Good morning. The big news yesterday was the ECB press conference where, after leaving rates unchanged, further stimulus was mentioned yet again to keep things growing. “The degree of monetary-policy accommodation will need to be reviewed at our December meeting when new macroeconomic projections will be available,” Draghi said. “We want to be vigilant, as people used to say in the old times.” Draghi’s predecessor Jean-Claude Trichet used the phrase “vigilant” to warn of upcoming changes in policy. The 19-nation region’s woes include a global economic slowdown that is weighing on overseas sales, and a currency appreciation that’s putting downward pressure on inflation. Consumer prices fell in September and while that is largely due to a drop in energy costs, there’s concern that the declines may become entrenched. The FTSE climbed to the 6400 level where a short got a few points with a dip to 6380, before an overnight rise to 6430. Earlier in the day the automated trades ended up being stopped at breakeven despite moving into profit initially.

US & Asia Overnight from Bloomberg

Asian stocks rose, joining a global equities rally, after the European Central Bank signaled it may boost stimulus this year. The MSCI Asia Pacific Index gained 0.5 percent to 134.48 as of 9:02 a.m. in Tokyo.

The MSCI All-Country World Index of developed and emerging-market shares surged to a two-month high on Thursday after ECB President Mario Draghi said policymakers will re-examine the degree of stimulus in December, adding that the quantitative-easing program will continue until beyond September 2016 if needed.“Investors interpreted this as meaning a greatly increased chance of more policy support,” said Matthew Sherwood, head of investment strategy at Perpetual Ltd. in Sydney, which manages about $21 billion. “The good thing for central banks is that they have most investors so hooked on the stimulus drug that all they have to do is boost supply and the patient will be happy again.”

Japan’s Topix index climbed 1.7 percent and Australia’s S&P/ASX 200 Index gained 2.1 percent. South Korea’s Kospi index rose 1.1 percent and New Zealand’s S&P/NZX 50 Index added 0.7 percent.

E-mini futures on the Standard & Poor’s 500 Index added 0.6 percent since the close of cash-market trading on Thursday. The underlying gauge advanced 1.7 percent Thursday.

After the market closed, Google parent Alphabet Inc. reported better-than-projected earnings amid stronger ad sales and while keeping expenses under control. It soared in extended trading, as did Amazon.com Inc. after the Internet commerce company’s quarterly sales topped analysts’ estimates.

Futures on Hong Kong’s Hang Seng Index gained 1.3 percent and contracts on the Hang Seng China Enterprises Index advanced 1.6 percent in most recent trading. Futures on the FTSE China A50 Index rose 1.3 percent in Singapore. [Bloomberg]

FTSE Outlook

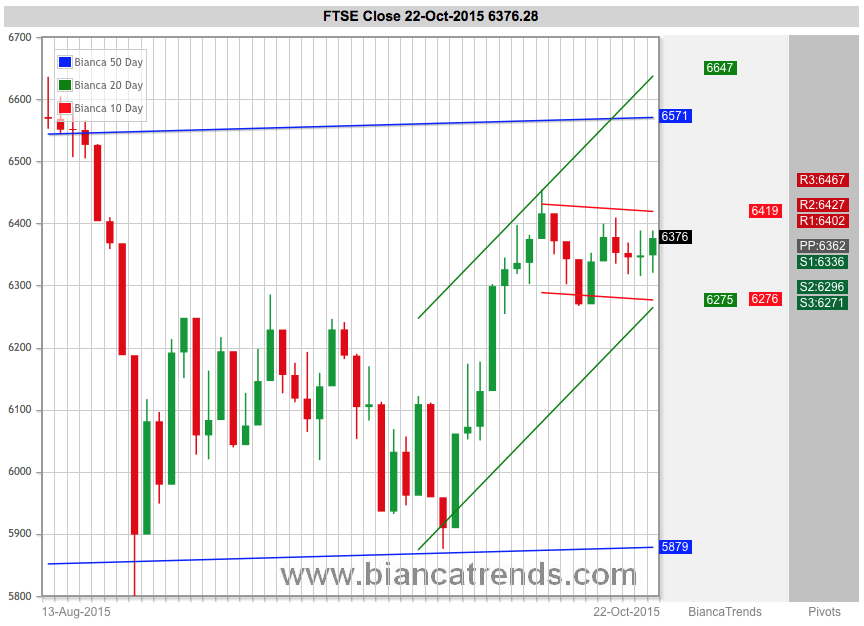

Fairly decent rise overnight off the back of the Asia session to test 6432, and with he top of the rising 10min channel at 6425 we might test that again. The top of the 10 day Bianca channel for today is 6419 so I think a short at around this area might well pay off, as people look to crystallise some profits from yesterdays rise and going into the weekend. With the stimulus talk the worm has turned for the moment so we are all good, with the Chinese slow down forgotten about for the moment. If we do dip from here then i expect a test of the daily pivot initially at 6389, and then possibly as far as the 200ema on the 30min to 6362 area. If that holds then the bulls should be able to go for a push again towards 6400 to close out the week on a fairly positive note. So a fairly simple plan for today really, as its Friday and all!