Good morning. The main features of yesterdays trading were the GDP figure from China which was broadly inline with expectations and the signal that the BOE would not be raising interest rates soon. Both conspired to push the FT100 higher in morning pulling in some buyers and breaking the 5900 level. Our short at 5888 kicked in and narrowly avoided being stopped out which was lucky and then benefitted from the 50 point fall. As has been seen a few times now the Wall Street open was more negative than expected and so the FT100 fell in the afternoon to see the 5805 level mentioned in the email. This was caused by a fall in crude prices which fell below the $30 level again. We got the bounce here at 5800 to 5850 but it has now fallen away again overnight, with Japan officially entering a bear market as well, and we are at 5750 to start off today. Interesting times!

US & Asia Overnight from Bloomberg

Asian stocks resumed declines as Japanese equities retreated and a gauge of energy shares traded near its lowest since 2008.

The MSCI Asia Pacific Index slid 0.2 percent to 119.61 as of 9:02 a.m. in Tokyo, after climbing 0.8 percent on Tuesday to pare the measure’s 2016 slump to 9.2 percent. While Brent crude rebounded, U.S. oil capped a 3.3 percent decline from Friday’s close, hovering just above $28 a barrel as the International Energy Agency fueled concern over the global glut. The 14-day relative strength index for the regional stock gauge, a measure of momentum, traded below the 30 level some traders take as indicating shares will rise.

“We’ll continue to see a tug of war between nervous sentiment and technical indicators showing that falls have gone too far,” said Chihiro Ohta, general manager of investment information at SMBC Nikko Securities Inc. in Tokyo. “At the root of the selling we’ve seen this year has been the imbalance of oil supply and demand, so until the oil price moves calm down, the stock market will struggle.”

Japan’s Topix index lost 0.7 percent, led by energy explorers and oil and coal producers. Bank of Japan officials are increasingly expressing disappointment at subdued annual wage talks, said people familiar with the discussions, making next week’s monetary-policy decision a closer call.

Australia’s S&P/ASX 200 Index lost 0.1 percent, with BHP Billiton Ltd. falling 1.5 percent after trimming its full-year iron ore forecast. New Zealand’s benchmark gauge added 0.2 percent, while the Kospi index slipped 0.5 percent in Seoul.

Consumer discretionary, material and energy shares led losses on the regional benchmark gauge on Wednesday. The MSCI Asia Pacific Energy Index dropped 0.4 percent after a 1.7 percent rebound on Tuesday from the lowest close since 2008.

U.S. Shares

E-mini futures on the Standard & Poor’s 500 Index dropped less than 0.1 percent. The U.S. gauge closed a volatile session little changed, near the lowest level since August, as gains in consumer shares offset declines in commodity companies.

With markets in Hong Kong and China yet to open, futures signaled declines in most recent trading. The Shanghai Composite Index jumped 3.2 percent on Tuesday, the most since November, with Reorient Financial Markets Ltd. saying government-led funds may have entered to bolster the market.

Data on Tuesday showed China’s economic growth missed analysts’ estimates last quarter, while industrial production, retail sales and fixed-asset investment all slowed at the end of the year. The government may further ease monetary policy, such as by cutting interest rates or lenders’ reserve-requirement ratios, according to Northeast Securities Co. and Central China Securities Co.

After the close, China’s securities regulator said it allowed seven companies to move forward with initial public offerings, the first time since a new system for IPOs started at the beginning of the year. [Bloomberg]

FTSE Outlook and Prediction

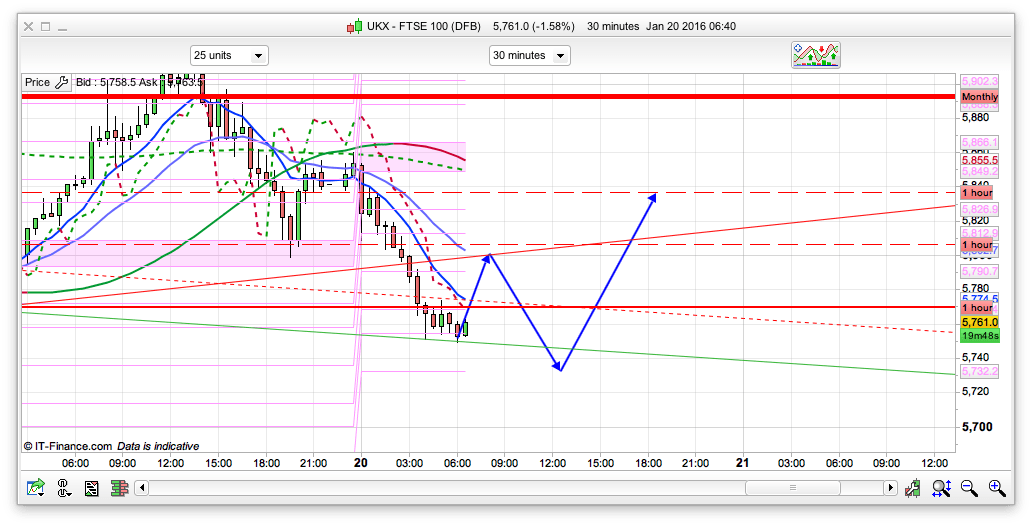

It’s not a good sign for the bulls in the short term that they were not able to hold onto the bounce from 5800 last night. It managed to get as high as 5860 before the bears took over and the weak Asian session dragged it down. We have the 5740 recent low in the cross hairs again now, but with a fib pivot support at 5733 might see a bit of a bounce here. The bulls really need something like oil to bottom out to stop the rout though there doesn’t appear to be much sign of that at the moment. However, we have Draghi speaking tomorrow which may well be a stimulus to prop up the markets/stop the falls so bear that in mind and we may see a bit of stabilisation this afternoon. Could do with another “we will do whatever it takes” speech. I have sort of plotted that with the arrows – a rise from the bottom of this 30min channel at the 5750 level to test the 5800 (yesterdays lower support, and now resistance on the 2 hour chart) before further downside this afternoon. One of the reasons I am expecting the sell off to reverse is that gold has stayed below the 1100 level – as its typically a safe haven (though admittedly less correlated recently) I would have expected that to climb a bit higher during last night Asian decline. So for today, looking at it remaining weak, with eyes on 5733 to see what it does there.