Good morning. Well a nice rise yesterday from the 6760 area though I must admit it looked a little dicey with that stop hunt down to 6752, but it finally rose to 6800. The bulls didn’t really build on that rise, though the bears didn’t really do anything either, probably watching the S&P to see if it broke the 2124 resistance area I suspect (it didn’t). Greece looks like its out the headlines now till September, having had enough money thrown at them to tide them over. Generally the Greek China storm has passed for the moment and there is a bit of optimism around. Fickle things markets!

US & Asia Overnight from Bloomberg

Asian stocks headed for the biggest weekly gain since April as the increased likelihood of an end to Greece’s debt crisis bolstered global equities.

The MSCI Asia Pacific Index traded little changed at 144.32 as of 9:03 a.m. in Tokyo, heading for a 2.3 percent advance this week. The Standard & Poor’s 500 Index added 0.8 percent on Thursday, while the Stoxx Europe 600 Index increased 1.4 percent for a seventh day of gains after Greece’s parliament approved bailout measures and the European Central Bank boosted emergency aid. The Shanghai Composite Index closed 0.5 percent higher.

“China worries have died down and Greece is now a non-issue, until September anyway,” said Evan Lucas, Melbourne-based market strategist at LG Ltd. “These points currently give me reason to be more optimistic.”

ECB President Mario Draghi sought to draw a line under the Greek crisis Thursday, confirming the nation’s place in the euro, as the central bank decided to raise funding to its lenders by 900 million euros ($979 million). He also said that Europe’s economic pickup is proceeding and increased uncertainty in financial markets isn’t hindering a broadening of that recovery.

Japan’s Topix index was little changed and Australia’s S&P/ASX 200 Index advanced 0.1 percent. New Zealand’s NZX 50 Index gained 0.3 percent and South Korea’s Kospi index rose 0.4 percent. Futures on Hong Kong’s Hang Seng Index climbed 0.5 percent in most recent trading and contracts on the Hang Seng China Enterprises Index rose 0.7 percent.

E-minis on the S&P 500 were little changed. American investors turned to the raft of earnings reports for clues on the health of the world’s largest economy. Netflix Inc. climbed to a record after reporting a jump in subscribers, while Citigroup Inc. and EBay Inc. advanced after disclosing results. [Ref]

FTSE Outlook

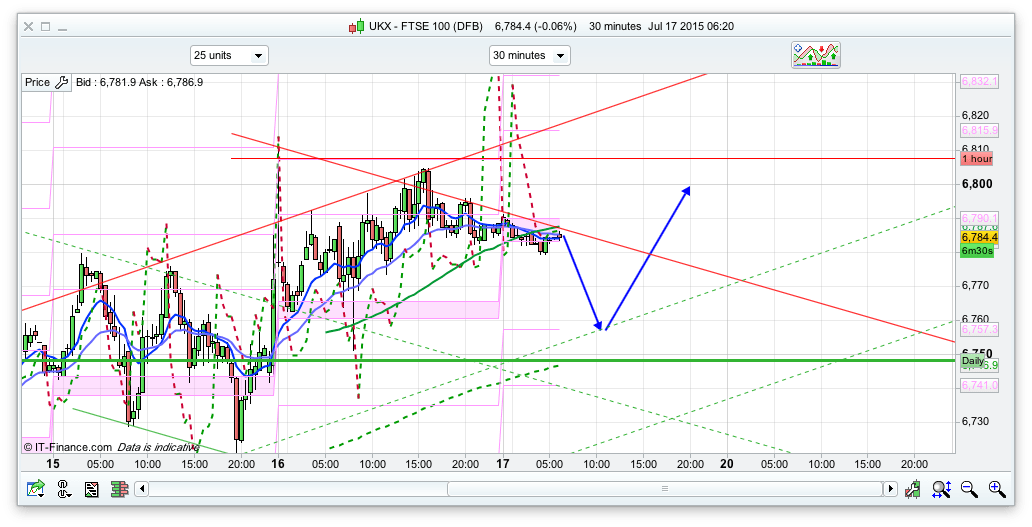

I am thinking we will get a dip and rise today, maybe dipping down to the 6750ish area where we have the 200ema on the 30min, and also the first support from that 30min channel. If that breaks then a dip dow to 6700 is likely, where we have the bottom of the 10 day Raff and the 25ema on the daily chart, we also have the bottom of the 10 day Bianca at 6687 so bear that in mind.The pivot is 6783 for initial support and we are just hovering around this area as I write this (and pretty much been around this area overnight) so it will be an interning open. If the pivot holds then a rise to 6800 is probably going to be first up rather than a drop through the pivot. Either way, I am looking to buy the dips at the moment. I did read yesterday that if the S&P can hold above 2122 then we could be on for a pretty decent rise.

Resistance wise, we have yesterdays high at 6808 then 6859 above that for the top of the 20 day Bianca channel. Not totally sure we will get that high today but you never know. I think the 30min channel looks good for trading off today – resistance at 6825ish and support 6755ish (possibly 6730ish).