Good morning. We got a decent rise from the 6160 level yesterday for the long but banking near 6200 was the right thing to do as it dropped back down to 6130 after that. However, the bulls are persistent and the FTSE has crept up again since. They really do need to hold 6200 today for a rise back to 6300+ next week. I thought we might have seen that level this week, but the spike and dump on Wednesday to 6300 put paid to that. Nice drop on the S&P as well after the 1954 entry which got a few points too. We have a consumer confidence report out at 3pm in the US today, which might help gauge rate rise chances next week. Its still all eye on the Fed really and the 17th Sept to see what rates are going to do.

US & Asia Overnight from Bloomberg

Asian stocks fell, paring the regional benchmark measure’s first weekly advance since July. Consumer and industrial shares declined.

The MSCI Asia Pacific Index declined 0.2 percent to 127.17 as of 9:02 a.m. in Tokyo. Most of this week’s 1.9 percent gain came on Sept. 9, when stocks in Japan soared in a rally that analysts said was fueled by short-sellers closing bearish bets. Investors are grappling with heightened global equity volatility as they await the Federal Reserve’s decision next week and watch developments in China.

“Markets have been wild and fear is still near its zenith,” said Tim Shirata, Los-Angeles based executive vice president at Guild Investment Management Inc. “Pessimism about China and the world economic outlook is widespread, and optimism about continued economic growth in the U.S. is declining. We hold a lot of cash, and are waiting patiently for opportunities to invest it.”

The Standard & Poor’s 500 Index rebounded from a selloff Thursday amid low trading volumes. Federal Reserve officials in recent weeks, while acknowledging a global equity rout that followed China’s currency devaluation, haven’t been willing to rule out a September interest-rate increase. While rate futures traders have pared bets, many economists are still predicting the Fed will increase its key rate.

Japan Volatility

Japan’s Topix index declined 0.8 percent. After the Nikkei 225 Stock Average’s 7.7 percent surge on Sept. 9, short-term price swings in Tokyo are topping those in Shanghai for the first time this year. With the country’s economy struggling to gather momentum after a contraction last quarter, more than a third of economists see the central bank expanding monetary stimulus by next month, according to a Bloomberg News survey.

Eleven of 35 respondents see the Bank of Japan stepping up its easing on Oct. 30, while two forecast a move as early as next week, the Sept. 7-10 survey shows. The central bank last expanded asset purchases in October 2014.

South Korea’s Kospi index retreated 1 percent. Australia’s S&P/ASX 200 Index rose 0.1 percent and New Zealand’s NZX 50 Index added 0.2 percent. Markets in China and Hong Kong are yet to open.

Singapore’s cash equity market is closed for a holiday as the nation heads to the polls with Prime Minister Lee Hsien Loong’s People’s Action Party expected to win re-election.

Futures on the FTSE China A50 Index in Singapore slipped 0.2 percent in most recent trading. Contracts on the Hang Seng Index added 0.3 percent and those on the Hang Seng China Enterprises Index advanced 0.7 percent. E-mini futures on the S&P 500 slipped 0.1 percent. [Bloomberg]

FTSE Outlook

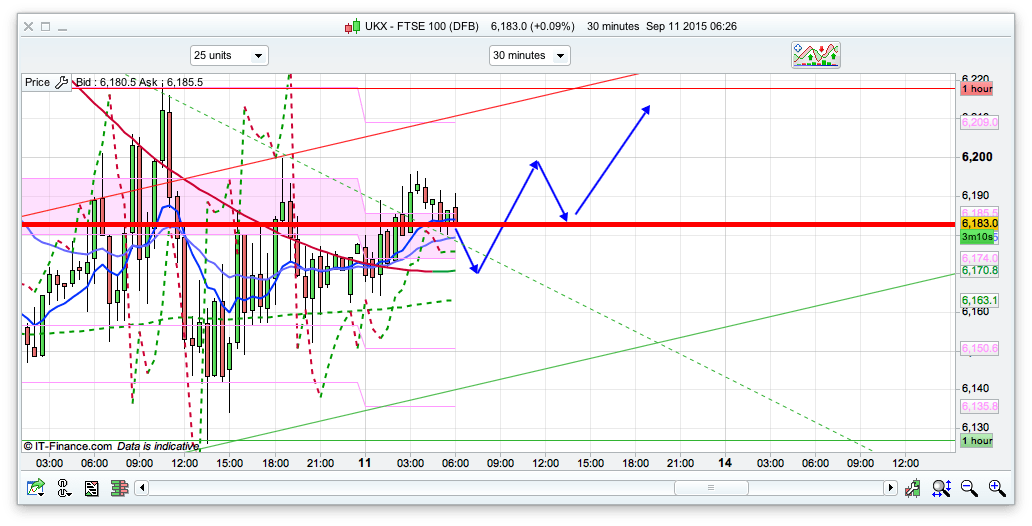

I am looking for the 6170 area to hold as support this morning and then a possible rise, and close above 6200. That could then be a decent springboard for a rise further next week. That said, if we do rise past 6200 then we would be nearing the top of the 10 day daily resistance channels once again, 6276 for Bianca and 6306 for the Raff. At the moment my 2 hour chart is bearish, but its weak., while the shorter timeframes – 10 and 30min – are both bullish to start things off today. There is a pretty decent rising channel on the 30min chart as you can see below, this has resistance at 6215and support at 6145ish, so i think these outer extremes are worth a trade today if seen. Apart from that its probably a bit of wait and see Friday, with everyone awaiting clues from the Fed on US interest rates.