Good morning. The FTSE and S&P shorts worked out well yesterday, with the FTSE having quite a dip form the 6362 area (which was nice!), though unfortunately went short on the Dax just a bit too early, getting stopped at 10185 before a 100 point drop. Frustrating that one sometimes! After the morning dip across the board the bus fought back and tested the 6350 are on the FTSE which has proved to be a fairly key area, acting like a magnet. Overnight Asia strength has pushed it back up to 6375, opening up the chance for 6410, the top of the 10 day Bianca channel. The Australian ASX200 put in a bullish performance today, so the FTSE may well follow suit – bearish morning then a bullish afternoon (again).

US & Asia Overnight from Bloomberg

Asian stocks rose with U.S. and U.K. equity-index futures as weak trade data from Japan bolstered speculation that central banks will add stimulus to address sliding global demand. Oil traded near $46 a barrel, while aluminum led industrial metals lower.

Shares in Tokyo and Jakarta led gains, driving the MSCI Asia Pacific Index to its first gain this week. The yen held near a one-week low as the slowest expansion in Japanese exports in more than a year sparked bets the central bank may boost its unprecedented asset-purchase program when it meets Oct. 30. Crude’s fall ahead of U.S. stockpiles data helped the Malaysian ringgit extend declines into a fourth day. Aluminum is heading for its longest losing streak in three months.[Japan’s QE program has underpinned stock gains]

Japan’s QE program has underpinned stock gains“Whenever we get negative economic news, hopes for additional monetary easing moves the market,” Takashi Aoki, a fund manager at Mizuho Asset Management Co., which manages the equivalent of about $33 billion, said by phone. “We’re starting to see hard evidence for our fears about the global economy being weak.”

The Japanese data add to a string of reports that highlighted how weakness in China’s economy is being transmitted to its trading partners. As the end-of-October Bank of Japan meeting looms, about a third of the economists surveyed by Bloomberg are predicting the stimulus program will be expanded. Traders have been paring back bets for a Federal Reserve interest-rate increase this year amid signs that the slowdown threatens the U.S. recovery and corporate earnings. The European Central Bank meets on Thursday.

Stocks

The MSCI Asia Pacific Index added 0.8 percent by 1:46 p.m. in Tokyo as Japan’s Topix index jumped 1.7 percent. Futures on the Standard & Poor’s 500 Index added 0.5 percent, after the U.S. benchmark gauge dropped 0.1 percent Tuesday, the second straight day it has closed little changed. Contract on London’s FTSE 100 Index advanced 0.4 percent.

Commodities

December futures on West Texas Intermediate crude slipped 0.5 percent to $46.04 a barrel. November contracts, which expired Tuesday, slipped 0.7 percent last session to $45.55, the lowest close since Oct. 2. Brent also fell, declining 0.3 percent to $48.59.

U.S. oil supplies expanded by 7.05 million barrels last week, the American Petroleum Institute was said to have reported Tuesday. Energy Information Administration data due Wednesday is forecast to show inventories rose by 3.75 million barrels, according to a Bloomberg survey.

Aluminum fell for a sixth day, headed for its longest losing streak in almost three months. The metal in London dropped 0.1 percent to $1,530 a metric ton after closing Tuesday at an eight-week low.

Nickel lost 0.1 percent and copper slid 0.3 percent as the Japan trade data compounded concerns about global demand after China, the world’s biggest commodities consumer, reported on Monday its weakest quarterly growth since the global financial crisis.

Gold extended gains, rising 0.2 percent to $1,177.92 an ounce as investors awaited next week’s Fed meeting. The precious metal sees greater demand when speculation over a rate increase is low as it doesn’t pay out interest like fixed-income assets.

Bonds

A gauge of U.S. sovereign bond market volatility dropped to 71 basis points this week, from 95 basis points as recently as August, as futures traders predict the Fed will be sidelined until March. The lowest level this year was 70 basis points at the end of July. Yields on benchmark 10-year notes have hovered near 2 percent since the start of this month. [Bloomberg]

FTSE Outlook

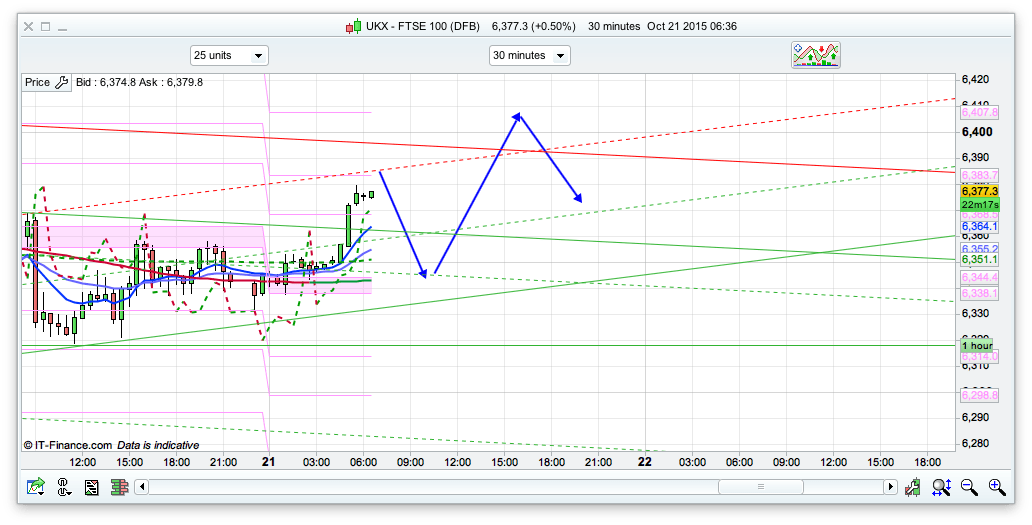

Looking at the 30min chart I think we could get a little dip of the channel at the 6390 area to start the day, however, I think the bulls want to test 6410 where we have the top of the 10 day Bianca. A pullback from that level could well be a good place to short, as the bulls have recently failed to hold on above 6400. Maybe it will be third time lucky and the top of the 10 day Raff at 6455 is possible – so tight stops on the 6410 short. We have a divi of 8.9 for the FTSE today so bear that in mind for position open at the close (if your platform applies them at 16:30) as that will effect open positions. Probably won’t see too much divi hunter action int he run up to the bell though for only 8.9 points. So, generally today I am now thinking we will get a run at 6410 to test the daily channel, but I think the bears will have a go there, as the top of the 10 day channel has been adjusting lower each day this week (possible start of downtrend).