Good morning. Well here we go with a new month, this year seems to be zipping by. Focus currently has swung to interest rates and when and who will be raising them first. Yellen is kind of backed into a bit of a corner for a rise next month so we shall see.I imagine the US will raise and then the UK will follow suit. Don’t want to do it too early though as we seem to be having a pre crisis rush for debt with loads of people leveraging themselves up while money is cheap. Lets hope they can sustain it with a 3 or 4% interest rate, otherwise hello recession. Again. Greek markets open today after a 5 week suspension, while talks are still ongoing about the austerity measures and debt relief reforms.

US & Asia Overnight from Bloomberg

Asian stocks fell for the first time in four days as data showed a Chinese factory gauge slipped to a five-month low and energy shares retreated amid a drop in oil.

The MSCI Asia-Pacific Index slipped 0.3 percent to 141.67 as of 9:07 a.m. in Tokyo. The measure lost 0.4 percent last week for a second weekly decline. The official China Purchasing Managers’ Index was 50 in July, compared with the median estimate of 50.1 in a Bloomberg survey and down from June’s 50.2. Energy shares sank as crude futures in New York slid as much as 1.6 percent after Iran claimed it will be able to bolster production a week after sanctions are lifted.

“China will have several hard questions asked of it over the week, feeding into concern it’s facing a hard landing,” Evan Lucas, a markets strategist in Melbourne at IG Ltd., wrote in an e-mail to clients. “We see a slightly negative start to August.”

Japan’s Topix index fell 0.1 percent. More than 70 companies in the nation’s benchmark gauge are scheduled to report earnings today.

Australia’s S&P/ASX 200 Index added 0.1 percent. South Korea’s Kospi index fell 0.4 percent. New Zealand’s NZX 50 Index gains 0.5 percent. Markets in Hong Kong and China are yet to open.

Futures on the FTSE A50 Index of China’s largest companies advanced 0.4 percent in most recent trading. The Shanghai Composite Index resumed a decline last week, tumbling 10 percent after three weekly gains. Most of the loss came on July 27, when the Chinese measure tumbled 8.5 percent for its largest daily slump since 2007.

China, Oil

A final reading of a private gauge of Chinese manufacturing due Monday is expected to show further contraction in the sector.

West Texas Intermediate crude declined as much as 1.6 percent after capping its worst month since 2008 in July amid concern over a global supply glut. Iranian production can increase by 500,000 barrels a day within a week after sanctions end, and by 1 million barrels a day within a month following that, state-run Islamic Republic News Agency said.

E-mini futures on the Standard & Poor’s 500 Index gained 0.1 percent after the underlying equity measure lost 0.2 percent on Friday in New York. [Ref]

FTSE Outlook

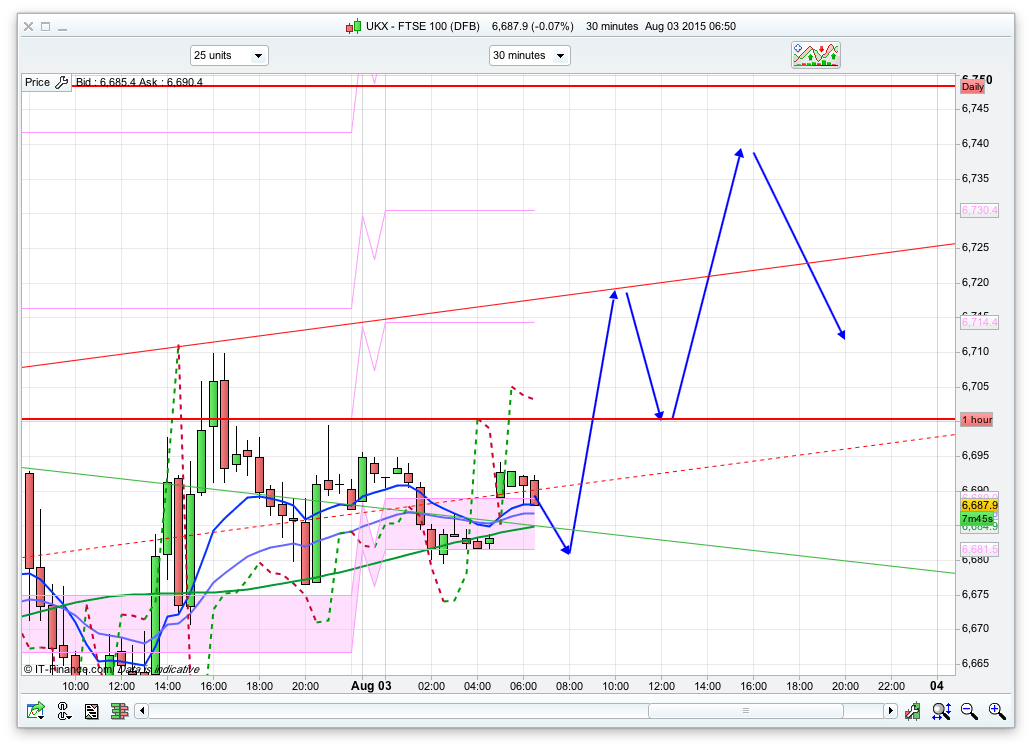

Todays pivot is 6681 and I think that might well hold as support initially. Typical hr start of a new month is fairly bullish as we see a decent amount of buying, certainly first thing. If the pivot does hold then I can see a rise to the top of the 30min channel at 6720, before dropping back. I have put in another leg up though after that to the top for he 10 day Bianca channel at 6740. If we get that high today then a 60 point rise might well be worth a short from that level. Above that there are some daily resistance levels at 6770 and6780. Support wise, below the pivot we have the bottom of that 30min channel and fib 1 at 6655, so this could well be a good place for another long. Generally I think August might be fairly bullish and if so we may even see 7000 again this month. If the 6655 area breaks though then we may follow Australia’s lead and in fact be bearish today.