Good morning. Nice long from 6732 yesterday that kept going, helped by the hopes of, finally, a Greek deal. European stocks rose the most in a month, snapping a six-day losing streak, amid investor optimism. Shares extended gains after people familiar with Germany’s position said it may be satisfied with Greece committing to at least one economic reform sought by creditors to open the door to bailout funds. Prime Minister Alexis Tsipras aims to meet Chancellor Angela Merkel and French President Francois Hollande on the sidelines of a summit in Brussels.

Greece pulled back on budget concessions in new proposals Tuesday, after last week rejecting terms and deferring a payment to the International Monetary Fund. The ASE Index slid 1.1 percent today, for the worst performance among western-European markets. “European stocks should rebound after we get through this,” said Lars Kreckel, Legal & General Investment Management’s global-equity strategist in London. “There was a very strong consensus that Europe was the best place to be and positioning was crowded. In that kind of context, some disappointments can lead to a bit of a pullback — the Greek situation is getting a bit closer to crunch time and that made people nervous.”

US & Asia Overnight from Bloomberg

Asian stocks rose for a second day, following U.S. shares higher amid optimism progress is being made in Greece’s debt talks.

The MSCI Asia Pacific Index gained 0.4 percent to 147.54 as of 9:07 a.m. in Tokyo. Speculation increased that the standoff over Greece will reach a favorable resolution as the European Central Bank raised the level of emergency cash available to the country’s banks by 2.3 billion euros ($2.6 billion). German Chancellor Angela Merkel said Wednesday her goal is “to keep Greece in the euro area.” The Standard & Poor’s 500 Index jumped the most in a month.

“We’re coming to a stage where a decision has to be made on Greece,” Matthew Sherwood, head of investment markets research at Perpetual Ltd. in Sydney, which manages about $21 billion, said by phone. “Markets are on edge, hoping that some stop-gap measure could be agreed. We could see a continued selloff in equities if Greece defaults.”

Germany may be satisfied with Greece committing to at least one economic reform sought by creditors to open the door to bailout funds, according to two people familiar with the country’s position. A government spokesman later denied that Germany is considering such a deal.

Japan’s Topix index gained 1.1 percent. Shares rose even after the yen jumped 1.4 percent against the dollar on Wednesday as central-bank chief Haruhiko Kuroda suggested further yen weakness is unlikely. The currency slid 0.2 percent to 122.93 against the greenback today.

Rate Cut

New Zealand’s NZX 50 Index jumped 1 percent. The nation’s lowered interest rates for the first time in four years and signaled another cut may be appropriate to boost inflation as growth slows.

South Korea’s Kospi index climbed 0.5 percent. Australia’s S&P/ASX 200 Index added 0.7 percent. Markets in China and Hong Kong have yet to open. Reports on China’s retail sales and industrial production for May are due Thursday.

The Shanghai Composite Index slipped 0.2 percent on Wednesday after swinging between a loss of as much as 2.2 percent and a gain of 1 percent. MSCI said mainland Chinese stocks will probably be added to its indexes once market access issues are resolved, deferring a move that could lure billions of dollars to the world’s best-performing market.

E-mini futures on the S&P 500 lost 0.1 percent today after the underlying equity index climbed 1.2 percent on Wednesday. [Ref]

FTSE Outlook

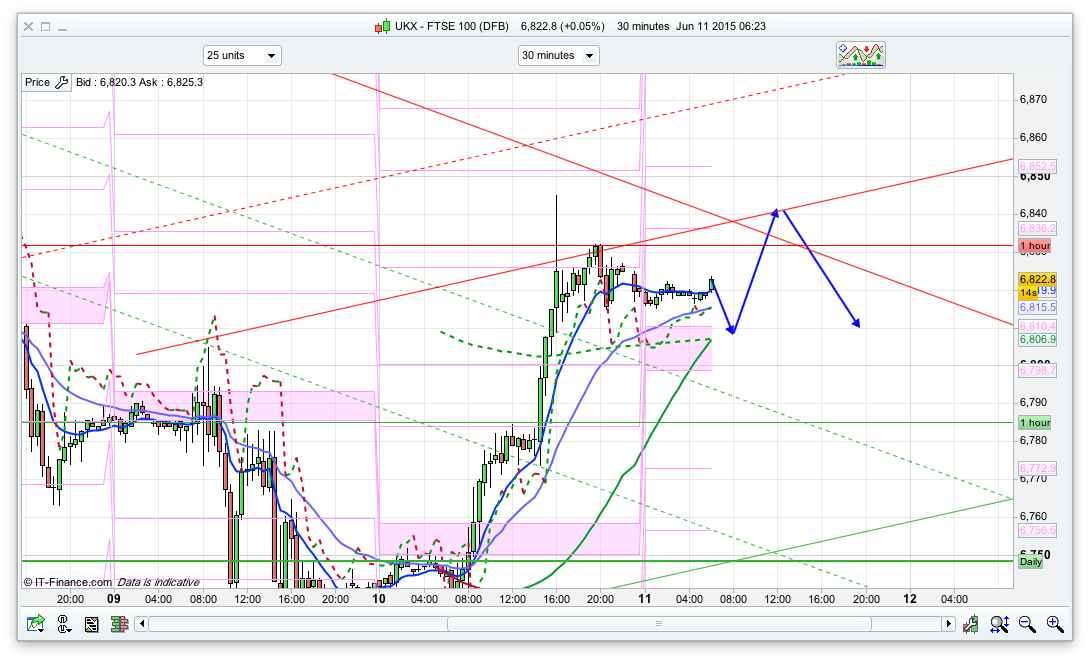

The market breathed a large sigh of relief that there might be a resolution (maybe only a short term one though?) for the current Greek debacle with yesterdays rally. Fortunate timing as we were testing the bottom of the Bianca channel (hence the long at 6732) and had very low RSIs on the daily – purely a coincidence of course! The markets needed to bounce before they could go any lower just to move out of those oversold conditions. As such, I don’t think we are at this point heading onwards and upwards and that they may in fact be a larger decline to come during the summer. Anyway, for today, the pivot is 6798 so support there, though there is also a back test of the 10 day Bianca channel at 6813 likely to occur first. The moving averages are all positive for some more upside from here, though there is resistance at 6839 looking at the 30min channel, with a fib at 6853 above that, with the extreme top of the channel at 6872. I don’t think we will be testing the top of the 20 day Bianca at 6955 today though, but back on the daily there is 25ema and 20day Raff resistance at 6912 – a level thats worth a swing short if seen.

I have plotted an initial dip down to the 200ema on 30min area at 6810 before a bit more upside – the market is probably quite relieved so unlikely to sell off just yet – and a rise to 6850ish. Once more detail emerges the rise might slow down though. In the US today we have the release of US Retail Sales, weekly jobs report and business inventories.