FTSE 1o0 Support 6731 6700 6680 6679 6632

FTSE 100 Resistance 6735 6742 6768 6773 6844

Good morning. It was a shame that the early morning short order for 6792 just missed yesterday (high was 6786) as it fell to just below 6700. The bulls fought back from 6690 though to manage 6760 before another leg down. As I expect you know we have the Italian referendum on Sunday so its a bit choppy ahead of that, as well as NFP today. Will Italy vote to leave the Euro as well? Iff they do is it the beginning of the end for the Eurozone? Gold advanced from its lows ahead of the uncertainty – its really taken a bit of a pasting lately, down to 1160 yesterday. For the FTSE 100 6680 is looking key today. If that breaks then a big drop is on the cards, while if it holds then we could be on for a decent climb.

US & Asia Overnight from Bloomberg

- Payrolls, Italy vote weigh on dollar, buoying yen, rand

- Bonds extend selloff as OPEC deal keeps U.S. oil near $51

The Trump rally is running out of steam as fresh concerns over the outlook for the U.S. and stability in Europe weigh on the dollar and global equities.

The Bloomberg Dollar Spot Index headed for its first weekly drop since Donald Trump’s election, as billionaire bond-fund manager Bill Gross said investors betting on a windfall from the president-elect are misguided, with any benefits from increased stimulus likely to be temporary. A selloff in technology shares flowed into Asia, driving declines in Japan, Australia and South Korea.

The yen extended its rebound against the greenback amid caution ahead of key American jobs data, Italy’s weekend referendum and Austria’s presidential vote. Gold rallied while bonds in Australia and New Zealand extended their slide as U.S. oil stayed near $51 following OPEC’s deal to cut output.

Developed-market stocks are also on track for their first weekly retreat since the U.S. vote, amid a let up in support for so-called reflation trades, which gained ground as Trump’s victory burnished the U.S. economic outlook and helped odds on an interest-rate hike this month to 100 percent. Italy’s referendum on reducing the power of the Senate is also weighing on risk sentiment, given a win for ‘No’ could result in the government’s ouster.

“Markets have rallied pretty strongly and we had three fantastic weeks but buying pressure certainly looks exhausted,” James Woods, global investment analyst at Rivkin Securities in Sydney said by phone. “We will see some corrective declines and profit taking. And from a technical perspective, allowing momentum indicators to unwind before gains can be sustained.”

As well as the U.S. nonfarm payrolls report, Friday brings updates on Australian retail sales and Thai foreign reserves.

Stocks

More than twice as many stocks fell as advanced on the MSCI Asia Pacific Index as of 1:39 p.m. Tokyo time, with Japan’s Topix index slipping 0.7 percent and the Kospi index down 0.7 percent in South Korea.

Technology and property shares led a 0.9 percent decline in Australia’s S&P/ASX 200 Index, while New Zealand’s S&P/NZX 50 Index was down 0.4 percent.

Hong Kong’s Hang Seng Index slid 1.2 percent and the Shanghai Composite Index fell 0.8 percent.

S&P 500 Index futures dropped 0.2 percent after the underlying benchmark lost 0.4 percent Thursday, retreating for the third time in four days after ending last week at a record high.

Technology shares extended their declines since the American election, with the Nasdaq Composite Index down 1.4 percent Thursday amid concern over Trump’s trade policy and as investors rotated out of one of the year’s most favored investment sectors.

The Philadelphia Semiconductor Index dropped 4.9 percent last session, the most since Britain voted to leave the European Union.

Currencies

The yen edged up 0.2 percent to 113.85 per dollar, after Thursday’s 0.3 percent gain, trimming its drop in the week to 0.6 percent.

The euro was up 0.2 percent at $1.0683 after climbing 0.7 percent in the previous session.

Korea’s won dropped 0.4 percent while the South African rand climbed 0.3 percent.

Bloomberg’s dollar gauge, which tracks the greenback against 10 major peers, was down 0.1 percent Friday, heading for a 0.4 percent loss for the week.

The MACD, or short-term moving average line, on the dollar index is poised to fall below the so-called signal line as the gauge heads for its first weekly drop since vote. That indicates bears may be taking control of the trade unless a strong jobs report revives the dollar’s rally.

Bonds

Australian government debt due in a decade yielded 2.85 percent, up another seven basis points Friday, headed for their highest closing level since January, while yields on similar maturity New Zealand notes rose by six basis points to 3.28 percent.

Ten-year Treasury yields dropped by two basis points to 2.43 percent after increasing by seven basis points to their highest close since July 2015 on Thursday.

Economists predict an 180,000-worker increase in U.S. November payrolls, after they climbed by 161,000 in October.

The Bloomberg Barclays Global Aggregate Total Return Index of bonds fell 4 percent in November, its biggest decline since the index was started in 1990.

Commodities

While West Texas Intermediate crude slipped 0.8 percent to $50.67 a barrel, it’s headed for a 10 percent rally this week.

The Organization of Petroleum Exporting Countries’ three largest producers — Saudi Arabia, Iraq and Iran — overcame disagreements to reach Wednesday’s deal in a bid to drain record global stockpiles and boost crude prices. Russia committed to cooperate with the group by curbing production next year.

Gold for immediate delivery gained 0.4 percent to $1,176.30 an ounce, halting a three-day drop to trim its weekly retreat to 0.8 percent, the fourth straight decline.

Copper futures in London fell for a second session, slipping 0.8 percent.

