Good morning. Well the FTSE was pretty resilient yesterday, with hat 6735 short stopping at 6720 (glad we took half of there) and then bouncing to 6765 (shame it didn’t quite reach that 6780 area for the top of the daily channels though). Everything else seemed especially weak, yet the FTSE remained pretty upbeat, even after the bell. Bit odd really! Its NFP Friday once again today, and employers are projected to have added 225,000 workers to payrolls in July after a 223,000 increase the month before, according to the Bloomberg survey median. So far this year, payrolls have grown by an average 208,000 each month. While that’s less than last year’s impressive pace of 260,000, it’s enough to keep reducing labor-market slack. For the Fed, it’s the continuance of that overall trend that matters. Markets, however, are going to be “intensely focused” on whether the data argue for a rate increase sooner or later.

US & Asia Overnight from Bloomberg

Asian stocks fell, following a slide in U.S. equities, ahead of a U.S. jobs report that may cement prospects that the Federal Reserve will raise interest rates as soon as next month.

The MSCI Asia Pacific Index declined 0.2 percent to 140.55 as of 9:01 a.m. in Tokyo. Japan’s Topix index slipped 0.2 percent ahead of a monetary policy decision by the Bank of Japan later today.

The Asia Pacific gauge is heading for a third week of decline before the U.S. government’s payrolls report and amid data Thursday that showed jobless claims near a four-decade low. Traders are pricing in a 48 percent probability that the Fed will raise interest rates in September.

There’s “a cautious tone in risk markets ahead of tonight’s non-farm payrolls,” said Matthew Sherwood, Sydney-based head of investment strategy at Perpetual Ltd., which manages about $22 billion. “Increased concern about what a strong report may mean saw equities out of favor and gold, safe haven currencies and government bonds edge higher.”

E-mini futures on the Standard & Poor’s 500 Index fell 0.1 percent after the underlying gauge on Thursday slid 0.8 percent.

South Korea’s Kospi index declined 0.3 percent and New Zealand’s NZX 50 Index slipped 0.4 percent. Australia’s S&P/ASX 200 Index sank 0.9 percent. Markets in Singapore are closed for a holiday.

Futures on Hong Kong’s Hang Seng Index declined 0.5 percent and contracts on the Hang Seng China Enterprises Index of mainland firms listed in the city slipped 0.5 percent in most recent trading.

In Japan, sixteen of 37 economists forecast the central bank won’t expand monetary stimulus at all, the most popular answer in the survey. Twelve expect the bank to add stimulus at its meeting on Oct. 30, unchanged from last month.[Ref]

FTSE Outlook

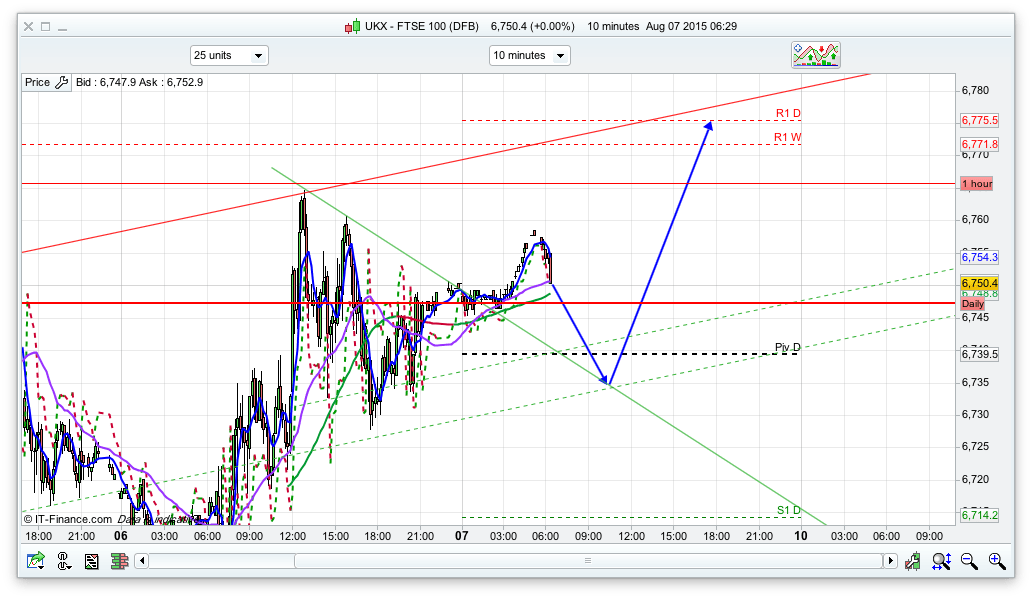

NFP Friday so expect bit of weirdness, especially as the markets will be looking to the result to give as much of a clue as possible for a US rate rise in September. I have put a fairly bullish scenario for today, mainly as there are a cluster of fairly decent supports around the 6740 area, including the daily pivot at 6739.5. However, the sell off in Australia during Friday session does give a little bit of cause for concern as the FTSE has been tracking the ASX fairly well recently. So, if 6740 breaks then a dip down to 6713 is pretty likely where we have the bottom of the 10 day Bianca channel. Below that then the daily chart shows support at 6682, which is a level that is worth a tentative long. A break of this then we will get pretty bearish for a while I think, down to 6400 this month being distinctly possible. Anyway, for today, if the 6740 area holds then we could get a rise to 6770 area where we have a couple of resistance levels. The 30min channel is more optimistic with a channel top at 6850ish – not sure we will get that high either but you never know! I have plotted the arrow on the 10min chart today, so you can see that channel quite clearly. A break of that would lead to 6713 and possibly lower.