Good morning. The main news yesterday was that Germany proved it wasn’t going to be dictated to and rejected the Greek bailout offer they made. As per usual I imagine it will go down to the wire, with crunch talks today, and Greece vowing to reject any further demands for austerity. “While there is mounting irritation in EU circles over Germany’s refusal to give ground, and signs of a Franco-German rift are emerging, the Greeks are on thin ice.” [Ref]. The bulls failed to break the 6920 resistance, though the 6970, despite an early dip, managed to hold as support. Everyone still keeping their powder dry really.

US & Asia Overnight from Bloomberg

(Bloomberg) — Japanese stocks extended their surge, with the Nikkei 225 Stock Average at a 15-year high, while Australian bonds dropped. Oil held losses as record U.S. supplies reinforced concern over a glut, and gold rallied.

The Nikkei 225 added 0.5 percent by 9:56 a.m. in Tokyo, while the broader Topix index climbed to its highest level since 2007 and headed for a fifth straight weekly gain. U.S. index futures were little changed after the Nasdaq Composite Index capped its longest rally in a year, while Australian stocks fell. Gold rose 0.2 percent to pare a weekly drop, and silver climbed 0.5 percent. Ten-year Australian bond yields advanced three basis points after U.S. Treasuries retreated. Oil in New York was headed for its first weekly decline in a month.

Record stimulus from the Bank of Japan is helping drive local stocks, with officials reiterating their monetary-policy stance this week. Markets in most of Asia remained closed for Lunar New Year holidays Friday, with investors looking to a meeting of finance ministers in Brussels for progress on Greece’s bailout negotiations. Manufacturing data for Japan to Europe and the U.S. is also due. American crude supplies rose a sixth week, extending a record high, a report Thursday showed.

“The Bank of Japan and GPIF have been the biggest drivers in pushing up stocks when they fell,” Masayuki Doshida, a senior market analyst at the Rakuten Economic Research Institute in Tokyo, said by phone, referring to the central bank and Japan’s public-sector pension fund. “The main scenario for Greece is that in the end it’ll be able to receive a concession. The market’s beginning to stop reacting to news on Greece ahead of a final agreement.”

Topix Gains

The Topix rose 0.4 percent in a fifth day of gains, its longest rally this year. A Markit Economics/ JMMA gauge of Japanese manufacturing due Friday is projected to show slight improvement.

Australia’s S&P/ASX 200 Index fell 0.3 percent, trimming its fifth straight weekly advance to 0.1 percent, the longest run of gains since April. Energy stocks led declines amid the drop in oil and after Santos Ltd., the country’s third-largest oil and gas producer, posted a loss for 2014 after the drop in crude prices forced it to write down the value of assets. Shares slipped 3.2 percent, the most in more than a month.

Telstra Corp., Australia’s largest phone company, fell 0.5 percent after saying that its chief financial officer would take over from Chief Executive Officer David Thodey.

The NZX 50 Index rose 0.5 percent in Wellington, its first day of gains this week. The measure is set for a 0.6 percent weekly decline, the second-worst performance after Greece’s ASE Index among 24 developed markets tracked by Bloomberg. The ASE has slumped 4.2 percent, with talks between Greece and its creditors breaking down earlier in the week.

Greek Outlook

The Stoxx Europe 600 Index added 0.3 percent Thursday, extending its highest close since November 2007.

The index swung around in European trade, rising as much as 0.4 percent after the European Commission said Greece’s request for an extension of loan facilities could pave the way for compromise. Stocks then pared gains on news Germany had rejected the plan, before rising again as a German official, who asked not to be named because the talks are private, said his government regarded a Greek proposal as a basis for negotiations.

U.S. Data

In the U.S., the Bloomberg Consumer Comfort Index’s monthly economic expectations gauge rose by 1 point to 54 in February, data Thursday in the U.S. showed, its highest level since January 2011. The Conference Board’s index of leading economic indicators, a measure of the outlook for the next three to six months, climbed less than forecast in January. A separate report indicated fewer Americans than forecast filed for jobless claims last week.

The mixed data came a day after minutes of the Federal Reserve’s January meeting signaled an inclination for officials to keep rates on hold “for a longer time” given the strong dollar and uncertainty over Greece and Ukraine.

While investors pushed back bets on when the Fed would raise interest rates, they’re still showing confidence an increase is possible by year-end. Fed fund futures traded on the CME Group Inc. exchange gave a 19 percent chance the central bank will raise rates at its policy meeting in June. They showed 77 percent odds of an increase by December.

West Texas Intermediate crude added 0.5 percent to $51.41 a barrel after sliding more than 4 percent the previous two days. WTI is down 2.6 percent this week, its first decline since losing 6.4 percent in the week to Jan. 23.

