Good morning. The market had a bit of a spike down at the open yesterday on negative announcements from mining company BHP Billiton and Aberdeen Asset Management, unfortunately not quite low enough to trigger the buy at 6320 though, hitting 6328 instead. During the rest of the day the market stabilised and traded near the unchanged level as most eyes were on the ECB announcement on Thursday. The short at 6378 managed a few points but it was a pretty lacklustre session once the bounce from the 6328 had occurred. It looks like a wait and see situation for traders and so we could be locked into the 6325-6425 range until Thursday.

US & Asia Overnight from Bloomberg

China’s benchmark stock index fell to the lowest level in a month after official data showed manufacturing conditions are deteriorating.

The Shanghai Composite Index slipped 0.5 percent to 3,427.25 at 1:06 p.m., led by financial and energy companies. China’s slump was in stark contrast to regional markets, including Hong Kong, where the Hang Seng China Enterprises Index jumped 1.9 percent to halt a six-day losing streak. The yuan weakened 0.2 percent in offshore trading after the International Monetary Fund said it would add it to its basket of reserve currencies.

The Shanghai Composite’s rebound from a $5 trillion rout is starting to ease after the gauge closed out November with a 1.9 percent gain, the smallest percentage move since January. Rising investor optimism with the return to a bull market earlier in the month has given way to caution as the government started withdrawing market support. Recent data have also mostly been dismal with exports falling, industrial output slowing and producer prices continuing declines. Tuesday’s report showed the official purchasing managers index at 49.6 in November, down from October’s 49.8 and below the level of expansion.

“Sentiment in the Shanghai market was affected by the PMI number,” said William Wong, head of sales trading at Shenwan Hongyuan Group Co. in Hong Kong. “The SDR bid has translated to an irreversible process of financial liberalization and will benefit China’s financial sector in the long run. The A shares will react to the news over time.”

In Shanghai, coal producers led declines for energy producers, with Wintime Energy Co. plunging 2.1 percent. Bank of China Ltd. paced losses for lenders, sliding 2.7 percent. Brokerages also retreated, with Western Securities Co. dropping 4.1 percent.

China’s manufacturing conditions slipped to the weakest level in more than three years as sluggishness in the nation’s old growth drivers add to risks facing the government’s growth target of 7 percent. Six central bank interest-rate cuts in a year haven’t been enough to spur a recovery in manufacturing, which has continued to weaken while activity in the services sector has shown more strength.

Another manufacturing PMI released by Caixin Media and Markit Economics edged up to 48.6 in November, exceeding the median estimate of 48.3. The gauge has a smaller sample size and includes smaller companies and exporters.

Hong Kong’s H-shares gauge headed for its biggest gain in a month, benefiting from a return of risk appetite. Benchmark share measures from Tokyo to Sydney and Seoul climbed at least 1 percent as Standard & Poor’s 500 Index futures rose 0.5 percent. The H-shares measure slumped 5.8 percent last month, the worst performance among major stock gauges in Asia.

IMF Move

The IMF said the Chinese currency will join the dollar, euro, pound and yen in its Special Drawing Rights basket. While yuan inclusion is short-term negative for Chinese stocks, it is positive in the long term, UBS Group AG analysts wrote. The risk of depreciation is likely negative for stocks on a three- to six-month time horizon, they said. Still, increased capital account opening and further domestic capital market development, coupled with very low global exposure to Chinese assets currently, could bring more inflows in the long term, they said.

“We see in particular the yuan inclusion to the SDR basket has lifted sentiment in the Asian stock market,” said Adrian Zuercher, the Hong Kong-based head of Asia asset allocation at UBS. “We think Asia is attractively valued and there is too much pessimism on China.”

U.S. short sellers are piling on bets against Chinese equities at the fastest pace since the height of the nation’s stock-market bubble five months ago. Short interest in the largest U.S. exchange-traded fund tracking domestic Chinese stocks more than doubled in two weeks to a record 28 percent of shares outstanding on Nov. 27, according to data compiled by Markit and Bloomberg. When such wagers last climbed this fast in June, short sellers proved prescient as China’s equity-market boom turned into a bust.

Hong Kong’s Hang Seng Index rose for the first time in seven days, adding 1.7 percent. The CSI 300 Index declined 0.5 percent.

