Good morning, hope you had a good weekend. Not looking like a great start to the week with the FTSE just above 6400 as I write this, off the back off the Chinese Manufacturing data last night, reaching a 3 month low (50.5 versus 50.9 estimate). Of course, the big even for this week is the Fed meeting tomorrow and Wednesday which should provide some clarity on when they will taper. That’s what everyone’s expecting anyway. I think though they will reiterate that it will be when data warrants it, rather than a set date at this stage as economies are still fragile, as shown by the Chinese data. Would be a shame to withdraw QE too early and put the brakes on any sort of vital signs in the economy. At least with prices on the FTSE now nearly at the 6400 level (an area that I had from ages ago as older members will know, as a potential bounce point) we could see the start of the climb around about now. Interestingly all 3 Bianca channels have met at this area as well. I’d go so far as to say that no immediate tapering could kick start that Santa Rally and we still get the 6800 year end close, provided 6400 holds.

Asia Overnight from Bloomberg

Asian stocks fell for a fourth day, poised for a three-month low, after a gauge of Chinese manufacturing fell and as investors awaited a Federal Reserve meeting starting tomorrow to gauge the timing of stimulus cuts.

The MSCI Asia Pacific Index lost 0.6 percent to 137.15 as of 2:05 p.m. in Hong Kong, heading for its lowest close since Sept. 13. The measure dropped 1.1 percent last week, a second week of declines, as improving U.S. economic data spurred bets stimulus will be reduced. The Fed will start paring $85 billion of monthly bond purchases this week, according to 34 percent of economists surveyed Dec. 6 by Bloomberg. Futures on the Standard & Poor’s 500 Index slid 0.5 percent today.

“The market is very divided on whether the Fed will announce any changes,” Stewart Richardson, who helps oversee about $100 million as chief investment officer at RMG Wealth Management LLP in London, said in an e-mail. “Equity markets seem to be behaving a little more bearishly in the run-up to this meeting compared to September.”

Manufacturing Data

The HSBC Holdings Plc/Markit Economics preliminary manufacturing purchasing managers’ index for China fell to 50.5 in December, missing the 50.9 estimate in a Bloomberg survey after coming in at 50.8 in November. Readings above 50 signal expansion. The data may signal pressure to support short-term growth as President Xi Jinpoing rolls out reforms to sustain momentum for the rest of the decade.

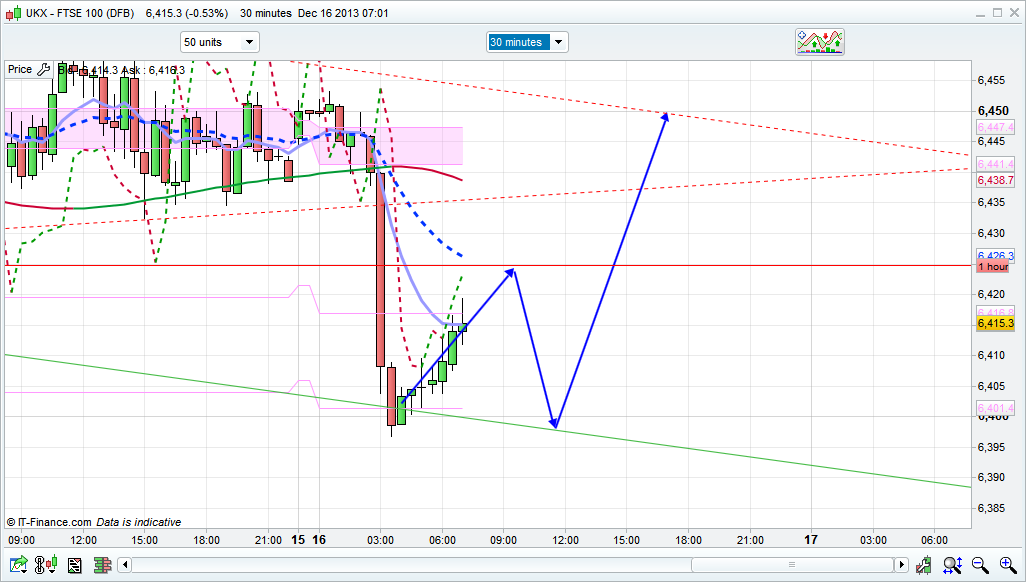

FTSE Outlook

No significant rally is likely to kick in pre Fed meeting I wouldn’t expect (though as we know, always expect the unexpected!) however 6400 presents a decent buying level I feel for a possible swing trade to hold till the end of the month. All 3 Bianca channels are there, I had 6400 in my mind from way back for a decline too (not actually thinking we would see it though I admit, once prices hit 6800 in October) and I do still think we won’t have tapering for a few months yet, and its still only a possible anyway as its data dependant.

Today’s pivot is 6445 so will be an initial resistance level that will need to be overcome. Immediate term this current bounce off 6400 I think might struggle at 6425ish which is where there is a ProTrend lien and also the 2 EMAs on the 30minute.