FTSE 100 Support 6886 6886 6837 6833 6825 6816 6772

FTSE 100 Resistance 6940 6943 6974 6984 7005 7027

Good morning. Well that was certainly bullish yesterday with the only area for a slight pullback being the 6890 area, when it dropped down to 6864, however the third test of the 6890 level broke and the bulls pushed on to 6940. Was expecting a climb but not quite like that! The 6680 level other day where we went long has proven to be a rather good support level! The rise all to do with the (yet again!) expectation of further economic stimulus measures, as we have the ECB early this afternoon (12:45) with Draghi expected to prolong the asset buying program.The bank stocks also rallied amid Monte dei Paschi rescue reports in Italy, which helped the general bullish sentiment. If in doubt throw money at the problem! Its eyes on the Fed as well about US interest rate rises and will they hike next week? Odds are at 100% that they will. We also have US unemployment claims data due out at 13:30.

US & Asia Overnight from Bloomberg

Fresh U.S. equity records ignited Asian markets, with benchmarks from Tokyo to Sydney and Mumbai extending gains as bond yields declined before policy decisions from the world’s two biggest central banks.

The MSCI Asia-Pacific Index of stocks rose to its most in more than a month as banks drove Australia’s S&P/ASX 200 Index to its highest level since August and SoftBank’s second day of gains led a jump in Japanese shares. The euro and the yen extended gains with gold before Thursday’s European Central Bank meeting, amid mounting speculation policy makers will prolong their asset-buying program. The New Zealand dollar and South Korea’s won strengthened. Yields on Australian bonds fell to their lowest this month amid a debt rally across developed markets. Oil held near $50 a barrel after a surge in U.S. stockpiles.Expectations ECB chief Mario Draghi will prolong the bank’s 80 billion euros ($86 billion) a month of bond purchases beyond March provided a shot in the arm for U.S. equities, which had been struggling to extend the rally ignited by Donald Trump’s unexpected election win a month ago. Both the S&P 500 Index and the Dow Jones Industrial Average rose to records Wednesday. Odds on the Federal Reserve hiking interest next week remain at 100 percent, according to Fed funds futures.

Globally, “we’re seeing a euphoric state continue, and investors will also be heading into the Christmas break soon, so we’re seeing some final moves to get into the market or close off positions,” said Ayako Sera, a Tokyo-based market strategist at Sumitomo Mitsui Trust Bank Ltd. “We’re also seeing gains from expectations on ECB’s moves to ease.”

As well as the ECB review, markets will be digesting an update on Chinese trade data, while Bank of Japan Governor Haruhiko Kuroda will speak at a party for economists. Final third-quarter data showed Japan’s economy expanded less than was projected, growing an annualized 1.3 percent after economists predicted a rate of 2.3 percent.

Stocks

The MSCI Asia Pacific Index climbed 1.2 percent as of 1 p.m. Tokyo time, rising for a third day as Japan’s Topix index gained 0.9 percent.

SoftBank jumped to levels unseen in two years, heading for a 12 percent advance this week, as Chairman Masayoshi Son’s meeting with President-elect Donald trump is seen benefiting the company’s businesses, which include Sprint.

Banks and mining companies drove the S&P/ASX 200 up 1.2 percent in Sydney, set for its highest close since Aug. 24. India’s S&P BSE Sensex rose more than 1 percent, led by Tata Motors Ltd. and Infosys Ltd.

The Hang Seng Index in Hong Kong climbed 0.7 percent; gauges in mainland China were little changed.

S&P 500 Index futures were up less than 0.1 percent at 2,231.25.

Telephone and property stocks drove the S&P 500 to its new all-time high Wednesday, with health-care shares the only decliners among 10 industry groups after President-elect Trump said that he opposed high drug prices.

Currencies

The euro advanced 0.2 percent at $1.0777 after rising 0.3 percent last session, while the yen appreciated 0.4 percent to 113.28 per dollar, heading for a second day of gains.

The kiwi climbed 0.7 percent, touching an almost four-week high, as Reserve Bank of New Zealand Governor Graeme Wheeler said he was likely done with rate cuts and the government raised growth projections.

The won added 0.8 percent, rising for a third day.

The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, retreated 0.2 percent and has swung between gains and losses all week.

Bonds

Australian 10-year bonds led the advance in Asia, with yields falling by seven basis points, or 0.07 percentage point, to 2.73 percent.

Similar maturity New Zealand debt yielded 3.18 percent, down five basis points.

Yields on Treasuries due in a decade held at 2.34 percent after falling five basis points on Wednesday.

Commodities

West Texas Intermediate crude edged up by 0.3 percent to $49.90 a barrel after sliding 2.3 percent last session.

Oil supplies at Cushing, Oklahoma, the biggest U.S. storage hub, climbed by the most since 2009 last week, fueling concern that American shale producers will fill the gap created by the OPEC-led deal to curb output.

Gold for immediate delivery rose 0.4 percent to $1,178.36 an ounce after gaining 0.4 percent on Wednesday.

Nickel rose 0.4 percent to $11,450 a metric ton on the London Metal Exchange.

