward chance of interest rises and also foreign investors don’t want to invest in property in a country which may exit.

All this resulted in commodities being the strongest sector and property the weakest.

The overall trend was quite positive moving up steadily for most of the day closing at 6037

US & Asia Overnight from Bloomberg

A global equity rally stumbled as most Asian gauges slipped, while U.S. index futures dropped. Crude slumped, the yuan weakened and the yen climbed.

Benchmark equity indexes in Japan, China and South Korea turned lower, while contracts on the Standard & Poor’s 500 Index slid 0.4 percent. Japan’s currency appreciated against all 16 major peers and Treasuries rallied. The yuan declined after the People’s Bank of China lowered its daily reference rate by the most in six weeks. New York oil dropped after surging above $33 a barrel on Monday, while nickel and zinc led industrial metals lower.

The first indicators for Asia’s biggest economy this month showed private gauges of manufacturing and services falling to new lows, while a reading of business confidence slipped. The impact of China’s slowdown and the commodity-price collapse was in focus Tuesday as BHP Billiton Ltd. made a larger-than-expected cut to its dividend, lowering the payout for the first time in 15 years, while Noble Group Ltd. blamed the tumble in coal prices for an additional $1.2 billion in charges.

“If there’s something dramatic in the Chinese market, then normally people buy U.S. Treasuries,” said Toshifumi Sugimoto, chief investment officer at Capital Asset Management in Tokyo. “The Chinese economy is not doing well.”

Stocks

The MSCI Asia Pacific Index dropped 0.1 percent at 1:02 p.m. in Hong Kong, falling from its highest level since Feb. 8. The Shanghai Composite Index retreated 1.3 percent. The Topix index lost 0.3 percent in Tokyo, while Australia’s S&P/ASX 200 Index slid 0.6 percent. The Kospi index declined 0.3 percent in Seoul.

BHP added 2.7 percent in Sydney, paring its 12-month drop to 41 percent. Underlying profit fell to $412 million at its continuing operations in the six months to Dec. 31, from $4.9 billion a year earlier, the world’s biggest mining company said Tuesday in a statement. Noble Group was little changed in Singapore after saying the impairments will force the embattled commodities trader to post its first full-year loss in almost two decades.

Bonds

Treasuries rallied, pushing the yield on the 10-year benchmark note down three basis points to 1.72 percent. Rates on similar-maturity Australian bonds slid four basis points to 2.42 percent.

Currencies

The yuan fell 0.09 percent to 6.5284 a dollar, according to China Foreign Exchange Trade System prices. The People’s Bank of China lowered the daily reference rate for the yuan by 0.17 percent, the most in six weeks. The fix was lower than most models were expecting, said Sue Trinh, the head of Asia foreign-exchange strategy at Royal Bank of Canada.

“It seems to be a direct policy signal to weaken the yuan, at least for today, and that is seeing dollar-yen leading the way lower and cross-yen selling off as well,” Hong Kong-based Trinh said. “If today’s fix is the start of a trend, then it would be consistent with our view that China needs a more flexible exchange rate and, in other words, a weaker exchange rate.”

The yen gained 0.5 percent to 112.34 per dollar, rallying from a decline Monday. Options traders are close to the most bullish on the yen since 2011, pricing on six-month contracts show.

Commodities

Oil traded near $33 a barrel as the International Energy Agency said a global surplus will persist into next year and limit any chance of a short-term price rebound. April futures in New York slid as much as 1.7 percent after the March contract expired Monday up 6.2 percent. While supply and demand will be aligned next year, large accumulated stockpiles will slow the pace of recovery in prices, the IEA said in its medium-term report.

Nickel retreated from the highest close this year, with the metal used in stainless steel falling 1.3 percent to $8,660 a metric ton. Copper dropped 1.3 percent and zinc declined 1.2 percent. [Bloomberg]

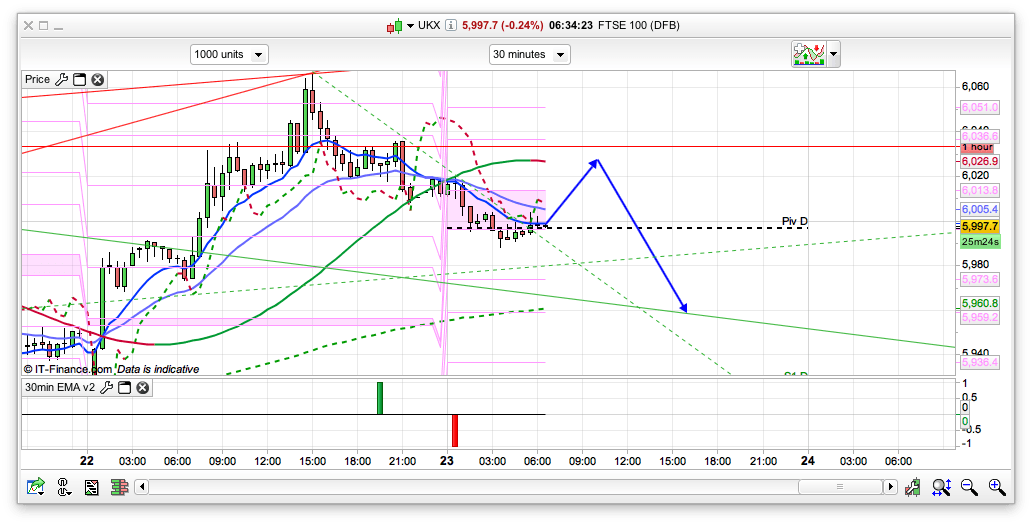

FTSE 100 Outlook and Prediction

We moved a little bit higher than the 6045 resistance area I had for yesterday but the bears managed to fight back and we have dropped off again overnight, and also are just sticking the nose below 6000 as I write this. The 2 hour chart is still bearish, whilst the daily is just crossing to bull, with support at 5898, and as I mentioned yesterday I do think we will get a pull back after the rise from 5500 before we push too much higher – we rose a bit too far too fast in the past 10 days, and on nothing really. For today the 30min has gone bearish with resistance at 6006 and then 6026 just above that – a level that I feel would be a good entry for a short for a dip to the 200ema on the 30min at 5960. There is a chance that we will dip further however, I think that would be decent support if seen today as we have some PRT supports here also. Psychologically, 5950 is likely to be a decent level for the bulls to have a go at 6000 from also, as well as the 10 day Bianca at 5947. That said, if it breaks then 5898 is pretty likely. So, for today, weak bull to start with but favouring a bit of a pull back, ideally from 6025.