Support 6049 6042 6030 6029 5943 5932

Resistance 6068 6072 6103 6194

Market Summary for 29th February 2016

Both the shorts worked well to give a decent end to February, with he first short taking on the spike with the Chinese rate cut news.

European data got the markets off to a negative start but then moved higher after China said it would resume its easing cycle (meaining banks could reduce their margins held against loans).

The FT100 spiked down below 6050 in the morning but regained that level after the China news fed through.

On the Wall Street open shares rallied further taking the FT100 to the 6100 area at the close.

This appears to be a level of high resistance so there is still a good chance of a fallback to below 6000 in the coming days, especially with possible Brexit unsettling some investors.

US & Asia Overnight from Bloomberg

- Chinese lenders’ reserve ratios cut amid deepening slowdown

- Crude trades near seven-week high; ringgit strengthens

Asian stocks rallied and emerging-market currencies strengthened as monetary stimulus in China brightened prospects for the world’s second-largest economy. Crude oil traded near a seven-week high, while copper led declines among industrial metals.

Benchmark share indexes advanced across most of Asia after the People’s Bank of China cut lenders’ reserve requirements, helping lower borrowing costs in the nation. The yuan gained for the first time in eight days and the pickup in oil prices buoyed Malaysia’s ringgit. Copper retreated and gold rose after a gauge of Chinese manufacturing declined, matching its lowest level of the past seven years.

While February marked a fourth consecutive monthly decline in global stocks, a benchmark equities index rallied more than 5 percent since Feb. 11. Mounting signs that American consumers can still power the world’s largest economy and hints from central banks in Asia and Europe that more stimulus is at the ready underpinned the revival, along with crude’s rebound from a 12-year low reached last month.

“Market sentiment is on its way toward a recovery, but the slightest bad news can still rock it,” said Toshihiko Matsuno, chief strategist at SMBC Friend Securities Co. in Tokyo.

The cut in Chinese lenders’ reserve requirements is the first in four months and comes after Asia’s biggest economy expanded last year at the slowest pace in a quarter century. The nation’s parliament will gather on Saturday for an annual meeting, where plans for 2016 and the next five years will be outlined.

Stocks

The MSCI Asia Pacific Index rose 0.5 percent as of 2:44 p.m. Tokyo time, headed for its biggest gain in a week. Hong Kong’s Hang Seng Index added 0.3 percent, while benchmarks in Australia and Taiwan rallied 0.9 percent. The Shanghai Composite Index gained 0.2 percent, though is still down 24 percent for the year.

China’s $5.3 trillion stock market will rebound as much as 20 percent in the “short term” as economic growth picks up and yuan volatility decreases, according to Lirong Xu, chief investment officer at Franklin Templeton’s money-management unit in Shanghai. That view was echoed by Gao Ting, head of China strategy at UBS Securities Co. in Shanghai, who said sentiment is “overly pessimistic” and there’s a growing chance of a rally within the next three months as the central bank loosens monetary policy.

Standard & Poor’s 500 Index futures slipped 0.2 percent after the U.S. benchmark retreated 0.8 percent on Monday, capping a monthly loss.

Currencies

The yuan strengthened 0.2 percent versus the dollar as the People’s Bank of China raised its daily reference rate for the first time in a week. An official manufacturing purchasing managers index dropped to 49 in February, missing the median estimate of 49.4 in a Bloomberg News survey of economists. It hasn’t been weaker since January 2009.

“With a stronger fixing, they’re trying to ensure a stable yuan even as they ease policy through the reserve-requirement-ratio channel,” said Khoon Goh, a foreign-exchange strategist at Australia & New Zealand Banking Group Ltd. in Singapore. “There’s potential for further RRR cuts, given that today’s PMI data was weak.”

Malaysia’s ringgit strengthened 0.3 percent versus the dollar, climbing for a fourth day as the rebound in crude prices brightens prospects for Asia’s only major net oil exporter. The Australian dollar fell 0.2 percent after central bank kept its benchmark interest rate at a record-low 2 percent at a Tuesday policy meeting — a decision forecast by all of the economists in a Bloomberg survey — and said low inflation offers scope for easing.