[Bloomberg]

FTSE 100 Outlook and Prediction

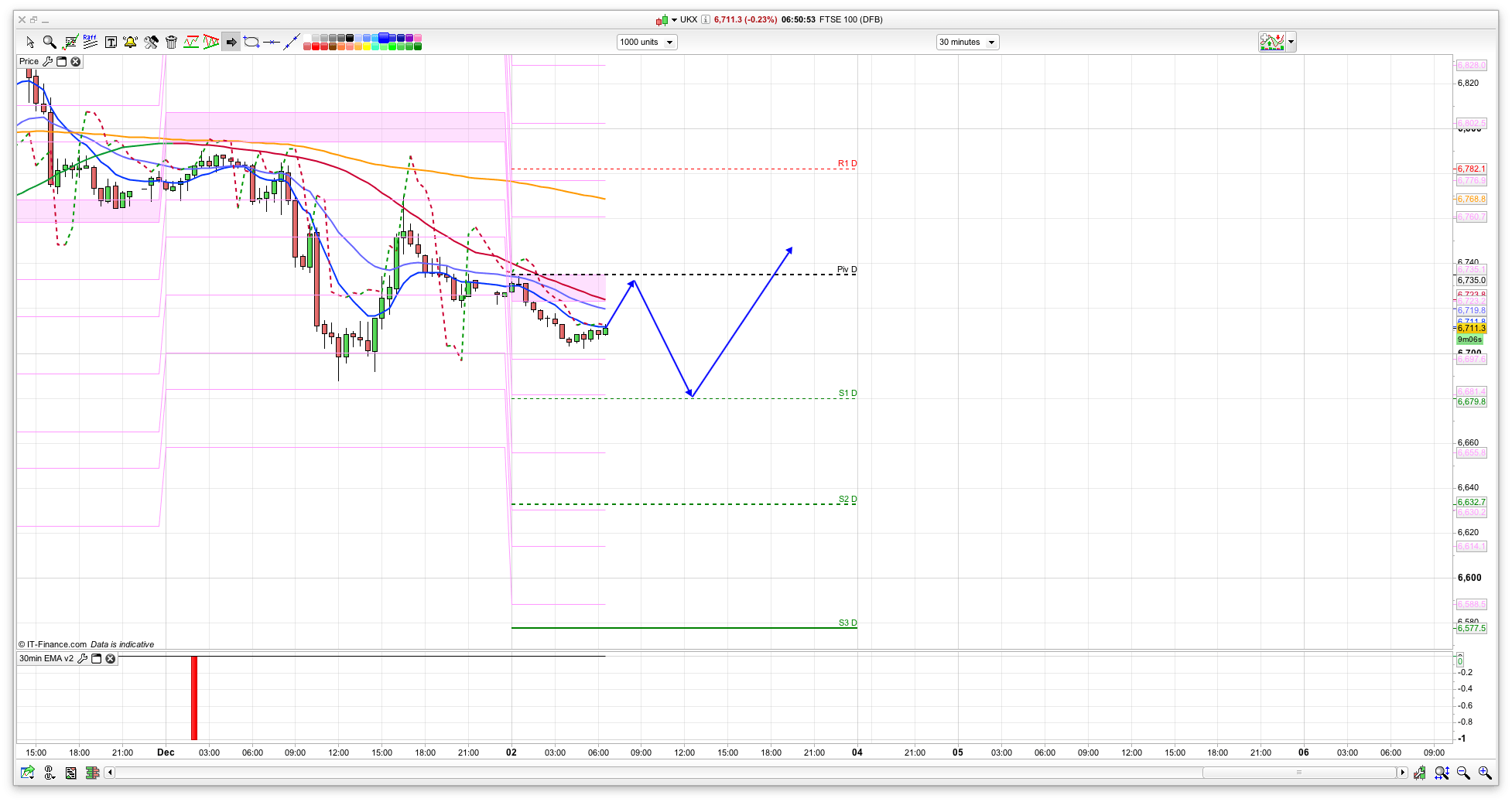

As its NFP Friday before another referendum vote, I’m taking it a bit easier today in terms of the trade plan orders. As mentioned above 6680 looks pretty key and while yesterday I was all for shorting the rallies, today I am being a bit more cautious. We dropped off well from the late rally to 6760, and I think we will test 6680 this morning. If that holds then a rise to the pivot and possibly higher is likely. However, if it breaks (and the fairly tight stop gets hit) then flip to short as its likely to fall fairly significantly.

It looks bearish to start with on the 10 min chart which is why I am thinking that we will get an initial drop towards the 6680 level. If we do then really its all eyes on 6680 and what happens here so this is a really key level. Below this then 6632 is S2 and the 200ema on the daily, but I expect the bears will have a fair bit of momentum behind them by that stage. The bottom of the 20 day Raff is down at 6500 – so this is the sort of area I am thinking that we would fall too, if the 10 day breaks. If indices do fall then it should see a climb on gold – purely as a safety play really, though admittedly they are not as correlated as they used to be.

So, thats my plan really – watch 6680 in the main and see what happens there.

Selling pressure on the FTSE its down 1% the DOW has hardly moved.. If that sells off we could see further decline..

Is anybody on the Long on Dax?

yes, had a couple of longs today:

10435 to 10455

10410 to 10440

Long on FTSE at 6680 now

Cool entry on FTSE!

Taken some off at 6705

I had one long from 10.30 at 10427 to 10440th, took profits in stages. The last one closed at 11.32

It was a counter trend but I hoped it would break up so I asked.

Expect falls as the pound rises to 1.29 and the oil price nonsense returns to reality. The 6660 level now waits merely to confirm the lack of support and the real target here folks is 6500. Whatever the catalyst this index will drop faster than 3 tenors in a lift and set up easy entries for the december rally nonsense in 3 weeks. Sell your worldly goods and fill your xmas stockings with short orders.

Oh dear, I was hoping for 10460 at least, dax.

all right, got 20 points and happy.

Nice double bottom missed on Dax.

FTSE looking very bullish at the moment…