Support 6131 6107 6098 6082 6066

Resistance 6152 6173 6180 6182 6248

Good morning.

Market Summary for 7th March 2016

The markets were relatively quiet today with little news until Thursday’s FED meeting.

There was a quick spike up at the open taking the FT100 above 6200 which appeared to be short stop “take out”.

The market then slipped through the day until the Wall Street open which saw renewed buying on a spike up in oil and commodity prices.

The FT100 closed just down by 17 points at 6182 having been down to around 6130 earlier in the day.

Best sector was commodities and the weakest gold. This pattern is seen a “risk on” play favoured by economic growth.

Dax and S&P trades worked well yesterday and while the FTSE followed the arrows with rise, dip, rise, the levels exceeded the stop orders so the early short was stopped on the spike.

US & Asia Overnight from Bloomberg

- Crude slips from this year’s high as copper, nickel drop

- U.S., Japan government bonds advance as Aussie, won weaken

Asian stocks dropped the most in about three weeks, oil fell and South Korea’s won weakened as data showed Japan’s economy and Chinese exports are shrinking. The yen gained with U.S. Treasuries on demand for haven assets.

Equities benchmarks retreated across most of Asia, while U.S. and U.K. stock index futures declined. Brent crude fell, after closing on Monday above $40 a barrel for the first time this year, as nickel led losses in industrial metals and iron ore tumbled. Australia’s dollar weakened with South Korea’s won, while the yen gained ground against all 31 major peers. Gold traded near a 13-month high as Japan’s 10-year bond yield sank to a record.

Sustained demand for precious metals and sovereign debt highlights a lack of confidence in rebounds in global stocks and commodities that took hold over the last three weeks, adding $4.6 trillion to the value of equities worldwide. Goldman Sachs Group Inc. recommends betting on declines in copper and aluminum prices, while Citigroup Inc. said it’s still bearish on iron ore. Japan announced on Tuesday a drop in fourth-quarter gross domestic product and China reported the biggest tumble in exports in almost six years.

“While there’s a likelihood of a pullback in the short term, investors should use this as an opportunity to buy into value plays,” said Nader Naeimi, Sydney-based head of dynamic markets at AMP Capital Investors Ltd., which oversees about $115 billion. “The tail risk from China continues to reduce. It’s quite clear that they are pretty keen to stabilize growth. That’s positive for commodities, emerging markets and global growth.”

The European Central Bank is widely expected to deliver a package of easing measures at a March 10 policy meeting to revive euro-area growth and inflation. China’s leaders are setting out economic plans at an annual meeting of the legislature and have already agreed to target a record-high budget deficit this year to support growth.

Stocks

The MSCI Asia Pacific Index fell 0.7 percent as of 1:44 p.m. Tokyo time, retreating from near a two-month high. Japan’s Topix dropped 0.8 percent, the Shanghai Composite Index slid 1.6 percent and Hong Kong’s Hang Seng Index declined 0.9 percent.

Japan’s economy contracted an annualized 1.1 percent last quarter, and while the drop was less than analysts predicted it underscored growing concern over Prime Minister Shinzo Abe’s reflation program. China’s exports tumbled 25.4 percent from a year earlier in dollar terms in February as imports fell for the 16th month in a row.

“The exports data are very, very poor,” said Castor Pang, head of research with Core-Pacific Yamaichi Hong Kong. “The huge decline doesn’t auger well for the stock market.”

Standard & Poor’s 500 Index futures slipped 0.4 percent, while contracts on the U.K.’s FTSE 100 Index declined 0.7 percent.

Currencies

The yen strengthened 0.3 percent versus the dollar, gaining for a second day. China’s yuan climbed 0.17 percent as the central bank raised its daily reference rate for the currency following Monday data showing a slide in the nation’s foreign-exchange reserves moderated in February. The Australian and New Zealand dollars fell 0.4 percent, while South Korea’s won weakened 0.3 percent.

Commodities

Iron-ore futures on the Singapore Exchange fell 6.3 percent to $54.94 a metric ton. Citigroup said it’s still bearish as supply and demand fundamentals remain weak, while Axiom Capital Management Inc. said the price jump was probably just a “blip”.