Oil Stockpiles

Crude supplies in the U.S., the world’s No. 1 oil consumer, increased by 7.72 million barrels to 425.6 million last week, the most in records compiled since August 1982 by the Energy Information Administration. The American Petroleum Institute reported stockpiles rose by 14.3 million barrels. Analysts surveyed by Bloomberg had predicted a median increase of 3 million barrels.

The highest U.S. crude production in three decades helped trigger a global glut that pushed oil prices almost 50 percent lower in 2014. Energy explorers are paring drilling rates and investments in response to the slump. Marathon Oil Corp. said Wednesday that it will cut an additional 20 percent from its spending plan for this year.

Gold climbed to $1,209.08 an ounce in the spot market, after retreating 0.5 percent on Thursday. The precious metal, often viewed as a store of value and haven investment, has lost 1.7 percent this week, on track for its fourth straight weekly loss and the longest slump since September 2013. Silver rose to $16.4595 an ounce.[Ref]

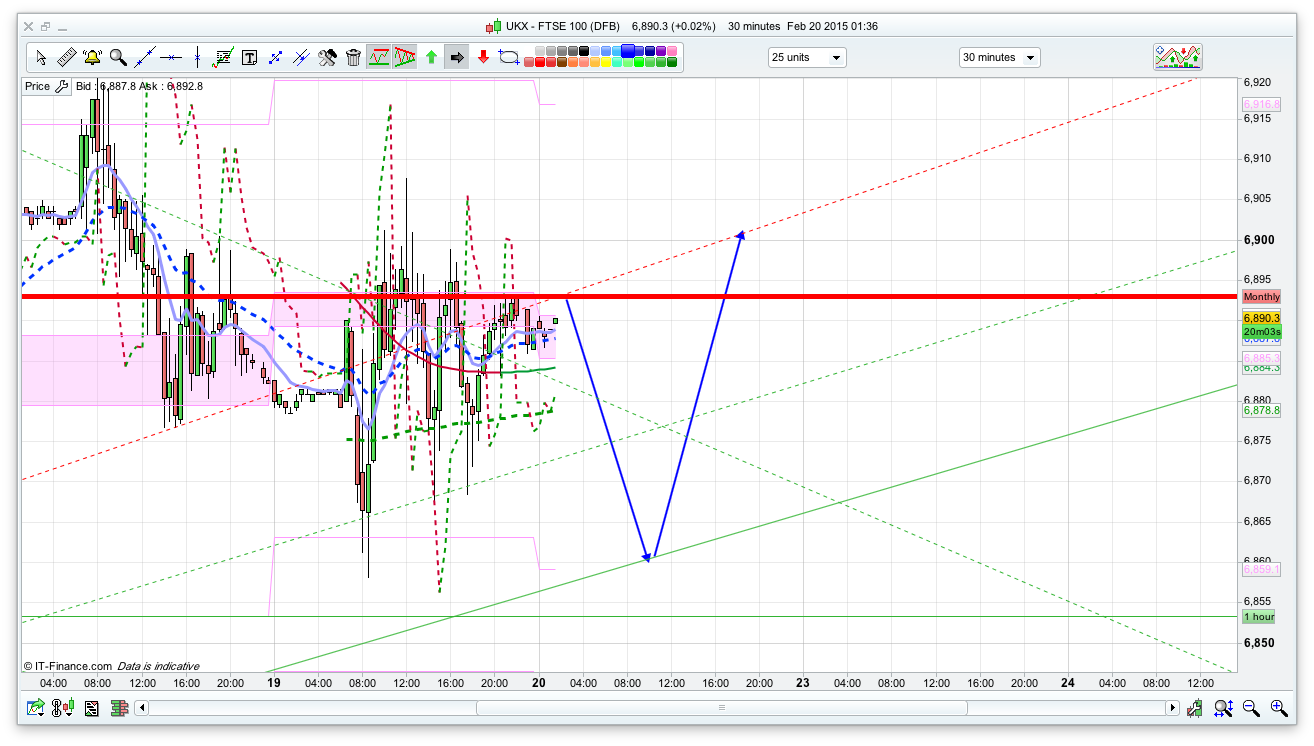

FTSE Outlook

Quite a narrow band on the 10 day Bianca now, with support at 6859 and resistance at 6933. Bulls will need to break 6910 first though, then that level should be achievable. Crunch talks, coupled with a Friday could make for an interesting session – hold over the weekend and hope for positive news, or close out and not have to worry which way it goes……

Support from the pivot initially at 6885, with 6865 below that, then 6659 for the Bianca 10 day. If that breaks then the 20 day at 6819 is worth a long. So, narrow range really in the absence of any news of note with 6959 and 6910 being the first levels of note to trade off. Despite Germany’s reaction yesterday prices have held up pretty well, though it won’t take much to derail the bulls. I expect a V shaped day today, with stutters around 6933/6939 if we get that high.