Bonds

Money-market rates declined in China as the cut in lenders’ reserve requirements freed up funds. The one-day repurchase rate, a gauge of interbank funding availability, dropped four basis points to 1.94 percent in Shanghai, while the seven-day rate was seven basis points lower at 2.27 percent.

U.S. Treasuries advanced, pushing the 10-year yield down by two basis points to 1.71 percent. The securities have returned 3 percent in the first two months of this year, their biggest back-to-back gain January 2015, according to the Bloomberg World Bond Indexes.

Commodities

Crude futures rose 0.2 percent to $33.83 a barrel in New York, after gaining 3 percent Monday to record the highest settlement price in seven weeks.

Copper, nickel and zinc all fell at least 0.9 percent on the London Metal Exchange, dragged lower by the deterioration in China’s manufacturing. Gold climbed 0.4 percent, building on an 11 percent jump in February that marked its biggest monthly increase since January 2012.

“Chinese growth concerns have boosted the safe-haven appeal of gold,” said Bernard Aw, a strategist at IG Asia Pte in Singapore. Gains may be capped on Tuesday by the “short-term boost to risk appetite from China’s easing,” he said. [Bloomberg]

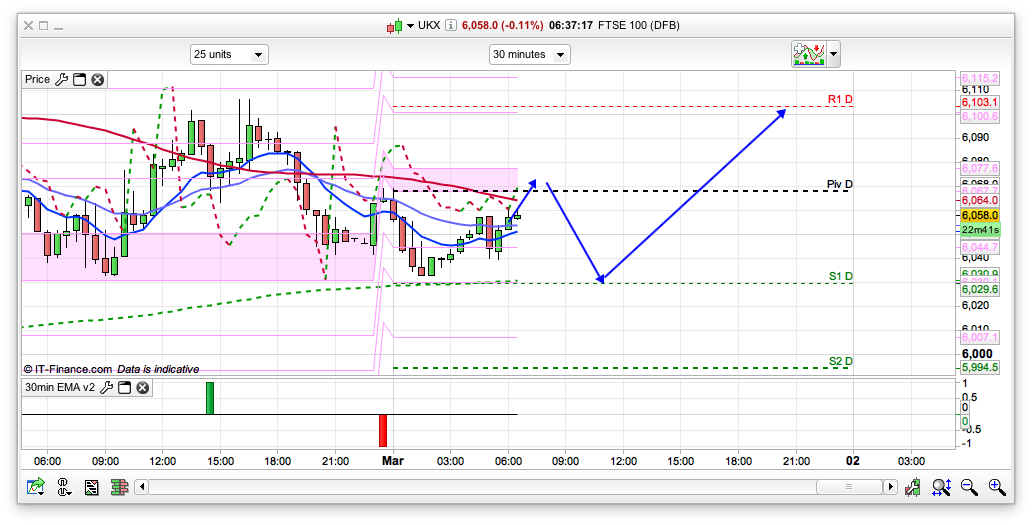

FTSE 100 Outlook and Prediction

For today there is initial resistance on the 2 hour chart at 6072 after crossing to a bear scenario overnight, so it will be telling to see if the bears start to appear at that level for a dip down towards the 200ema at 6030 on the 30min chart. Despite that rate cut news yesterday the bulls were hardly able to make it climb loads, and then with poor Chinese factory data overnight and further stimulus talk helping Asian markets, the FSTE has stayed around the 6060 area from last night. One again it looks like stock market growth will come from stimulus measures rather than a solid foundation. Kick that can a bit further once again! I digress. If the bulls manage to hold an early test of the 6030 area then I think we might see a bit of a bounce from there, mainly as the daily chart is still positive and the Raff channels are up at the moment, though I must admit I am feeling slightly more bearish than bullish at the moment, especially since we didn’t recapture 6115 yesterday which we saw on Friday (6110 was the 10 day Bianca high on Friday), so while that 10 day channel is now at 6194, the bulls are not really pushing on. Probably a bit early for Brexit worries, but that will be a factor in some sluggish moves. So, fairly simple plan really for today, initial dip from 6072 then bounce at 6030. Lets see if it plays ball!