Good morning. The 6932 long on Friday took to gain few more points, hitting the 6958 target in the afternoon. I travelled back to the UK over the weekend so things are back to normal times now with just the jet lag to get over! Anyway, weekend news was mostly the opposition assassination in Russia, while it looks like Greece will meet the conditions neccessary to resolve its debt crisis. Interesting looking Bianca chart as the 10 day channel continues to narrow, so expecting a break out either from he 6939 support, or the 6985 resistance soon, though it may continue to meander for a little while longer. The U.S. economy grew at an annualized pace of 2.2 percent in the fourth quarter, beating the 2 percent rate predicted by economists, a report on Friday showed. Data on U.S. manufacturing is due today at 15:00. The FTSE divi for this week is expected to be 16.2 so should get the divi hunters out just before the bell on Wednesday.

US & Asia Overnight from Bloomberg

(Bloomberg) — The dollar rallied with gold as the yuan slipped to a two-year low after China cut interest rates for the second time in three months. Oil retreated following its first monthly gain since June.

The Bloomberg Dollar Spot Index increased 0.2 percent at 1:22 p.m. in Hong Kong as China’s currency traded at its weakest level since October 2012 and the euro slipped 0.2 percent. Gold climbed 0.7 percent. The Hang Seng Index and Shanghai Composite Index advanced, while contracts on the Standard & Poor’s 500 Index added 0.1 percent. Oil in New York and London dropped at least 0.6 percent after OPEC output exceeded its quota for a ninth month in February.

China’s second rate cut in 14 weeks was the latest in a wave of global easing that underscores diverging economic outlooks for the U.S. versus the rest of the world. A private measure of factory activity in Asia’s largest economy showed a faster-than-estimated expansion Monday as lawmakers prepare to meet in Beijing. The euro area updates on consumer prices and U.S. private spending data are due.

“It’s clear markets are being driven by other factors besides earnings, and key is the ongoing loose central-bank policy around the world,” Mark Lister, head of private wealth research at Craigs Investment Partners Ltd., which manages about $7.2 billion, said by phone from Wellington. “China is clearly slowing down, you don’t cut rates twice in three months if things are going stunningly well.”

China Economy

The People’s Bank of China announced a benchmark lending and deposit rate cut of a quarter percentage point Saturday. A day later, a government factory gauge for February signaled contraction for a second month, underscoring the scope for looser policy.

The yuan traded at 6.2732 per dollar after the central bank reduced its reference rate to the weakest since November today. Today’s purchasing managers index from HSBC Holdings Plc and Markit Economics came in at 50.7, beating economists’ estimates for it to hold steady from a preliminary reading of 50.1. Readings above 50 denote expansion.

The Bloomberg gauge of dollar strength traded at 1,174.11, less than one point from its highest level in at least 10 years. The greenback was stronger against 13 of 16 major peers, advancing 0.5 percent against the Australian and New Zealand currencies. The euro bought $1.1179.

Gold for immediate delivery was at $1,220.82 an ounce, the highest level since Feb. 19. Silver increased 0.9 percent to $16.75, while platinum and palladium added 0.2 percent.

Hong Kong

The Hang Seng Index climbed 0.2 percent. Property stocks rebounded after sliding at the close Friday as the Hong Kong Monetary Authority announced extra cooling measures for the city’s real-estate market. The Shanghai Composite was 0.3 percent higher after falling as much as 0.4 percent.

Australia’s S&P/ASX 200 Index advanced 0.5 percent and South Korea’s Kospi index was 0.5 percent higher. Japan’s Topix index climbed 0.1 percent as the yen slipped 0.2 percent to 119.87 per dollar.

Futures on the Nasdaq 100 Index were 0.2 percent higher. The Nasdaq Composite Index on Friday capped its biggest monthly advance since January 2012 after Apple Inc. climbed 9.6 percent during February.

The MSCI All-Country World Index touched a record intraday high Feb. 26, capping its best month since January 2012 as more than $3 trillion was added to the value of global equities.