[Bloomberg]

FTSE 100 Outlook and Prediction

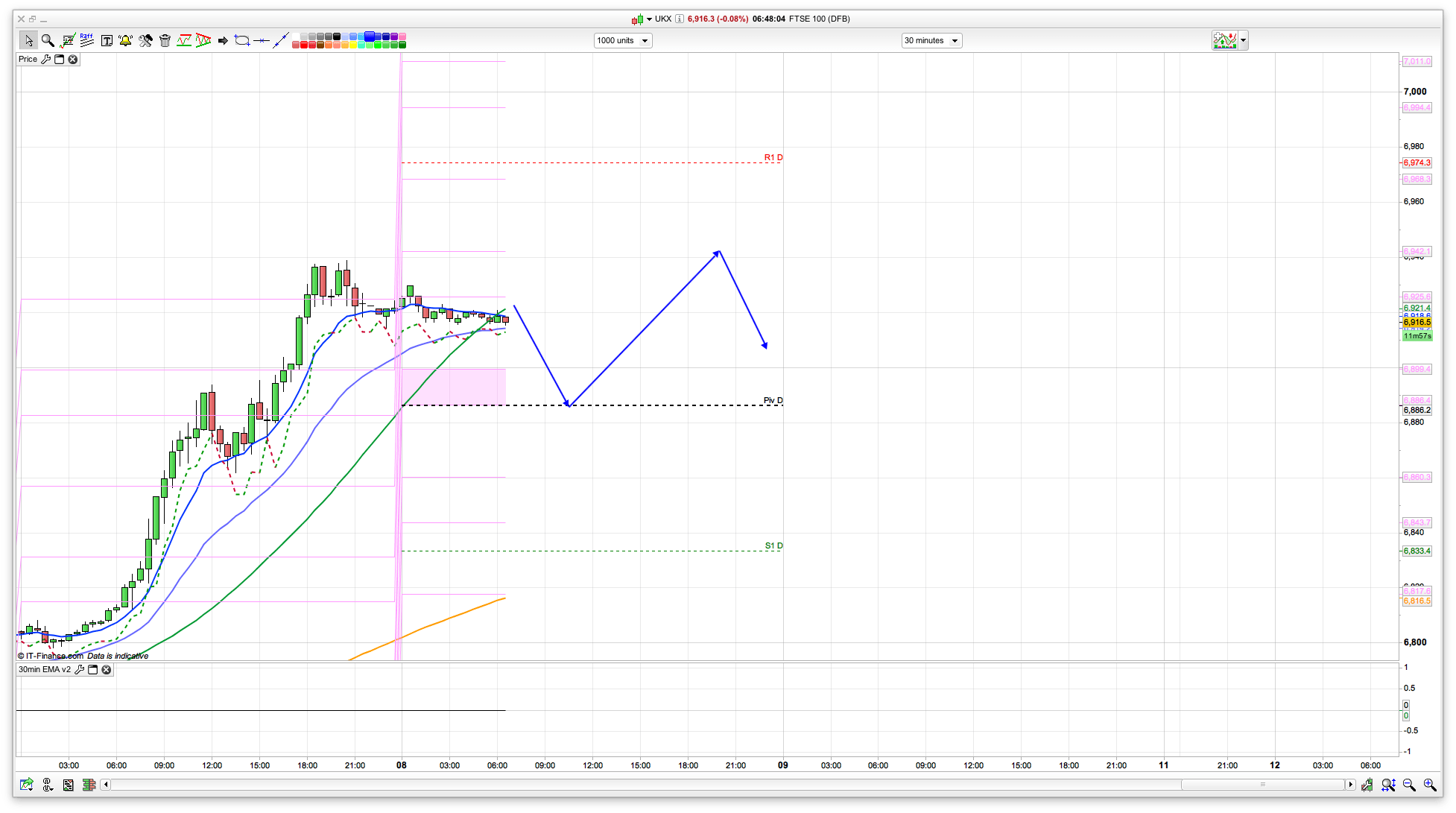

Today its all on the ECB later at 12:45 and what stimulus measures are ahead – prolonging the asset buying program or not. Along with this we have the rate decision, expected to stay at 0%. We also have US news at 13:30 with unemployment claims, forecasted to be 255k versus 268k previously. After the strong rise yesterday we may well have a period of consolidation while we await this news, then some volatility and then more flat this afternoon. The levels that I am watching at 6886 for initial support where we have the daily pivot, and a back test of the top of the Bianca channels here. Below that then 6836 is the next support area I am looking at, with 6772 even lower down. Would have to be a pretty bearish day (unlikely) to reach that today though). Worth longs off these levels (go with the trend and all that!).

For resistance we have 6942 initially, where we have the top of the 10 day Raff and also the overnight high. Above that then 6974 and 7006for the top of the 10 day Raff. The bulls will be keen to keep the momentum going and head for the 7000 level I expect, though with the US starting to make record highs then that usually only lasts for a little while before the inevitable pull back. I still think that there is more trouble around the corner despite this equity rises. A view reinforced by the need for the ECB to extend the asset purchases program! Still, trade what you see, not what you think.

Longs around the 6890 level look good

Am long on Dax at 11007 as well

A bit of weakness kicking in, it seems.

Really not sure at the moment.

Shorted S&P at 2242 and slowly moving down. Bears are running scared though I think. Singed fur from yesterday!