Copper fell 1.3 percent in London, trimming this month’s advance to 5.1 percent. Nickel slid 3.1 percent, retreating from its highest close since November, and aluminum lost 0.6 percent. Goldman Sachs Group Inc. reiterated its view that the structural drivers for last year’s slump in industrial metals prices remain intact, predicting drops of as much as 20 percent for copper and aluminum over the next 12 months.

Gold was little changed at $1,266.71 an ounce, after recording its highest close in more than a year on Monday. The precious metal last week entered a bull market — commonly defined as a 20 percent advance from the most recent low — and platinum and palladium followed suit on Monday. Platinum retreated 0.2 percent on Tuesday, while palladium dropped 1 percent.

Brent crude fell 1 percent in London to $40.22 a barrel, after surging 5.5 percent on Monday. It’s advanced more than 40 percent since slumping to a 12-year low in January amid speculation a proposal by major producers to freeze production will trim a global glut. Data on Wednesday is forecast to show U.S. stockpiles increased last week to the highest level since 1930.

Bonds

The yield on 10-year U.S. Treasuries fell three basis points to 1.88 percent, retreating from a one-month high. The rate on similar-maturity Japanese debt dropped as much as four basis points to an unprecedented minus 0.085 percent. The Asian nation’s government sold 30-year securities with a record-low 0.8 percent coupon on Tuesday. [Bloomberg]

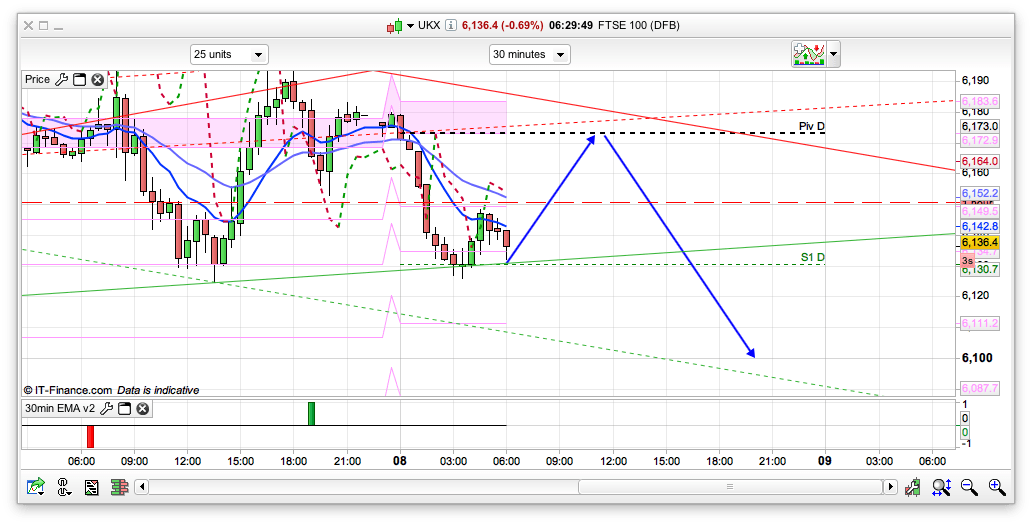

FTSE 100 Outlook and Prediction

The bulls haven’t been able to hold above 6200 so far despite a couple of attempts, and also despite the expected stimulus that is coming on Thursday from the ECB to revive euro-area growth. Overnight we have dropped off from the 6180 area on Asia weakness. However, we are sitting on a support area at 6130 as I write this so we may well get a rise towards the pivot at 6173 this morning. The 2 hour chart still looks bearish with the coral T3 trend indicator turning bearish on this current candle, with 6180 as resistance. The 30min chart has resistance slightly lower at 6151, so there are a few hurdles to jump for the bulls if they do manage an early rise. In the trade plan I have put a couple of short trades, you can either do smaller stakes and fade in at those levels with the higher stop or use tight stops and trade off both levels. Generally I think we will see a bit of a dip today, probably down towards the 6098 20 day Bianca channel area. I still think we will see 6000 this week. The daily RSI(10) is highish at 60, but not overbought as such. Generally I am watching that declining 30min channel with the 6180 and 6100 edges and expect the price to stay within that today.