GDP Beat

The U.S. economy grew at an annualized pace of 2.2 percent in the fourth quarter, beating the 2 percent rate predicted by economists, a report Friday showed. Data on U.S. manufacturing is also due Monday, along with factory gauges for the euro region to India.

West Texas Intermediate crude fell 0.6 percent to $49.43 a barrel. The Organization of Petroleum Exporting Countries pumped 30.6 million barrels a day in February, above the group’s output target of 30 million a day, according to a Bloomberg survey. Brent dropped 0.6 percent to $62.22 a barrel.

WTI jumped 3.3 percent Friday and capped a monthly gain of 3.2 percent amid signs the more-than 50 percent slump in oil prices since June is curbing new drilling in the U.S. The number of crude rigs in service in the U.S. fell to 986 last week, the lowest level since June 2011, according to data from Baker Hughes Inc.

Copper for three-month delivery on the London Metal Exchange rose 0.6 percent to $5,927.50 per tonne. The metal climbed 7.3 percent last month, the most since 2012, amid speculation China — the world’s biggest consumer of industrial metals — would expand stimulus to stoke growth. [Ref]

FTSE Outlook

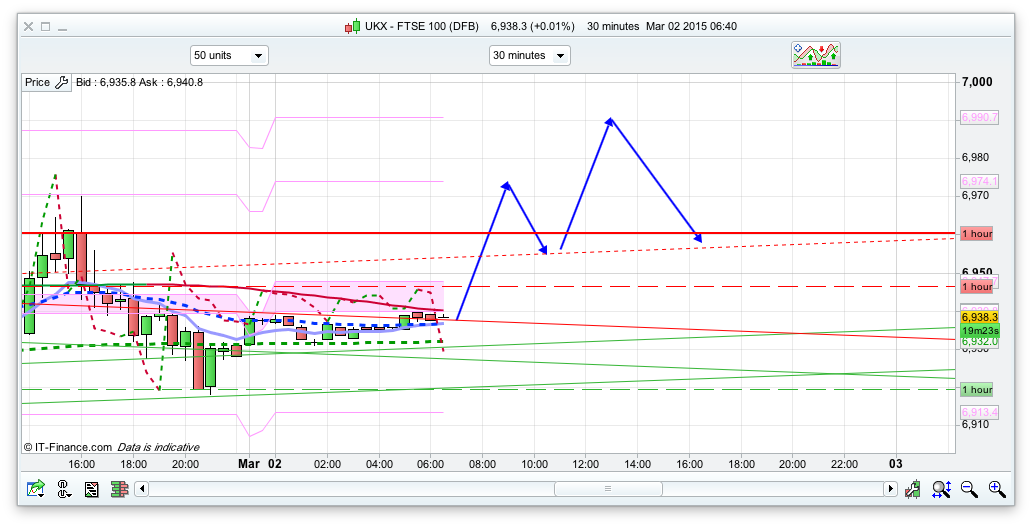

The FTSE looks like its going to open bang on the bottom of the 10 day Bianca channel and previous support at 6939, as well as the IG pivot at this level too. So, the bulls will be keen to charge first thing, and may well be helped by the fact that its the start of a new month so a new influx of cash for the first trading day. However, I am just watching gold at the moment which has continued to rise, possibly in preparation for a downturn in equities – we shall see but be prepared for that. The top of the 10 day Bianca isn’t very far away at 6985, and the 20 day at 6995, so still a couple of resistance levels there and I have plotted a dip from there after an initial rise this morning. Prior to that there is resistance at 6974, so if the bulls do get a rise firth thing, there might well be a little dip from there. The Bianca channels has been working well during February so it will be interesting to see how they perform in March – a short around the 6990 area looks like it could be a decent play today, though it might not have legs for a large drop as the trends are still up. If the 6938 break then the next support is 6924 and then 6897 where we have the bottom of the 20 day Bianca.