Good morning. The FTSE traded strongly to the upside after the BOE meeting implied UK interest rates would be on hold for longer than expected. In the afternoon however Wall Street pulled the FTSE100 back on stronger dollar concerns and interest rate worries for the US. This impacted oils, commodities and some banks. An added concern was the US non farm payroll figures which are due today triggering some profit taking after the recent rises.

US & Asia Overnight from Bloomberg

Most Asian stocks advanced as investors awaited U.S. jobs data to gauge whether the economy is strong enough to withstand the first Federal Reserve interest-rate increase in almost a decade.

About three shares rose for every two that fell on the MSCI Asia Pacific Index, which traded little changed at 134.81 as of 9:01 a.m. in Tokyo. Economists expect the October jobs report Friday to show an increase of 185,000 non-farm workers, compared with a 142,000 gain the previous month. Federal Reserve officials from Chair Janet Yellen to Atlanta chief Dennis Lockhart underlined this week that the central bank is still data dependent. The prospect of higher U.S. borrowing costs this year has muddied the rally in global stocks from last quarter’s selloff, with central banks in Japan and the euro area remaining coy over whether they’ll bolster stimulus.

“The market is on tenterhooks ahead of the U.S.. non-farm payrolls,” Angus Nicholson, an analyst at IG Markets Ltd. in Melbourne, said by phone. “U.S. data has been somewhat mixed but the market has been responding more strongly to the Fed statements this week that they could hike rates this year.”

Japan’s Topix index added 0.3 percent as the yen held four days of losses against the dollar. South Korea’s Kospi index slipped 0.2 percent. Australia’s S&P/ASX 200 Index fell 0.6 percent. New Zealand’s S&P NZX 50 Index was little changed. Markets in China and Hong Kong have yet to start trading.

China Shares

China’s Shanghai Composite Index gained 1.8 percent to 3,522.82 on Thursday, taking its advance from its Aug. 26 low to more than 20 percent and entering a bull market. The government took extreme measures to shore up equities as a boom turned to bust in June, including banning major stockholders from selling shares, curbing short selling and directing state funds to purchase equities. Margin debt is also rising and trading volumes have stabilized. The Hang Seng China Enterprises Index of mainland stocks in Hong Kong added 0.5 percent on Thursday.

“Perhaps some healthy gains could continue until the Shanghai index reaches the 4,000 level,” IG’s Nicholson said. “There should be quite a lot of positive economic data coming out of China as we go into the fourth quarter because there has been a significant amount of monetary easing.”

E-mini futures on the Standard & Poor’s 500 Index lost 0.1 percent on Friday. The underlying U.S. equity gauge slipped 0.1 percent on Thursday as investors weighed the outlook for interest rates and the economy. Traders are predicting a 56 percent chance the Fed will raise rates at the December meeting. [Bloomberg]

FTSE Outlook

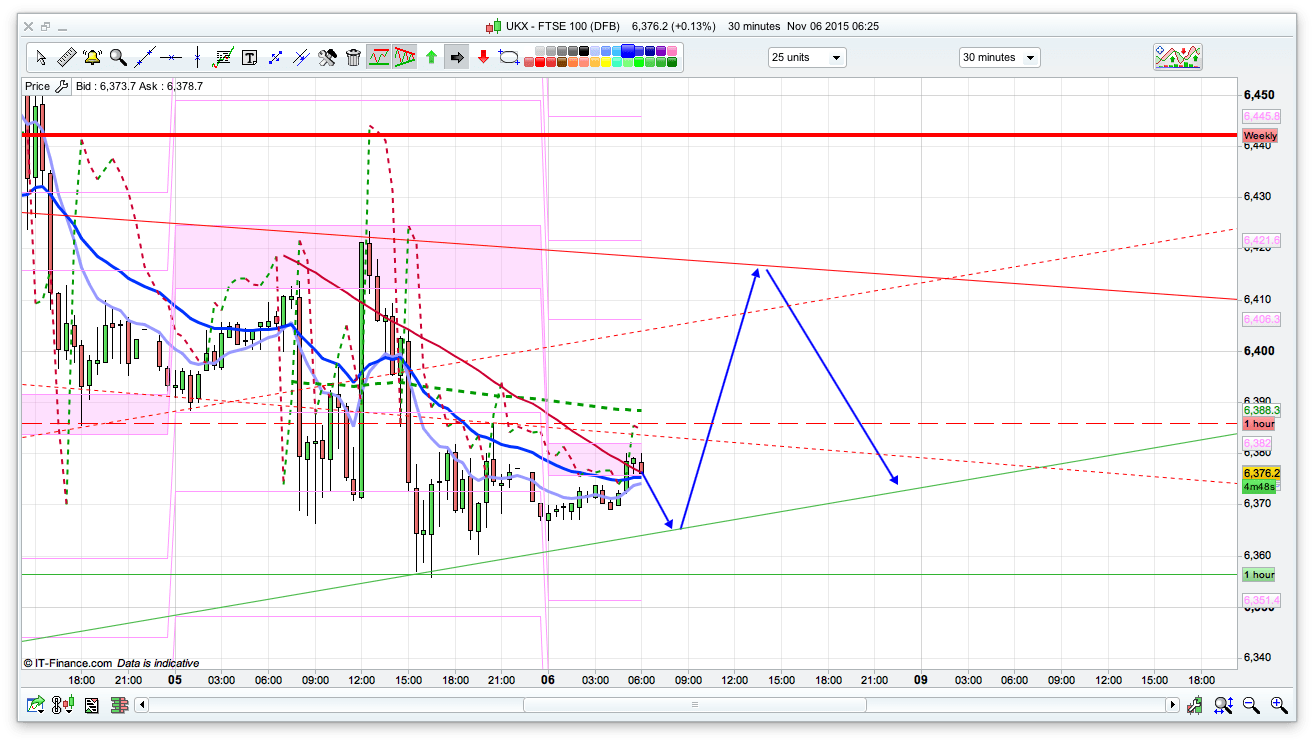

It’s NFP Friday today with the news due out at 13:30 and forecasted at 184k versus 142k previously. As such we may well see a bit of buy the rumour, sell the news today. I have plotted that accordingly for the prediction with a short off the top of the 10 day Bianca at the 6419 area. We also have the top of a declining PRT channel line at 6415 so this area is worth a small short. Support wise, we have the 6355 area as decent support from a rising PRT line, and yesterdays low at 6353. Initially the bulls need to break the daily pivot at 6382 to push up to the higher resistance levels, so longing a break of that will be worth trying, otherwise if it dips down to the 6360 area a long here. Stay nimble today!