Support 6139 6131 6129 6109 6113 6060 6038

Resistance 6155 6170 6181 6206 6243

Good morning.

Market Summary for Friday 11th March 2016

The markets kicked backed in style on Friday after the massive whipsaw moves on Thursday.

The main focus was bank shares which outperformed on plans for a new round of cheap funding.

With a test of the 6000 area tested with a spike down on the spread bet markets it appears that could be the base for a move up now.

Considering the large intraday moves it is interesting that the FT100 settled at 6139 which is near the middle of the longer term interday range of 6100-6200 showing that markets do like to revert to mean.

Unsurprisingly banks and financials were the best sector gainer with gold shares the main losers as the metal tends to be contra-cyclic.

US & Asia Overnight from Bloomberg

- Aussie rises to eight-month high as copper, gold advance

- U.S. crude oil retreats as Iran plans to boost production

A global stocks rally gathered momentum in Asia, South Korea’s won strengthened and copper rose as a surge in Japanese machinery orders buoyed risk appetite before central banks in two of the world’s three biggest economies review policy this week.

The MSCI Asia Pacific Index climbed to a two-month high, led by banking shares, after the Standard & Poor’s 500 Index erased its loss for the year on Friday. The Shanghai Composite Index rallied after the new head of the securities regulator signaled he will maintain state support for Chinese equities. The won was headed for its strongest close of the year versus the dollar and Australia’s dollar rose to levels last seen in July. Copper exceeded $5,000 a metric ton for the first time in a week, while U.S. crude oil retreated from a three-month high as Iran reiterated plans to boost output.

Central banks are being relied on to revive the global economy after a worsening growth outlook wiped almost $9 trillion off the value of equities worldwide this year through mid-February. The bulk of the stock-market losses have been clawed back, helped by monetary easing in China and last week’s announcement of unprecedented stimulus by the European Central Bank. The Bank of Japan will conclude a policy review on Tuesday and a Federal Reserve meeting ends Wednesday.

“Central banks are going to be dominating market sentiment,” Matthew Sherwood, head of investment strategy at Perpetual Ltd. in Sydney, which manages about $21 billion, told Bloomberg Radio. “That could be enough for the risk rally to continue, but I think it is starting to run out of steam. The Fed is going to be front and center” this week, he said.

Japan’s central bank will keep the annual expansion of the monetary base at 80 trillion yen ($702 billion), according to 35 of 40 economists surveyed by Bloomberg. All but two predict the policy rate will remain at minus 0.1 percent. Fed funds futures indicate there’s only a 4 percent chance the Fed will hike borrowing costs this week, down from 12 percent at the start of this month. In China, central bank Governor Zhou Xiaochuan said “excessive” stimulus wouldn’t be required to achieve the nation’s economic growth goal of at least 6.5 percent over the next five years.

Stocks

The MSCI Asia Pacific Index climbed 1.1 percent as of 1:49 p.m. Tokyo time, set for its highest close since Jan. 5. Japan’s Topix added 1.6 percent as data showed machine orders jumped 15 percent in January from a month earlier, beating December’s 4.2 percent increase and higher than economist forecasts for a 1.9 percent gain.

“The machine orders results should be a boost to stocks,” said Masaaki Yamaguchi, a Tokyo-based equity market strategist at Nomura Holdings Inc. “It’s not just this one indicator that’s moving the market, but globally we’re moving toward a more risk-on stance.”

The Shanghai Composite Index rallied 2.7 percent, its biggest gain in more than a week. Liu Shiyu, chairman of the China Securities Regulatory Commission, said it was too early to think about the state rescue fund leaving the market and vowed to step in “decisively” if needed to curb panic. China Vanke Co. jumped 13 percent in Hong Kong, the most since 2014, after saying it plans to pay as much as 60 billion yuan ($9.2 billion) for a stake in Shenzhen’s urban transit company.

Futures on the S&P 500 Index were little changed, after the benchmark surged 1.6 percent on Friday to cap a fourth straight weekly advance.

Currencies

The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, fell for a fourth day and was headed for its lowest close since October. The won strengthened 0.7 percent to 1,184.42 versus the greenback.

“Risk-off sentiment continues to be damped, which leads to a steady won,” said Masashi Murata, a vice president at Brown Brothers Harriman & Co. in Tokyo.

Australia’s dollar appreciated 0.2 percent to 75.82 U.S. cents, extending this month’s advance to 6.2 percent. It earlier weakened as much as 0.3 percent after Chinese industrial output and retail sales data over the weekend added to signs of a slowdown in the world’s most-populous nation. The yuan fell 0.11 percent in Hong Kong’s offshore market and was little changed in Shanghai.

Turkey’s lira snapped a four-day advance after a suicide car bomb in Ankara killed at least 34 people, the capital’s third attack in five months.

Commodities

Copper rose as much as 1.2 percent to $5,030 a metric ton in London, rebounding from earlier losses amid speculation Chinese demand will strengthen. The nation’s National Development and Reform Commission said Monday it approved 15 fixed-asset investment projects in February totaling 34.1 billion yuan ($5.3 billion).

Gold gained 0.4 percent, after retreating 1.8 percent on Friday. The precious metal has surged 19 percent so far this year, on pace for the biggest quarterly gain since 1986, and is far from being out of favor. Money managers are holding the biggest net-long position in gold futures and options in more than a year, according to Commodity Futures Trading Commission data.

