Good morning. Was a little bit too early shorting at 6190 as it popped up to the stop level at 6205 before dropping, though the bulls did fight back following the favourable Draghi press conference about more QE and another ready to do whatever it takes type comment. Overnight hasn’t been quite as favourable for the bulls and we are just above 6100 as I write this, with the NFP news due out today at 13:30. Expect volatility then! Also, US markets are closed on Monday for Labour day so the late afternoon might be a bit quieter. “We have very light volumes, a big U.S. holiday on Monday and with payrolls tonight, investors not doing much besides taking some risk down,” said David Welch, head of equity sales trading at Reorient Group in Hong Kong. “Yesterday’s bounce was artificial with China closed, and with the U.S. payrolls data tonight, people are taking risk off.”

US & Asia Overnight from Bloomberg

Asian shares headed for a seventh straight weekly slump and industrial metals slipped with the Australian dollar amid concern that China will pare back support for its stock market on Monday. U.S. equity-index futures fell before payrolls data, while the yen jumped.

The MSCI Asia Pacific Index was set for its longest weekly losing streak since 2011, while Hong Kong’s Hang Seng Index headed for its worst stretch since the collapse of Lehman Brothers Holdings Inc. in 2008. Copper, nickel and zinc fell with Australia’s currency, with Chinese markets closed for a holiday. The yen rallied toward its biggest weekly gain this year, and the euro was little changed after central bank officials signaled on Thursday they’ll boost economic stimulus if needed.

“There’s nervousness in the market about growth in Asia and the implications of the Fed changing policy should payrolls be seen as clearing the way for a hike,” said Sean Callow, a strategist at Westpac Banking Corp. in Sydney. “The fact that dollar-yen in particular is looking soggy is obviously a bad sign.”

The August nonfarm-payrolls report Friday may add fuel to the debate over whether the U.S. economy is strong enough for the Federal Reserve’s first interest-rate increase since 2006. Investors have pared bets on a September liftoff to 30 percent amid turmoil in global markets over the past month. Mainland Chinese markets will open Monday after signs of government intervention to prop up share prices before the nation’s World War II victory parade this week.

Stocks

The MSCI Asia Pacific Index dropped for the fourth time in five days, losing 1 percent by 12:57 p.m. in Tokyo as Japan’s Topix index declined 2.1 percent. The Asia-Pacific benchmark has fallen 4.8 percent this week and is down 15 percent since the end of June.

The Hang Seng Index dropped 0.5 percent on Friday. It’s heading for a 3.6 percent drop since Aug. 28, the seventh weekly decline in a row. The gauge has retreated 18 percent since July 17. A measure of Chinese companies listed in the city fell 1.7 percent to a two-year low Friday, down more than 6 percent for the week.

Futures on the Standard & Poor’s 500 Index slipped 0.7 percent. The nonfarm payrolls report represents the last major data point before the Fed meets on Sept. 16-17. U.S. markets are closed on Monday for Labor Day.

Futures traders have cut the probability of a rate increase in September from 38 percent at the end of last week, according to data compiled by Bloomberg. The figures are based on the assumption that the benchmark rate will average 0.375 percent after the first hike.

Australia’s S&P/ASX 200 Index fell a second day, retreating 0.1 percent to bring its drop in the week to 4.6 percent, the most since early June. The Kospi index in Seoul declined 0.5 percent.

The Dow Jones Industrial Average pared back an almost 200-point rally Thursday as traders cut holdings before the payrolls data, while Treasuries climbed amid the ECB’s comments on stimulus.

Currencies, Bonds

The yen, regarded as a haven in times of volatility, added 0.6 percent to 119.35 per dollar. It has climbed 2 percent versus the dollar this week, the best performance among 16 major currencies, and the biggest such advance since the five days ended Dec. 12.

Yields on 10-year U.S. notes dropped two basis points to 2.14 percent Friday, after slipping three basis points last session. Even though the Fed may be on the cusp of raising interest rates, 10-year Treasuries outpaced their Group of Seven peers during the August equities swoon.

The euro was on track for a second week of losses, the first two-week decline since July against the greenback, trading at $1.1125 after Thursday’s 0.9 percent slump.

The euro’s losses were fueled by the ECB’s decision to raise the limit on bond purchases per issue under its quantitative-easing program, as well as President Draghi’s comments that officials are willing and able to act to meet inflation targets.

The Aussie weakened 0.7 percent to 69.69 U.S. cents, and touched its weakest level since April 20, 2009. New Zealand’s dollar also lost 0.6 percent.

“We have very light volumes, a big U.S. holiday on Monday and with payrolls tonight, investors not doing much besides taking some risk down,” said David Welch, head of equity sales trading at Reorient Group in Hong Kong. “Yesterday’s bounce was artificial with China closed, and with the U.S. payrolls data tonight, people are taking risk off.”

Wheat futures dropped to a four-month low in Chicago on Friday, set for a 4 percent weekly decline on signs of ample global supply.

Copper fell 1 percent after rising to a three-week high in London on Thursday. The metal is 1.1 percent higher this week to head for a second weekly increase. [Bloomberg]

FTSE Outlook

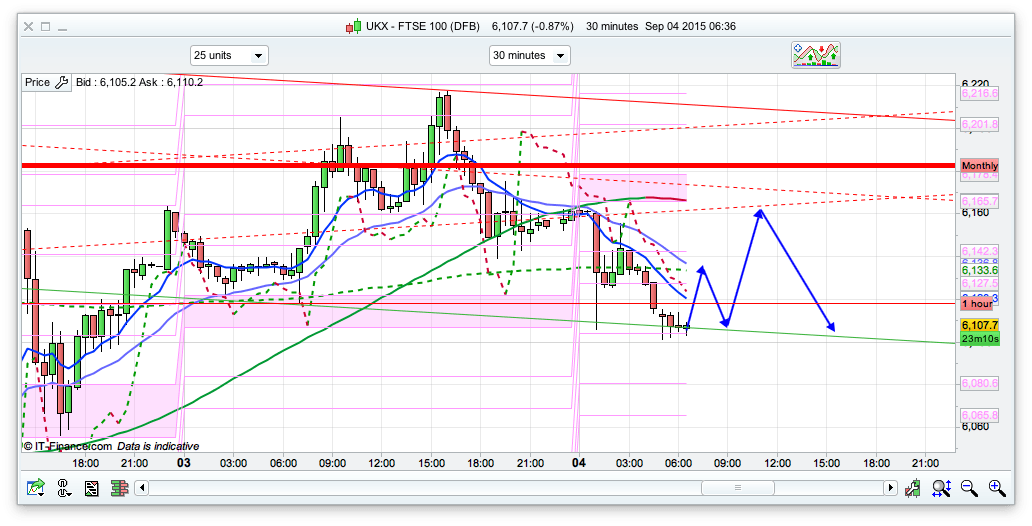

Its NFP Friday today so I expect it to be a little choppy and also with the US closedown Monday a fairly risk off sort of day, especially towards the end. Looking at the short term charts the moving averages are pretty bearish at the moment, and shorting the spikes seems a better play today. I have resistance at 6140 and 6165 is the daily pivot so those levels look decent enough initially. I think the bulls will try and defend 6100 quite hard to then try and build on yesterdays rise next week but today I can see maybe being a bit lacklustre. Time will tell! If 6100 were to break then the next decent support is down at 6012 and 6000 for the bottom of the 10 day Raff. I might be a bit more optimistic next week though for the FTSE to push up towards 6300/6400.