Good morning.

Market Summary for Friday

When it appeared the markets were stabilising and we were building towards a test of 6000 on the FT100, Friday comes along and destroys the consolidation of the previous days!

Oil plummeted again and was the main driver of the market move, breaking down below the $30 barrel level. BHP caused the trigger for a very negative open by writing down its shale assets by a few billion and this had knock on effects to other commodity shares. Iran sanctions have been lifted over the weekend and likely to add an extra 500,000 bpd which could lead to a further weakening in the oil price.

Shares slipped for most of the day however did stabilise on the Wall Street open to close near the 5800 level. This level has not been seen since November 2012 so over 3 years of gains have been wiped out by the current correction. Fortunately, the lower support level at 5740 that I mentioned held well (5936 was the low) and we have a seen decent and sustained bounce from this level. Too early to say if its “the” low but its looking like its generated some buying activity.

US & Asia Overnight from Bloomberg

Nikkei 225, S&P/ASX 200 indexes down 19% from 2015 peaks

Oil price below $30 a barrel for first time in 12 years

Asian stocks slumped, with Japanese and Australian shares on the cusp of joining China in a bear market, as concern grew over the strength of the global economy amid a continuing collapse in oil prices.

The MSCI Asia Pacific Index lost 1 percent to 118.94 as of 11:10 a.m. in Tokyo, extending this year’s slide to 9.9 percent. Japan’s Nikkei 225 Stock Average declined 1.4 percent after plunging as much as 2.8 percent in early trading. The gauge is down 19 percent from a June peak. A drop of more than 20 percent at the close would meet the definition of a bear market. Australia’s S&P/ASX 200 Index slipped 0.7 percent, and is currently down 19 percent from an April high.

Oil is below $30 a barrel for the first time in 12 years as global growth worries roil equity, bond and currency markets. Investors awaited 2015 gross domestic product estimates from China on Tuesday as it struggles to boost a slowing economy and money managers debate how many times the Federal Reserve will raise interest rates this year.

“Worries about China, the Fed and global growth are likely to drive continued share market weakness and volatility in the short term,” said Shane Oliver, head of investment strategy in Sydney at AMP Capital Investors Ltd., which oversees about $115 billion. “Expect volatility to remain high.”

Traders have been whipsawed in 2016, with equities around the world off to their worst start to a year on record as oil plummeted to levels last seen more than a decade ago and China struggled to maintain control over its markets.

The Shanghai Composite Index entered a bear market last week, for the second time in seven months, amid persistent investor concern over volatility. China’s stock-market watchdog has acknowledged ineptitude and loopholes within its regulatory system after a review of the turmoil that has rocked local markets since June.

The measure rose 0.2 percent Monday as China’s central bank strengthened its daily reference rate for the yuan by 0.07 percent, the biggest gain in four weeks. The People’s Bank of China will impose reserve-requirement ratios on yuan deposits held on the mainland by offshore participant banks from Jan. 25, according to people familiar with the matter. Premier Li Keqiang on Friday pledged a “stable” exchange rate, and said the nation has no intention of stimulating exports through competitive currency devaluation.

The MSCI Asia Pacific Index has been in a bear market since August, as global equities plummeted after China devalued the yuan. The gauge is trading at the lowest level since 2012.

Japan’s Topix fell 1.3 percent on Monday, bringing its losses from an August high to 18 percent. Hong Kong’s Hang Seng Index retreated 0.9 percent, extending a three-year low, and South Korea’s Kospi index dropped 0.2 percent. Singapore’s Straits Times Index lost 1.3 percent. The market is one of the worst global performers over the past year, with the benchmark gauge down more than 25 percent from a peak.

New Zealand’s S&P/NZX 50 Index slid 1.5 percent. Australia’s ASX 200 pared earlier losses as Woolworths Ltd. surged 4.8 percent after saying it’s exiting Masters — its unprofitable Australian home-improvements joint venture with Lowe’s Cos.

Both U.S. crude and Brent settled below $30 a barrel at the end of last week and the Standard & Poor’s 500 Index sank 2.2 percent Friday. Brent oil briefly dropped below $28 a barrel on Monday after international sanctions on Iran were lifted, paving the way for increased exports from the OPEC producer amid a global glut.

Futures on the S&P 500 rose 0.2 percent. U.S. markets are closed Monday for a holiday.

The U.S. economy is weaker than expected though probably not headed for recession in 2016, Mohamed A. El-Erian said in an interview on Fox News.

“We are experiencing a lot of volatility. Growth and wages are lower than where we could’ve been, but let’s not forget it’s an economy that creates a lot of jobs,” Allianz SE’s chief economic adviser said. [Bloomberg]

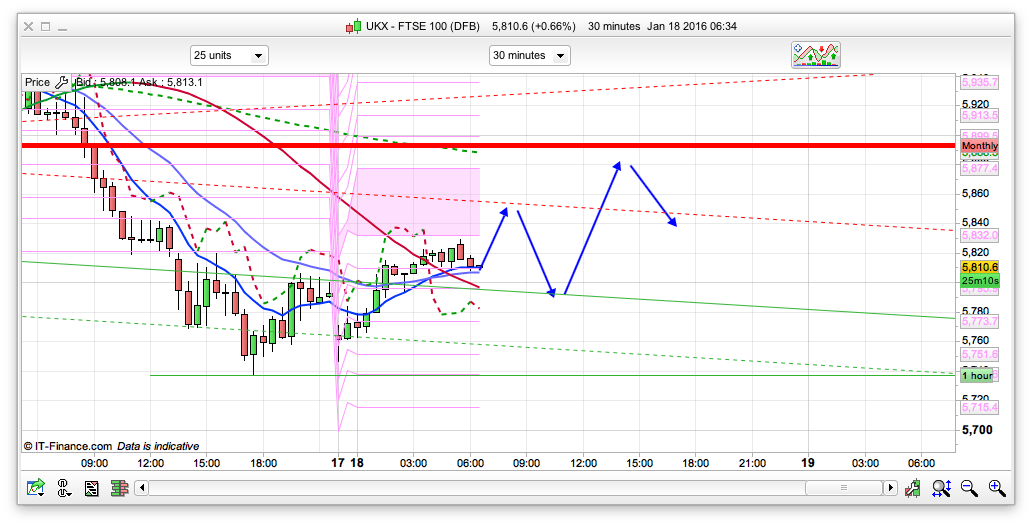

FTSE Outlook and Prediction

The US markets are closed today for Martin Luther King day, and “normally” you would expect a fairly flat day. However, with the volatility the way it’s been we will probably get a 100 point range today! We tested the 5740 level on Sunday night out of hours open, and again have bounced back and are just nudging above 5800 as I am writing this. I expect that the rise will continue first thing as the 10min and 30min chart do have bullish moving averages, with support around the 5810 area on both. The daily pivot is 5841 and I expect this will be the first test of the bulls momentum and we may well get a bit of a dip from here if we get the early rise. Above this then 5865 is the 100 Hull moving average resistance on the 2 hour chart – so later on this might have moved down to 5860ish, so a short from around this area could be worth doing, for a pullback to 5800ish. If the bulls manages to break that 5860 area then the top of the 10 day Bianca is 5927. I am actually feeling fairly optimistic now we have twice tested the 5740 level and bounced up, and I feel that buying the dips is wise for the rest of January. If 5740 breaks though then I accept I am wrong and we have further downside sub 5700.