Good morning. It was a mainly quiet day on the FT100 on Friday with Wall Street having a shortened day of trading. The 6350 long ran up for a few points, whilst the Dax was the best performer for the trade plan, playing out as predicted rising to 11350 then falling back. The only news which moved the market was some weak China economic data overnight and a fall on the Shanghai index due to some broker irregularities. This and a negative announcement from Anglo American had a knock-on effect on the commodity sector which fell around 4%.

US & Asia Overnight from Bloomberg

Asian stocks fell after Chinese shares posted the biggest one-day selloff in three months. Material and consumer-staple shares led losses on the benchmark index at the start of a pivotal week for the region’s markets.

The MSCI Asia Pacific Index lost 0.3 percent to 132.82 as of 9:02 a.m. in Tokyo, headed for a monthly loss of 1.2 percent, its sixth such decline in seven months. This week brings a decision by the European Central Bank and the last reading on U.S. jobs before the Federal Reserve decides on whether to raise interest rates in December. The Shanghai Composite Index dropped 5.5 percent on Friday, its largest retreat since the depths of a market rout in August, as regulators clamped down on brokerages.

“The main event is the ECB moving on Thursday and the U.S. non-farm payrolls on Friday,” said Mark Matthews, head of Asia research and a managing director of Bank Julius Baer & Co. in Singapore. Friday’s move in Chinese markets was “a positive because they were investigating brokers, which is a sign they don’t want another bubble to form, which was happening as it was up about 25 percent just in the last couple of months. It was oversold on Friday and I would expect it to bounce today.”

Japan’s Topix index lost 0.3 percent. Data Monday showed a preliminary reading for industrial production rose less than economists estimated in October compared with the previous month, while retail sales climbed more than they had expected.

Regional Gauges

Australia’s S&P/ASX 200 Index added 0.1 percent. Dick Smith Holdings Ltd. plunged 47 percent in Sydney after the electronics retailer said it sees a A$60 million ($43 million) writedown and abandoned its profit forecast.

New Zealand’s S&P/NZX 50 Index increased 0.4 percent. South Korea’s Kospi index fell 0.8 percent. Futures on Hong Kong’s Hang Seng Index added 0.3 percent in most recent trading, while contracts on the FTSE China A50 Index slid 0.2 percent.

China’s securities regulator is investigating Citic Securities Co., Haitong Securities Co. and Guosen Securities Co. over alleged breaches of rules on margin and short-selling contracts. Shares of Chinese brokerages led the decline on Friday.

E-mini futures on the Standard & Poor’s 500 Index fell 0.2 percent after the underlying gauge climbed 0.1 percent on Friday in a shortened session. As investors await payrolls figures for November, traders are now pricing in a 72 percent chance the Federal Reserve will raise interest rates in December.

ECB Meeting

European policy makers meet Dec. 3 to discuss monetary policy and what the ECB can do to prop up sluggish inflation within the region. The central bank is considering cutting its deposit rate further below zero and adding to its program of quantitative easing.

International Monetary Fund Managing Director Christine Lagarde and some two dozen officials on the fund’s executive board gather Monday in Washington to decide whether to grant China’s yuan status as a reserve currency by adding it to the fund’s Special Drawing Rights basket. While Lagarde has already announced that fund staff had recommended the yuan be included and that she supported the finding, the IMF is likely to give more details on how it arrived at the decision.

This week also sees a policy decision from the Reserve Bank of Australia, while members of the Organization of Petroleum Exporting Countries will gather in Vienna. [Bloomberg]

FTSE Outlook and Prediction

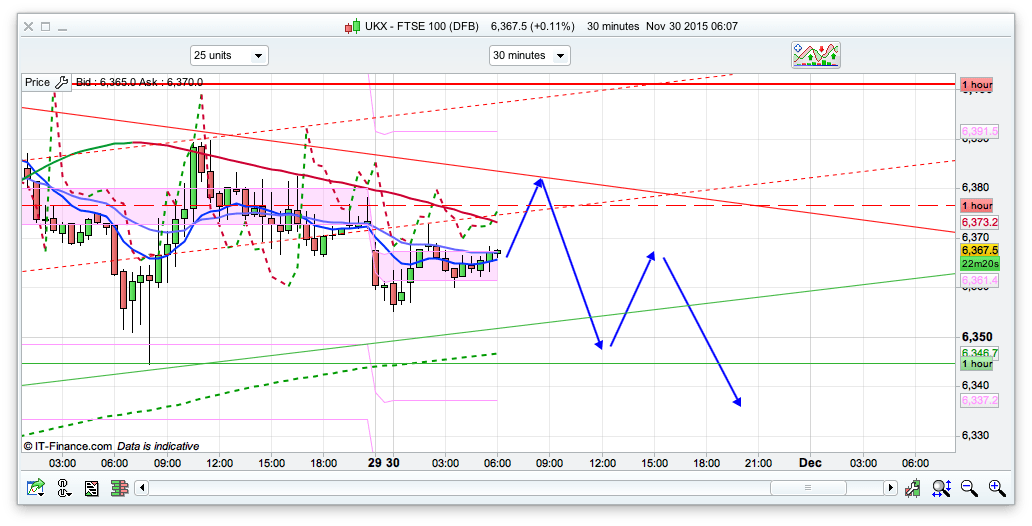

I am feeling a little bearish this morning looking at the charts, with a decline from the 6380 level towards the 6315 area looking distinctly possible. We have the daily pivot at 6369, as well as the hull ma (2hour) showing resistance at 6377. A short around this area first thing this morning could set the tone for the day, especially as Asia stocks have fallen during Mondays session. The ASX200 (Australia) had a little rise initially then fell back also. I think the FTSE will follow the same pattern today. However, if not and the bulls manage to break the 6380 area of resistance then a rise towards the top of the Bianca channels at 6450 is possible. We have an ECB meeting on 3rd December which may yield further monetary stimulus, so might see some more bullishness around then in anticipation of that. 6345 area is going to be initial support today, as that was Fridays low that we bounced off, the bottom of a rising 30min channel and the 200ema on the 30min there also.Therefore the bears, if they show up first thing, will be keen to break through this strong area of support to target the 6315 level. Below 6300 and there is quite a lot of fresh air till 6200 and 6140 so the bulls will be keen to defend this area.