In the oil market, West Texas Intermediate crude futures declined 0.2 percent to $38.41 a barrel following four straight weeks of gains. Iran plans to boost output to 4 million barrels a day before it will consider joining other suppliers in seeking ways to rebalance the global crude market, Oil Minister Bijan Zanganeh said, according to the Iranian Students News Agency.

Bonds

Benchmark Treasuries were little changed Monday, with the 10-year yield at 1.98 percent. Morgan Stanley forecast the rate will fall to 1.45 percent by the end of September, approaching the record low of 1.38 percent set in 2012, and said the Fed will wait until December before raising interest rates. The U.S. bank also cut its end-2016 projection to 1.75 percent and lowered forecasts for yields on similar-maturity debt issued by Germany, Japan and the U.K., according to a report released on Sunday.

The cost of insuring Asian corporate and sovereign bonds against default fell four basis points to 135 basis points, according to prices from Nomura Holdings Inc. The benchmark is set for the lowest close in more than two months, CMA data show. [Bloomberg]

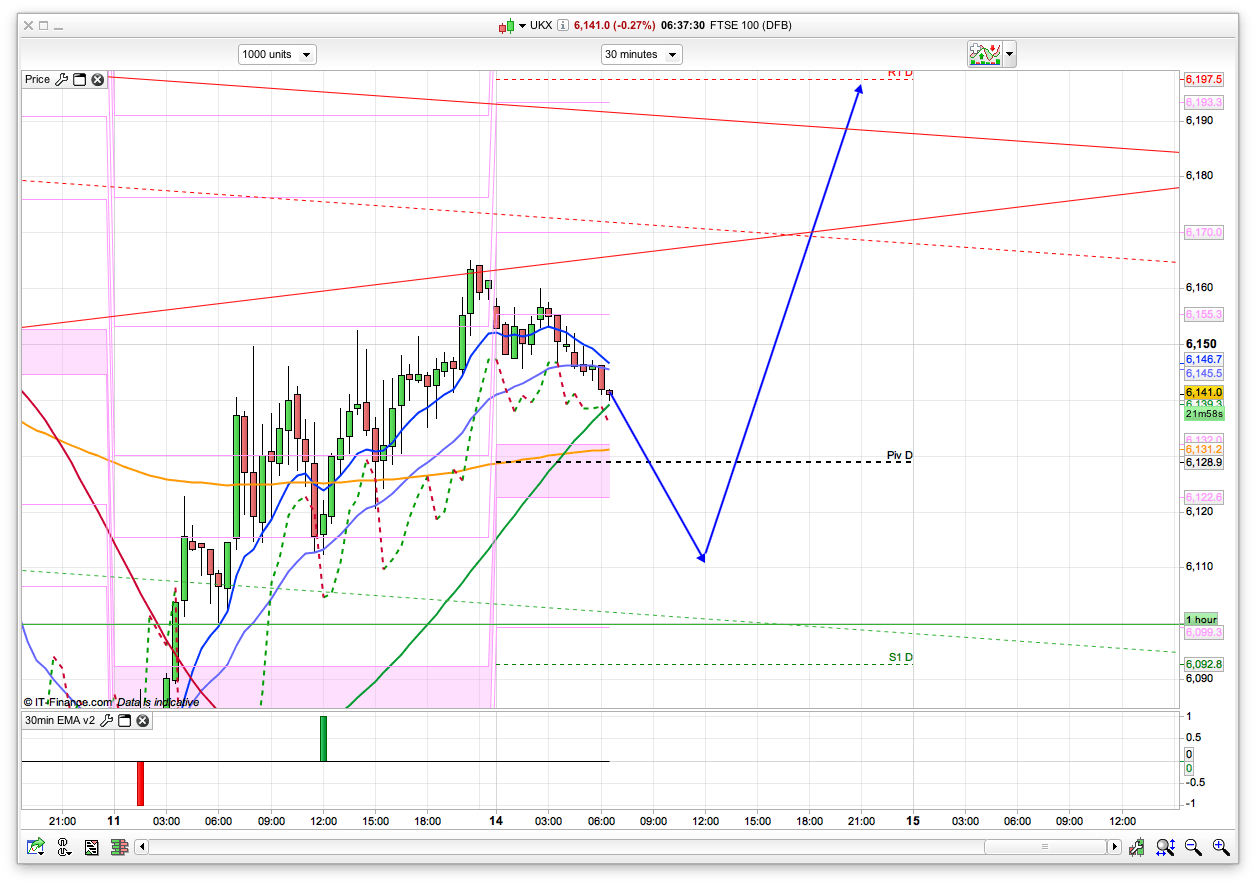

FTSE 100 Outlook and Prediction

It’s looking a little tricky to call first thing today to be frank, as we have had a few things happen over the weekend that could be negative – further terrorist attacks (one in Turkey and one in Ivory Coast) and also Angela Merkel suffering regional election losses, probably as a backlash against the “open-door” stance on refugees. Mrs Merkel’s Christian Democrat party (CDU) was beaten in its stronghold of Baden-Württemberg for the first time in more than 50 years, according to exit polls. All of which could lead to a negative start for the Dax, and also the FTSE, this morning. The 10min chart is certainly bearish to start off with, whilst the 2 hour chart has support at 6113 following Fridays recovery after Thursday’s volatile session. So, if that level holds then we could spring up from there to test the top of the 10 day Bianca channel at 6206. There is some initial support on the 30min chart at the 6130/6140 area, though we are right on them as I write so haven’t given them too much weight to start with, but bear them in mind. The live charts pivot is 6109, and as that is close to my 2 hour support I have favoured a long from this area today for a rise to 6181, and possibly 6200.