Good morning. Not the best day for the order trades yesterday with the FTSE long getting stopped out, Dax and S&P missing (just!), but the gold long at 1172 ran to target at 1178 so all was not lost. The Dow had an interesting little spike up at the closing bell to hit the 17250 level mentioned yesterday – thought it might have tried to hit that properly rather than a spike but anyway, hit it it did, and then dropped back 70 odd points so far. There is a chance that was the last little hurrah from the bulls and we are on for a leg down now (16500 maybe on Dow). Certainly Tuesday’s session in Asia has been a little weaker, and the ASX has dropped so the FTSE might we’ll follow suit today. Apart from that quick move to test 6410 yesterday was pretty bearish too in the end.

US & Asia Overnight from Bloomberg

Asian stocks fell, paring the benchmark regional equities gauge’s biggest monthly rally in five years, as material shares led losses.

The MSCI Asia Pacific Index slipped less than 0.1 percent to 134.01 as of 9:08 a.m. in Tokyo. The gauge surged 8.3 percent this month through Monday, on course for its best monthly advance since September 2010, as Chinese shares rallied and traders pushed back expectations on the timing of the Federal Reserve’s first interest-rate increase. The global stock rebound in October has restored more than $4 trillion in equity value.

“The three-week recovery is approaching an exhaustion point,” said Matthew Sherwood, head of investment strategy at Perpetual Ltd. in Sydney, which manages about $21 billion. “Valuations have expanded and 2016 earnings have not been upgraded.”

The October surge pushed valuations on the MSCI Asia Pacific index this month back above their five-year average, Bloomberg data show. The index trades at 13.6 times estimated earnings, the data show. Equity gains came after last quarter’s volatility triggered by China’s surprise decision to devalue the yuan in August.

Japan’s Topix index gained 0.5 percent. South Korea’s Kospi index was little changed. New Zealand’s S&P/NZX 50 Index rose 0.7 percent.

Australia’s S&P/ASX 200 Index dropped 0.3 percent. The nation’s banking regulator will take additional steps by the end of 2016 to ensure Australia’s lenders have strong capital levels, the government said Tuesday in its response to the Financial System Inquiry.

E-mini futures on the Standard & Poor’s 500 Index slipped 0.1 percent. The underlying gauge closed little changed on Monday at the highest since Aug. 20, rising above a level where past rallies since the summer selloff have lost momentum. International Business Machines Corp. fell in late trading as quarterly revenue missed estimates. [Bloomberg]

FTSE Outlook

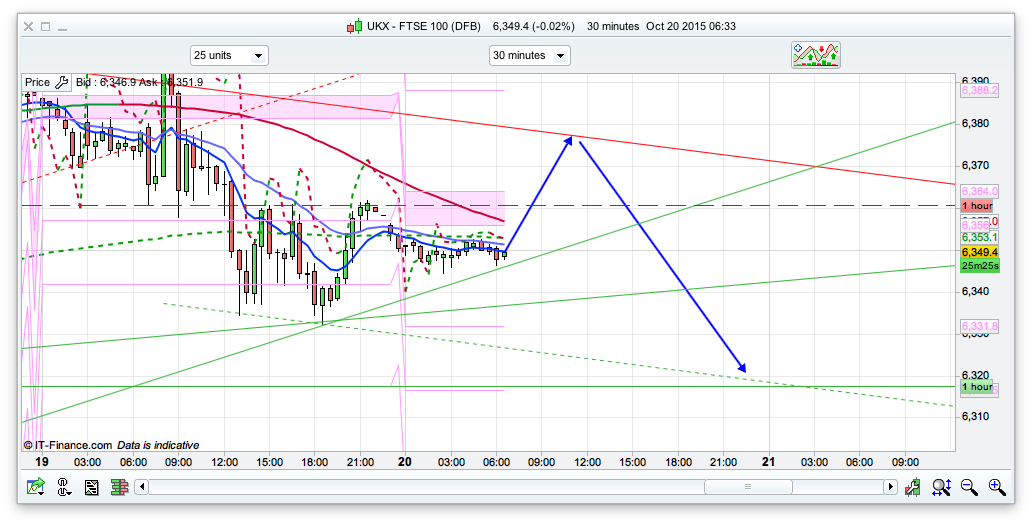

I have gone for an initial climb off the 6345 support area to test the top of that declining 30min channel, however I think the swing might be gong the bears way over the next few sessions. That spike not he Dow last night looked a bit suspicious (mind you, so did the FTSE spike up to 6410 then swift reversal yesterday). We are just below the daily pivot at 6351 as I write this, and the top of the 10 day Bianca channel is slightly lower today so starting to move downwards. Bears will be keen to 6280 on any downside moves as there is daily support there. As mentioned above looking at dow, we could get a leg down to 16500 from 17250 last night, which would take the FTSE down to 6100ish, maybe lower. Initially it all looks bearish for the moving averages on the 10min and 30min charts, so the bulls will need to be quick out the blocks to break the 6351 pilot for a push up. The 2 hour chart has resistance at 6362 as well, so a small short around these area could be worth a go if you fancy backing the early bears! Other wise wait for 6375.