Good morning, well the stalemate in the US continues which has put the brakes on Fridays rally – purely driven by hope that a deal was going to be done on Saturday. As you would expect on still no deal, futures prices gapped down on Sunday night with the FTSE dropping 60 from its 6530 high seen at close. It all doesn’t bode well for the second part of this financial time bomb, as the debt ceiling will be hit on the 17th October. China and a few other US debt owning nations are probably getting rather frustrated/worried! Talking of China, their latest news was that exports unexpectedly fell, while food prices rose, also fuelling the bearish scenario.

This from the Telegraph explains it pretty well – “There are two parts to the current episode. The first is the shutdown of large parts of the American government because of Congress’s failure to pass a Budget. The second is its refusal to raise the debt ceiling. Congress regularly reviews the ceiling and usually increases it without incident, thereby allowing the US Treasury to go on borrowing. But this is what the Republican majority in the House of Representatives has been refusing to do now as they are in a dispute with the Democrats (and President Obama) over a healthcare bill popularly known as Obamacare.”

The US situation will be the main focus this week I imagine and if a deal is done then we, based on Fridays movements, get a decent rally. However, the longer it drags on the more bearish it will be. To be honest it looks like markets are fairly certain a deal will be done, its just a question of when.

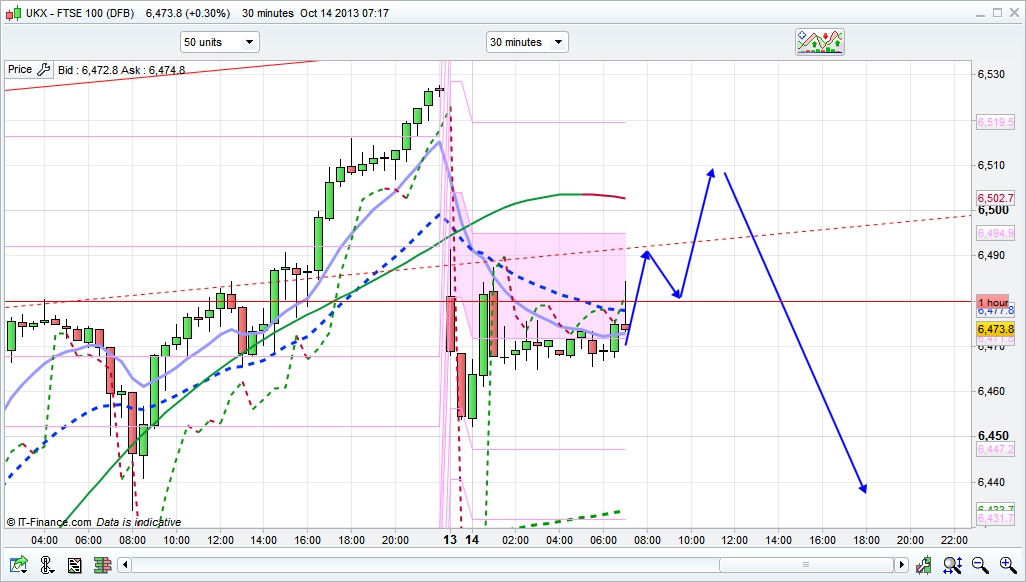

I mentioned 6509 as a decent shorting point on Friday, however, whilst stalling there initially, prices went a bit higher on the hope of a debt solution, but have since fallen back to 6470 at the time of writing. I did have a short there but got stopped out at 6520 (kept it tight as it was Friday, and didn’t fancy holding over the weekend in case a deal was done), however if still holding from there then it looks like it should do well early this week.

Asia Overnight from Bloomberg

Asian stocks and U.S. index futures fell, while the yen snapped a four-day slump as American lawmakers struggled to reach an accord on raising the nation’s debt limit and restoring government operations. Industrial metals dropped after Chinese exports unexpectedly decreased.

With the U.S.’s borrowing authority set to lapse Oct. 17, the Senate wrapped up almost four hours of debate in Washington without unveiling a deal. China’s exports unexpectedly fell in September and inflation jumped on food prices, signaling constraints on the nation’s recovery as Premier Li Keqiang seeks to sustain growth without adding monetary stimulus. India today may report benchmark wholesale-price inflation was at 6 percent in September, compared with 6.1 percent a month earlier.

“There was no miracle deal done over the weekend in Washington, and investors were hoping by Monday morning things would be clearer and we could think about something else for a change,” said Richard Sichel, the chief investment officer at Philadelphia Trust Co., where he helps oversee $1.9 billion. “Instead, the debt ceiling is there, and all those headlines get in the way of looking at fundamentals.”

FTSE Outlook

Its going to be all eyes on the US this week and any hope of a resolution should see a climb. However, for today the futures have found support around the daily pivot area at 6468 though 6489 could be a stumbling block on any rises, as well as that 6509 level which is still on the radar, and likely to be hit if 6489 breaks. Support is pretty close at 6434 though, being the 200ema and a break of that could see us testing the bottom of the Raff 10 day at 6315 fairly quickly. I am thinking the bulls will try and keep Friday’s bullish momentum going but probably won’t have much luck past 6509. Unless some deal is suddenly reached today and then it could break that resistance and head for 6600. We are still above the Bianca 10 and 20 day channels hence why I have a slightly bearish overtone.