“Hong Kong has dropped for quite a few days so they’re taking it as an excuse to squeeze those short sellers and the latter has to do short covering,” said Louis Tse, a Hong Kong-based director at VC Brokerage Ltd. [Bloomberg]

FTSE Outlook and Prediction

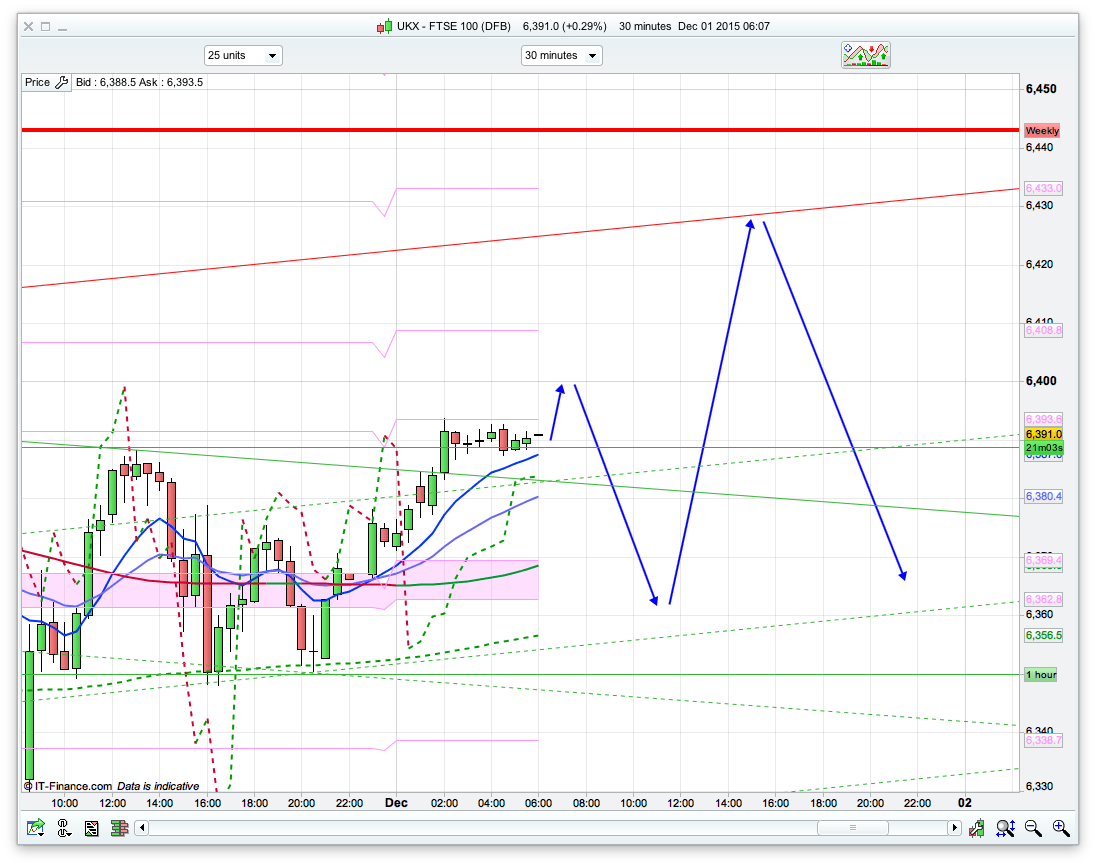

As mentioned above its a bit of wait and see till the ECB on Thursday and what, if any, stimulus measures might be announced. We also have a commons vote on Wednesday about bombing Syria, though markets have largely remained unperturbed by this. Anyway, onto today. We have the pivot at 6363 so I think we may see some support here initially, though the 6326 area is support below this where we have the 10 day Bianca channel and yesterday’s low – so worth a long at this level if it gets this level. Resistance wise we have 6400 as the main attraction, with 6425/6430 above that and worth a short from. It’s the first day of the new month so usually slightly bullish as there is the influx of new money for the month, but any initial rise to the 6430 area this morning could easily reverse. Gold has moved up off its recent lows, and we had a bullish ASX session today, so there is a slight bullish tinge to todays proceedings!